Understanding Distribution Yield: A Key Metric for REIT & ETF Investors

Distribution yield is defined as a way of measuring the annual income payments made to unitholders, by an A-REIT or an ETF, as a percentage or portion of its unit price. It is used as a measure of income relative to the size of an investment.

Distributions are similar to dividends. They are commonly received by individuals or investors with investments in exchange-traded funds (ETFs)Exchange Traded Fund (ETF)An Exchange Traded Fund (ETF) is a popular investment vehicle where portfolios can be more flexible and diversified across a broad range of all the available asset classes. Learn about various types of ETFs by reading this guide. and/real estate investment trusts (REITs). A distribution can be defined as a portion of the profits generated by a trust or a fund, which is distributed to unitholders or investors, and an income payment. It is one method of making money from investment classes (ETFs and REITs). The capital gains and distributions made from the investments ideally make up an investor’s total return.

Summary

- Distribution yield is defined as a way of measuring the annual income payments made to unitholders, by an A-REIT or an ETF, as a percentage or portion of its unit price.

- Distribution yield is used as a measure of income relative to the size of an investment.

- It is important to note that a distribution yield is based on a fund’s past performance and that the yield computations do not include or make any projections for future performance.

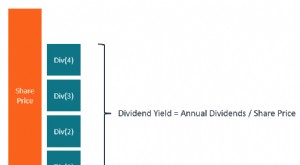

Calculating the Distribution Yield

The formula below shows how the distribution yield can be calculated:

The distribution yield equation makes use of the recent distribution and multiplies the amount by 12 to produce an average annual return. The annualized sum is then divided by the net asset value (NAV)Net Asset ValueNet asset value (NAV) is defined as the value of a fund’s assets minus the value of its liabilities. The term "net asset value" is commonly used in relation to mutual funds and is used to determine the value of the assets held. According to the SEC, mutual funds and Unit Investment Trusts (UITs) are required to calculate their NAV at the end of the period to estimate the yield of the distribution. The end of the period can be the end of the month and the distribution can include a capital gain, gains in the form of interest received, or the declaration and receipt of a special dividend. Distribution yields on annuitiesAnnuityAn annuity is a financial product that provides certain cash flows at equal time intervals. Annuities are created by financial institutions, primarily life insurance companies, to provide regular income to a client. and fixed income portfolios can serve as a proxy for cash flow comparisons and analysis.

It should be noted that a distribution yield is based on a fund’s past performance and that the yield computations do not include or make any projections for future performance. The distribution yield, therefore, does not provide concrete information on what a bond fund will produce from the time it is purchased or invested in, to the time that it is sold off.

Distributions that consist of recurrent dividends and interest tend to be more accurate in comparison to distributions with irregular payments. Excluding irregular distributions or payment may result in lower distribution yields, although the inclusion of the payments can also distort the yield calculated.

Furthermore, although distribution yields provide investors with highlights for income payments, the variables associated with special dividend payments and capital gain distribution may provide skewed returns. It is why investors find the sum of the distributions over the recent 12-month periods and divide the sum by the NAV at the time of computation to find the true or more reliable yield.

Drawbacks of the Dividend Yield Computation

The dividend yield computation does come with a few drawbacks. One of the first challenges to be mindful of is the fact that the calculation is based on the assumption that the last 30-day income multiplied by 12 will result in the 12-month returns. Although the sum-product may provide a good estimate and picture of the returns gained over the 12-month period, it is not always the same and the actual returns made may differ.

Secondly, the computation assumes a 30-day month; however, not all months have 30 days. It can affect the accuracy of the calculation. One example can be the days in the month of February. February normally has 28 days and 29 days on a leap year. Months like August have 31 days. The variation in actual lengths of a month may result in a skewed distribution yield. The difference will not be significant, but it does have an impact.

Furthermore, another assumption of the distribution yield computation is that the net present value is an average NAV of the last 12 months. It is not always the case.

SEC Yield vs. Distribution Yield

The SEC yield is relevant to companies that fall under the jurisdiction of the Securities and Exchange Commission (SEC)Securities and Exchange Commission (SEC)The US Securities and Exchange Commission, or SEC, is an independent agency of the US federal government that is responsible for implementing federal securities laws and proposing securities rules. It is also in charge of maintaining the securities industry and stock and options exchanges and the figure is to be reported to the SEC. Following an assumption that an investor holds each bond in a portfolio to maturity, the SEC yield is used to provide an estimate on the yield an investor is expected to receive. Moreover, the yield follows an assumption that the income made will be reinvested, and it also accounts for expenses and fees.

It is argued that the SEC may provide more accurate results in comparison to the distribution yield and the calculation displays more month-to-month consistencies. Both calculations show past performance and not future performance, and the calculations both follow assumptions that may result in skewed results. However, the SEC yield is standardized, which allows investors to easily make comparisons.

More Resources

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

- Annualized Rate of ReturnAnnualized Rate of ReturnAnnualized rate of return is a way of calculating investment returns on an annual basis. As we invest, we often want to know how much we are earning

- Cap RateCap Rate (REIT)Cap rate is a financial metric that is used by real estate investors to analyze real estate investments, and determine their potential rate of return based

- Effective YieldEffective YieldEffective yield is a financial metric that measures the interest rate – also known as the coupon rate – return on a bond.

- Capital GainCapital GainA capital gain is an increase in the value of an asset or investment resulting from the price appreciation of the asset or investment. In other words, the gain occurs when the current or sale price of an asset or investment exceeds its purchase price.

-

Understanding HSA Distributions: How to Access Your Health Savings Account Funds

You can use a health savings account (HSA) to pay your medical expenses and decrease your tax burden. The funds in these accounts belong to the contributor, unlike medical insurance premiums, which, o

-

Understanding Forward Dividend Yield: A Key Metric for Investors

Forward dividend yield refers to the projection of a company’s yearly dividend. It’s calculated as a percentage of the current share price. For many investors, the dividends paid out by co

invest

- Understanding Deeds of Distribution: Estate Planning & Property Transfer

- Discount Yield Explained: Calculating Returns on Discounted Bonds

- Understanding Distribution Waterfalls in Equity Investing

- Effective Yield: Understanding Compounding for Bond Investments

- Understanding Money Market Yields: A Comprehensive Guide

- Understanding Roll Yield in Commodity Futures

- Understanding SEC Yield: A Guide for Bond Investors

- Understanding Sovereign Bond Yields: Risks & Rates

- Yield Farming Explained: A Beginner's Guide to DeFi

-

Nominal Yield Explained: Definition & Calculation

Nominal Yield Explained: Definition & CalculationNominal yield is a fixed percentage amount calculated for fixed income securitiesFixed Income SecuritiesFixed income securities are a type of debt instrument that provides returns in the form of regul...

-

Understanding the Par Yield Curve: A Guide for Investors

Understanding the Par Yield Curve: A Guide for InvestorsThe par yield curve is a graphical representation that shows the yield to maturityYield to Maturity (YTM)Yield to Maturity (YTM) – otherwise referred to as redemption or book yield – is th...