Understanding Interest Rate Sensitivity: A Key Concept for Investors

Interest rate sensitivity is the analysis of fixed income security price fluctuations to changes in the market interest rate. The higher the security’s interest rate sensitivity, the greater the price fluctuations.

Summary

- Interest rate sensitivity is the analysis of fixed income security price fluctuations to changes in the market interest rate.

- It is an important consideration when selling and buying fixed income on the secondary market.

- Interest rate sensitivity is affected by factors such as the asset’s maturity length and coupon rate.

Understanding Interest Rate Sensitivity

Fixed income is one of the major asset classes available to investors. Investors profit from fixed income through the interest (coupon) rate and price appreciation. Fixed income coupon payments are fixed over the life of the security, while price fluctuations are a direct outcome of market interest rate changes.

Fixed income securities are created and initially sold on the primary market. Next, investors can choose to hold the fixed income security until maturity or resell it on the secondary market. Fixed income price is negatively correlated with the market interest rate – this is known as interest rate risk.

At issuance, coupon bonds are sold at par valuePar ValuePar Value is the nominal or face value of a bond, or stock, or coupon as indicated on a bond or stock certificate. It is a static value based on the prevailing market interest rate. Once the bond is issued, the coupon payments are fixed over the life of the loan, but the market interest rate fluctuates continuously.

When the market interest rate increases, the outstanding fixed-income security prices depreciate because newly issued fixed-income securities will pay higher coupon payments. Vice versa, if the market interest rate decreases, the outstanding fixed income prices appreciate because its coupon payments are higher than newly issued fixed income securities.

Therefore, understanding interest rate sensitivity becomes an important consideration in selecting fixed-income securities. Certain characteristics affect a security’s interest rate sensitivity, such as:

1. Maturity Length

The longer the maturity is, the higher the security’s interest rate sensitivity. This is because longer-term securities have higher exposure to interest rate riskInterest Rate RiskInterest rate risk is the probability of a decline in the value of an asset resulting from unexpected fluctuations in interest rates. Interest rate risk is mostly associated with fixed-income assets (e.g., bonds) rather than with equity investments..

2. Coupon Rate

The lower the coupon rate, the higher the security’s interest rate sensitivity because it will have higher interest rate risk.

How to Measure Interest Rate Sensitivity

To measure interest rate sensitivity, duration is a great metric because it takes such characteristics into consideration. The general rule of thumb is the higher the duration, the higher the interest rate sensitivity. The three most common types of duration are:

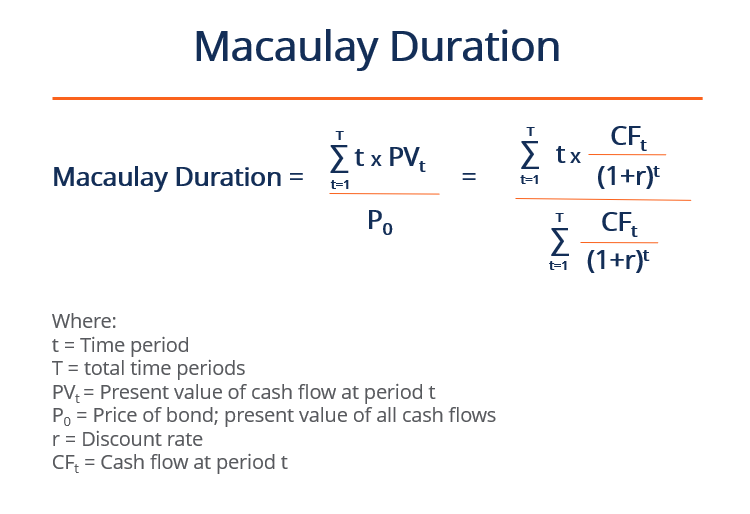

1. Macaulay Duration

The Macaulay duration represents the length of time the investor must hold the security until its total cash flows can repay the bond’s price. For coupon-paying bonds, the Macaulay duration is always shorter than its time to maturity. With zero-coupon bondsZero-Coupon BondA zero-coupon bond is a bond that pays no interest and trades at a discount to its face value. It is also called a pure discount bond or deep discount bond. (bonds without coupon payments that are sold at a discount), the Macaulay duration is equal to its time to maturity.

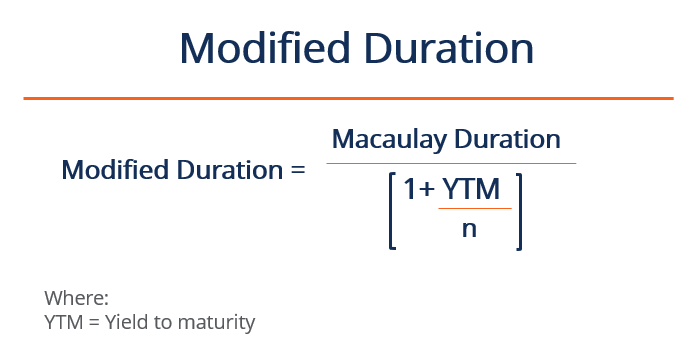

2. Modified Duration

The Modified duration builds on the Macaulay duration by integrating the yield to maturity. It represents the percentage change in bond price in relation to the percentage change in the interest rate.

