Syndicated Loans: Definition, Benefits & How They Work

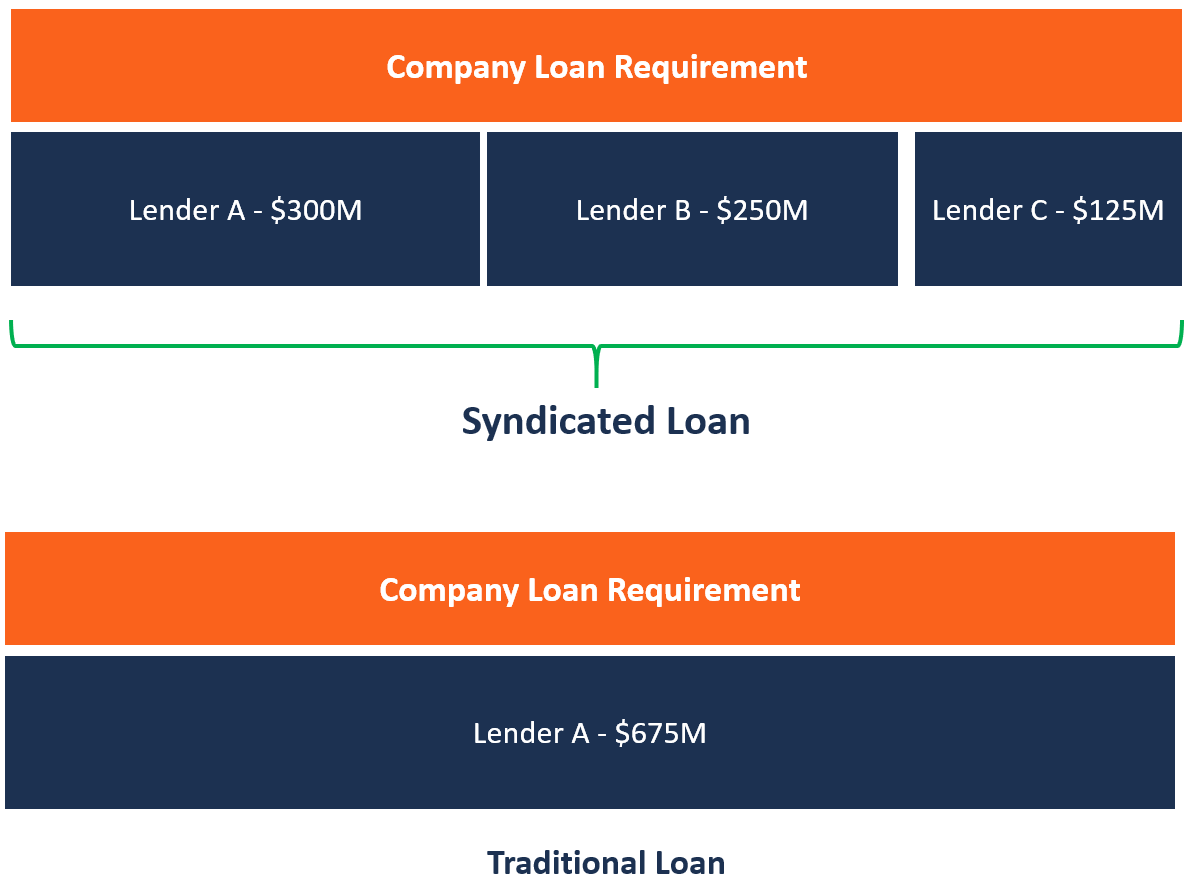

A syndicated loan is offered by a group of lenders who work together to provide credit to a large borrower. The borrower can be a corporationCorporationA corporation is a legal entity created by individuals, stockholders, or shareholders, with the purpose of operating for profit. Corporations are allowed to enter into contracts, sue and be sued, own assets, remit federal and state taxes, and borrow money from financial institutions., an individual project, or a government. Each lender in the syndicate contributes part of the loan amount, and they all share in the lending risk. One of the lenders act as the manager (arranging bank), which administers the loan on behalf of the other lenders in the syndicate. The syndicate may be a combination of various types of loans, each with different repayment terms that are agreed upon during negotiationsNegotiation TacticsNegotiation is a dialogue between two or more people with the aim of reaching a consensus over an issue or issues where conflict exists. Good negotiation tactics are important for negotiating parties to know in order for their side to win or to create a win-win situation for both parties. between the lenders and the borrower.

Loan syndication occurs when a single borrower requires a large loan ($1 million or more) that a single lender may be unable to provide, or when the loan is outside the scope of the lender’s risk exposure. LendersTop Banks in the USAAccording to the US Federal Deposit Insurance Corporation, there were 6,799 FDIC-insured commercial banks in the USA as of February 2014. then form a syndicate that allows them to spread the risk and share in the financial opportunity. The liability of each lender is limited to their share of the total loan. The agreement for all members of the syndicate is contained in one loan agreement.

To learn techniques on how to analyze a company’s Financials check out CFI’s Financial Analysis Fundamentals Course.

