Understanding Distribution Waterfalls in Equity Investing

A distribution waterfall is a popular term in equity investing that refers to the way in which capital gainsCapital GainA capital gain is an increase in the value of an asset or investment resulting from the price appreciation of the asset or investment. In other words, the gain occurs when the current or sale price of an asset or investment exceeds its purchase price. of a fund are allocated between the participants in an investment, typically the limited partners (LPs) and the general partner (GP).

The capital of limited partners is managed by the general partner in a private equity fundPrivate Equity FundsPrivate equity funds are pools of capital to be invested in companies that represent an opportunity for a high rate of return. They come with a fixed. The general partner himself contributes a relatively small proportion of the total investment. Distribution waterfall structures are put in place primarily to ensure that profits are allocated to the manager only after the limited partners have received the agreed return on their investment. The structures are detailed in the distribution section of the private placement memorandum (PPM).

Summary

- A distribution waterfall is a popular term in equity investing that refers to the way in which capital gains of a fund are allocated between the participants in an investment, typically the limited partners (LPs) and the general partner (GP).

- Its main purpose is to align incentives for the general partner and define a pay structure for limited partners.

- It generally comprises four cascading tiers: the return of capital, preferred return, catch-up, and carried interest.

- The European and American distribution waterfalls are the most common types of waterfall structures; the former favors the investors while the latter leans towards the manager.

Importance of the Distribution Waterfall

A distribution waterfall lays down the rules and procedures for the distribution of profits in a private equity investment agreement. Its main purpose is to align incentives for the general partner and define a pay structure for limited partners.

The distribution structure can be visualized as a set of buckets placed one below the other. Each bucket defines an allocation of profits. When the first bucket is filled to the brim, the profits flow into the second bucket, and so on.

In such a manner, the capital flows from limited partners (favored by the initial buckets) to the general partner (favored by buckets further away from the source). Such a structure of allocation protects the interests of the investors and, at the same time, incentivizes the general partner to maximize the return of the fund.

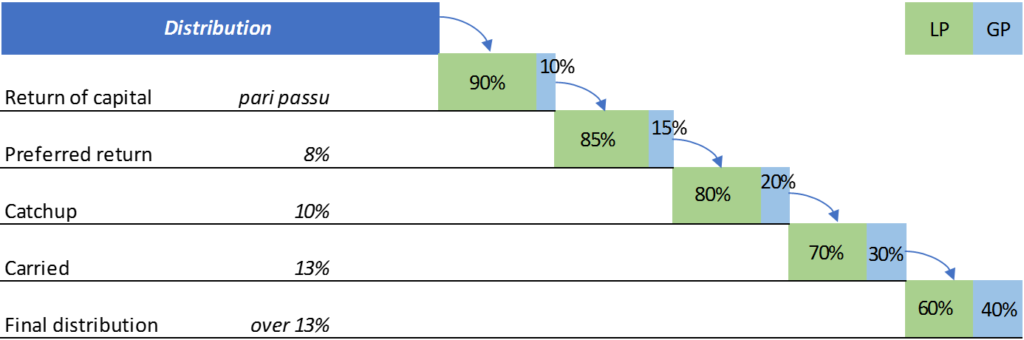

Tiers in a Distribution Waterfall Structure

The allocation in question derives its name from the cascading nature of its four constituent tiers, which are shown below.

In addition, the hurdle rate, which is the minimum rate of returnRate of ReturnThe Rate of Return (ROR) is the gain or loss of an investment over a period of time copmared to the initial cost of the investment expressed as a percentage. This guide teaches the most common formulas on an investment required by an investor, can be another tier. In case an excessive incentive fee is given to the manager or general partner, a “clawback” clause in the PPM mandates the return of such excess fees.

The four tiers are:

Return of Capital: The initial capital investments of investors, plus some expenses and fees, are returned to them.

Preferred Return: 100% of the distribution goes to the LPs until the preferred internal rate of return based on every distribution to them and every contribution called is reached.

Catch-up: The catch-up bucket is highly favorable to the general partner. They are given all or a major portion of the gain until they receive a certain percentage of profits.

Carried Interest: It constitutes the allocation of the remaining amount between the limited and general partners.

European Waterfall vs. American Waterfall

The European or global waterfall distribution is applied at an aggregate fund level. It gives precedence to the distribution of initial capital investment and a preferred return to the investors over the distribution of profits to the general partner/manager. The biggest drawback to the European structure is the payment structure of the manager, who may be demotivated to maximize investment returns in the long term.

On the other hand, the American waterfall distribution is applied on a deal-by-deal basis. It favors the general partners over limited partners of the fund and gives precedence to the distribution of profits to the GP. However, it may include a “clawback” clause in the agreement to make the equity fund attractive to investors.

Related Readings

CFI offers the Capital Markets & Securities Analyst (CMSA)® Program Page - CMSAEnroll in CFI's CMSA® program and become a certified Capital Markets &Securities Analyst. Advance your career with our certification programs and courses.certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below:

- Capital Gains TaxCapital Gains TaxCapital gains tax is a tax imposed on capital gains or the profits that an individual makes from selling assets. The tax is only imposed once the asset has been converted into cash, and not when it’s still in the hands of an investor.

- General PartnershipGeneral PartnershipA General Partnership (GP) is an agreement between partners to establish and run a business together. It is one of the most common legal entities to form a business. All partners in a general partnership are responsible for the business and are subject to unlimited liability for business debts.

- Hurdle RateHurdle Rate DefinitionA hurdle rate, which is also known as minimum acceptable rate of return (MARR), is the minimum required rate of return or target rate that investors are expecting to receive on an investment. The rate is determined by assessing the cost of capital, risks involved, current opportunities in business expansion, rates of return for similar investments, and other factors

- Internal Rate of Return (IRR)Internal Rate of Return (IRR)The Internal Rate of Return (IRR) is the discount rate that makes the net present value (NPV) of a project zero. In other words, it is the expected compound annual rate of return that will be earned on a project or investment.

-

Non-Qualifying Investments: Understanding Tax Implications

A non-qualifying investment is a type of investment that can never be subject to any tax benefits. Tax benefits include deductions, exemptions, and credits. The benefits are used to reduce taxable inc

-

Portfolio Planning: A Comprehensive Guide to Investment Strategies

Portfolio planning is the process of strategizing the construction of an investment portfolio. The investment portfolio should be encompassing of the investor’s risk toleranceRisk ToleranceRisk

invest

- Understanding Deeds of Distribution: Estate Planning & Property Transfer

- Understanding Investments: A Beginner's Guide to Growth & Income

- Understanding Distribution Yield: A Key Metric for REIT & ETF Investors

- Understanding Drawdowns: A Key Investment Risk

- Understanding Investment Horizon: A Comprehensive Guide

- Brownfield Investment: Definition, Benefits & Examples

- Investment Trusts Explained: A Comprehensive Guide

- Hedging Explained: Protect Your Investments from Risk

- Distribution Waterfall Explained: Allocation of Investment Returns

-

Loss Aversion: Understanding the Psychology of Financial Decisions

Loss Aversion: Understanding the Psychology of Financial DecisionsLoss aversion is a tendency in behavioral financeBehavioral FinanceBehavioral finance is the study of the influence of psychology on the behavior of investors or financial practitioners. It also inclu...

-

Micro-Investing Platforms: A Beginner's Guide to Small Investments

Micro-Investing Platforms: A Beginner's Guide to Small InvestmentsA micro-investing platform is an application that eases the process of investment by enabling users to save and invest small amounts of money periodically. Micro-investing platforms are different from...