Understanding Non-Cash Expenses: A Comprehensive Guide

Non-cash expenses appear on an income statement because accounting principlesIB Manual – Accounting PrinciplesAccounting Principles for Investment Banking Analysts. A fundamental understanding of accounting principles is critical to creating any meaningful financial analysis. Analysis of mergers and acquisitions requires knowledge of accounting concepts. We build from the beginning and try to summarize and explain accounting require them to be recorded despite not actually being paid for with cash. The most common example of a non-cash expense is depreciationDepreciation ExpenseWhen a long-term asset is purchased, it should be capitalized instead of being expensed in the accounting period it is purchased in., where the cost of an asset is spread out over time even though the cash expense occurred all at once.

How Non-Cash Expenses Work

Here is an example of how a non-cash expense occurs:

- On July 1, 2017, a company purchases a computer for $2,500 with cash. The computer is estimated to have a useful life of five years, so an annual depreciation expense of $500 is created for the next five years.

- In 2017, the company will have a depreciation expense of $500 on the income statement, and an investment of $2,500 on the cash flow statement.

- In 2018, the company will have a depreciation expense of $500 on the income statement, and no investment recorded on the cash flow statement.

- This continues until 2022 when the depreciation from this computer is now $0 because it is fully depreciated.

As you can see, the $500 depreciation expense is actually a non-cash item, and the capital cost is recorded only once on the cash flow statement.

List of the Most Common Non-Cash Expenses

There are many types to watch out for, but the most common examples include:

- Depreciation

- Amortization

- Stock-based compensation

- Unrealized gains

- Unrealized losses

- Deferred income taxes

- Goodwill impairmentsGoodwill Impairment AccountingGoodwill is acquired and recorded on the books when an entity purchases another entity for more than the fair market value of its assets.

- Asset write-downsInventory Write DownAn inventory write down is an accounting process used to record the reduction of an inventory’s value, and is required when the inventory's

- Provisions and contingencies for future losses

Why Non-Cash Charges Need to be Adjusted for in Financial Analysis

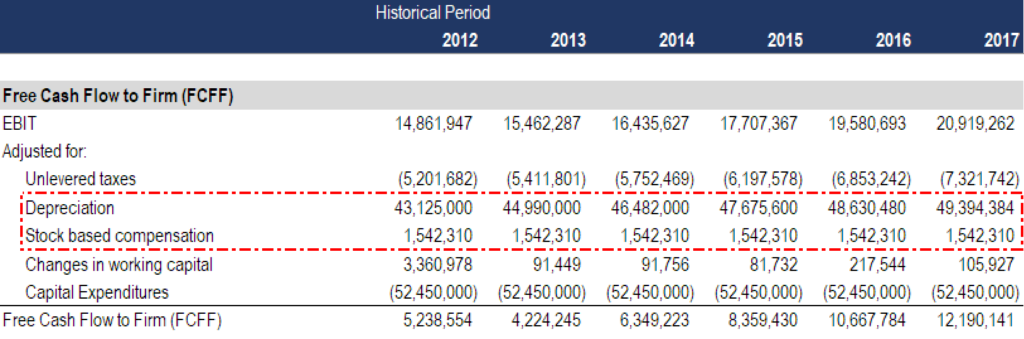

When performing a financial valuation of a company, an analyst typically performs a Discounted Cash Flow (DCF)DCF Model Training Free GuideA DCF model is a specific type of financial model used to value a business. The model is simply a forecast of a company’s unlevered free cash flow analysis based on its Free Cash Flow (FCF)Free Cash Flow (FCF)Free Cash Flow (FCF) measures a company’s ability to produce what investors care most about: cash that's available be distributed in a discretionary way.. FCF is used because it demonstrates the true economic viability of a company.

Since analysts can’t use net income in a DCF model, they need to adjust net income for all the non-cash charges (and make other adjustments) to arrive at free cash flow.

Below is an example of how an analyst would make the above adjustments when building a financial model.

Source: CFI financial modeling courses.

Additional resources

Thank you for reading this guide to non-cash expenses and charges that need to be adjusted in financial modeling and valuation. CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- How the 3 financial statements are linkedCFI Webinar - Link the 3 Financial StatementsThis CFI quarterly webinar provides a live demonstration of how to link the 3 financial statements in Excel. Learn the formulas and proper linking procedure

- How to go a great financial analystThe Analyst Trifecta® GuideThe ultimate guide on how to be a world-class financial analyst. Do you want to be a world-class financial analyst? Are you looking to follow industry-leading best practices and stand out from the crowd? Our process, called The Analyst Trifecta® consists of analytics, presentation & soft skills

- Financial modeling guideFree Financial Modeling GuideThis financial modeling guide covers Excel tips and best practices on assumptions, drivers, forecasting, linking the three statements, DCF analysis, more

- Valuation techniquesValuation MethodsWhen valuing a company as a going concern there are three main valuation methods used: DCF analysis, comparable companies, and precedent transactions

-

Petty Cash: Definition, Uses & Management for Businesses

Petty cash refers to a small amount of hard currency that a businesses will keep on hand to pay for miscellaneous and unexpected items, such as team lunches, birthday cakes, or office snacks. Pe

-

Understanding Prepaid Expenses: Definition & Accounting

Prepaid expenses represent expendituresExpenditureAn expenditure represents a payment with either cash or credit to purchase goods or services. An expenditure is recorded at a single point in that hav

finance

- Understanding Financial Barriers: How Costs Impact Your Lifestyle

- Cash Reserves: Definition, Benefits & Short-Term Needs

- Financial Controls: Definition, Importance & Key Processes

- Financial Covenants: Definition, Types & Importance

- Understanding Financial Ratios: A Comprehensive Guide

- Understanding Financial Statement Footnotes: A Comprehensive Guide

- Understanding Finance: A Comprehensive Overview

- Understanding Cash Equivalents: Definition & Examples

- Understanding Financial Services: A Comprehensive Guide

-

Understanding Maintenance Expenses: A Comprehensive Guide

Understanding Maintenance Expenses: A Comprehensive GuideMaintenance expenses are costs incurred on a regular basis to keep an asset working in its optimal condition. Maintenance costs come into play when a person purchases an asset, such as a motor vehicle...

-

Understanding Operating Expenses (OPEX): A Comprehensive Guide

Understanding Operating Expenses (OPEX): A Comprehensive GuideOperating expenses, operating expenditures, or “opex,” refers to the costs incurred by a business for its operational activities. In other words, operating expenses are the costs that a co...