Participants in a Syndicated Loan

Those who participate in loan syndication may vary from one deal to another, but the typical participants include the following:

1. Arranging bank

The arranging bank is also known as the lead manager and is mandated by the borrower to organize the funding based on specific agreed terms of the loan. The bank must acquire other lending parties who are willing to participate in the lending syndicate and share the lending risks involved. The financial terms negotiated between the arranging bank and the borrower are contained in the term sheetTerm Sheet TemplateDownload our term sheet template example. A term sheet outlines the basic terms and conditions under of an investment opportunity and nonbinding agreement.

The term sheet details the amount of the loan, repayment scheduleDebt ScheduleA debt schedule lays out all of the debt a business has in a schedule based on its maturity and interest rate. In financial modeling, interest expense flows, interest rate, duration of the loan and any other fees related to the loan. The arranging bank holds a large proportion of the loan and will be responsible for distributing cash flows among the other participating lenders.

2. Agent

The agent in a syndicated loan serves as a link between the borrower and the lenders and owes a contractual obligation to both the borrower and the lenders. The role of the agent to the lenders is to provide them with information that allows them to exercise their rights under the syndicated loan agreement. However, the agent has no fiduciary duty and is not required to advise the borrower or the lenders. The agent’s duty is mainly administrative.

3. Trustee

The trustee is responsible for holding the security of the assets of the borrower on behalf of the lenders. Syndicated loan structures avoid granting the security to the individual lenders separately since the practice would be costly to the syndicate. In the event of default, the trustee is responsible for enforcing the security under instructions by the lenders. Therefore, the trustee only has a fiduciary duty to the lenders in the syndicate.

Advantages of a Syndicated Loan

The following are the main advantages of a syndicated loan:

1. Less time and effort involved

The borrower is not required to meet all the lenders in the syndicate to negotiate the terms of the loan. Rather, the borrower only needs to meet with the arranging bank to negotiate and agree on the terms of the loan. The arranger then does the bigger work of establishing the syndicate, bringing other lenders on board, and discussing the loan terms with them to determine how much credit each lender will contribute.

2. Diversification of loan terms

Since a syndicated loan is contributed to by multiple lenders, the loan can be structured in different types of loans and securities. The varying loan types offer different types of interest, such as fixed or floating interest ratesFloating Interest RateA floating interest rate refers to a variable interest rate that changes over the duration of the debt obligation. It is the opposite of a fixed rate., which makes it more flexible for the borrower. Also, borrowing in different currencies protects the borrower from currency risks resulting from external factors such as inflation and government laws and policies.

3. Large amount

Loan syndication allows borrowers to borrow large amounts to finance capital-intensive projects. A large corporation or government can borrow a huge loan to finance large equipment leasing, mergers, and financing transactions in telecommunications, petrochemical, mining, energy, transportation, etc. A single lender would be unable to raise funds to finance such projects, and therefore, bringing several lenders to provide the financing makes it easy to carry out such projects.

4. Positive reputation

The participation of multiple lenders to finance a borrower’s project is a reinforcement of the borrower’s good market image. Borrowers that have successfully paid syndicated loans in the past elicit a positive reputation among lenders, which makes it easier for them to access credit facilities from financial institutions in the future.

Related Readings

Thank you for reading CFI’s explanation of a syndicated loan. CFI offers the Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

- Debt CovenantDebt CovenantsDebt covenants are restrictions that lenders (creditors, debt holders, investors) put on lending agreements to limit the actions of the borrower (debtor).

- Junior TrancheJunior TrancheA junior tranche is an unsecured debt that ranks lower in repayment priority than other debts in the event of default. It is also referred to as subordinated debt.

- Letter of CommitmentLetter of CommitmentA letter of commitment is a formal binding agreement between a lender and a borrower. It outlines the terms and conditions of the loan and the nature of the prospective loan. It serves as the agreement that initiates an official loan borrowing process.

- Senior and Subordinated DebtSenior and Subordinated DebtIn order to understand senior and subordinated debt, we must first review the capital stack. Capital stack ranks the priority of different sources of financing. Senior and subordinated debt refer to their rank in a company's capital stack. In the event of a liquidation, senior debt is paid out first

-

What is a Stock Loan?

A stock loan is a type of transaction that commonly occurs between two different stock brokers. This type of transaction is also known as a securities loan. Here are the basics of a stock loan a

-

Personal Loans: A Comprehensive Guide to Understanding and Applying

When you need money–whether it’s to consolidate debts, pay for an emergency, or get caught up on everyday bills–a personal loan is one option you might consider. Personal loans are j

finance

- Collateral Explained: What It Is & How It Works

- FHA Loans: Your Guide to Government-Backed Mortgages

- Understanding Interest: Costs & Rewards of Borrowing and Lending

- Leveraged Loans: Definition, Features & Who Uses Them

- Understanding Loans: Definition, Types & How They Work

- Loan Covenants: Understanding Terms & Conditions

- Loan Servicing Explained: What It Is & How It Works

- Starter Loans: Build Credit with Low or No Credit History

- Syndicated Loans: Definition, How They Work & Key Features

-

Amortization Explained: Understanding Debt Repayment & Schedules

Amortization Explained: Understanding Debt Repayment & SchedulesAmortization refers to the process of paying off a debt through scheduled, pre-determined installments that include principal and interestDebt ScheduleA debt schedule lays out all of the debt a busine...

-

Annuity Loans: Access Retirement Funds Without Cashing Out

An annuity loan is a type of loan an annuity holder borrows money against the cash value of the annuity contract. This type of loan allows individuals to access their retirement funds without go...