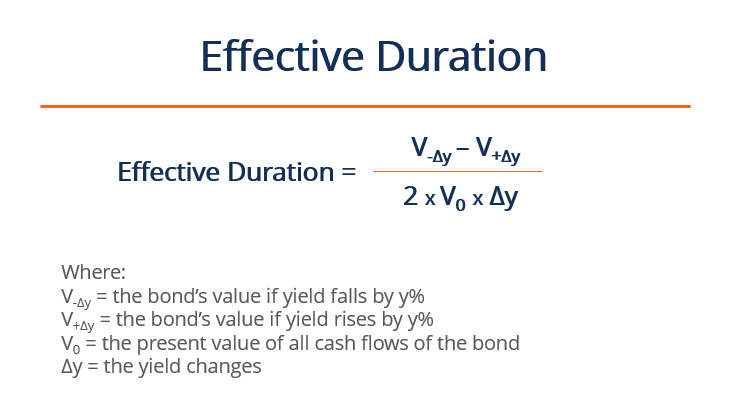

3. Effective Duration

The effective durationEffective DurationEffective duration is the sensitivity of a bond's price against the benchmark yield curve. One way to assess the risk of a bond is to estimate the is applied specifically to bonds with embedded options to account for its uncertainty of future cash flows. The effective duration serves as the percentage change in price relative to the percentage change in yield to maturity.

Practical Example

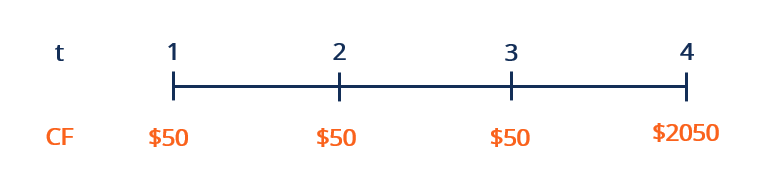

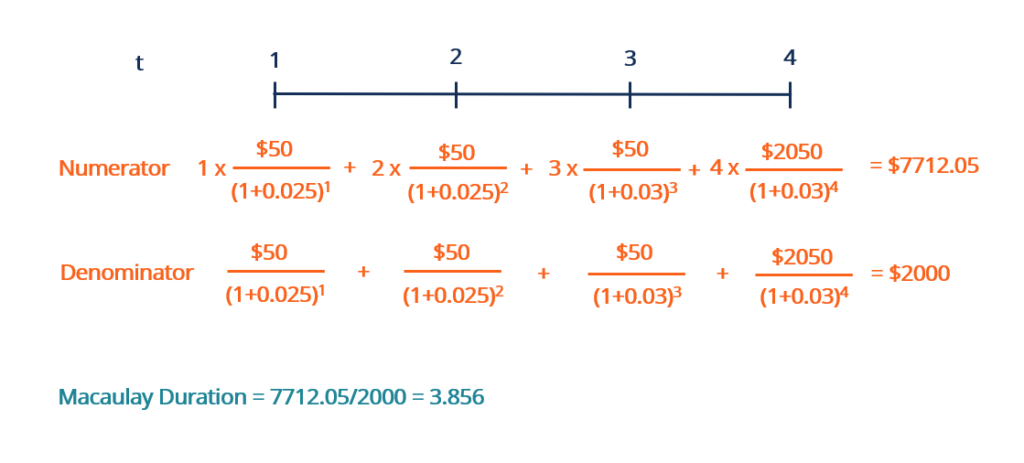

Suppose an investor purchases a $2,000 par value bond with a 2.5% coupon rate compounded annually. The maturity date is four years from today, on which the principal $2,000 will be returned. What is the Macaulay duration of the bond?

While the formula may look intimidating, the numerator and the denominator are almost identical, except each cash flow in the numerator is multiplied by its respective time period t. For the discount rate r, we are using the coupon rate of the bond.

With the numerator and denominator solved, we put those together to get a Macaulay duration of 3.856. It means that it will take approximately 3.856 years of holding the bond for its cash flows to cover its price. Because the bond pays coupon payments, the Macaulay duration is shorter than its time to maturity of four years.

Learn More

CFI offers the Capital Markets & Securities Analyst (CMSA)®Program Page - CMSAEnroll in CFI's CMSA® program and become a certified Capital Markets &Securities Analyst. Advance your career with our certification programs and courses. certification program for those looking to take their careers to the next level. To keep learning and advance your career, the following resources will be helpful:

- Bond PricingBond PricingBond pricing is the science of calculating a bond's issue price based on the coupon, par value, yield and term to maturity. Bond pricing allows investors

- Secondary MarketSecondary MarketThe secondary market is where investors buy and sell securities from other investors. Examples: New York Stock Exchange (NYSE), London Stock Exchange (LSE).

- Sensitivity AnalysisWhat is Sensitivity Analysis?Sensitivity Analysis is a tool used in financial modeling to analyze how the different values for a set of independent variables affect a dependent variable

- Yield to Maturity (YTM)Yield to Maturity (YTM)Yield to Maturity (YTM) – otherwise referred to as redemption or book yield – is the speculative rate of return or interest rate of a fixed-rate security.

-

![Covered Interest Rate Parity (CIRP): Explained | [Your Brand Name]](https://www.etffin.com/article/uploadfiles/202110/2021100815223296_S.jpeg)

Covered Interest Rate Parity (CIRP): Explained | [Your Brand Name]

Covered interest rate parity (CIRP) is a theoretical financial condition that defines the relationship between interest rates and the spot and forward currency rates of two countries. It establishes t

-

Floating Rate Notes (FRNs): Explained - How They Work & Benefits

A floating rate note (FRN) is a debt instrument whose coupon rate is tied to a benchmark rate such as LIBORLIBORLIBOR, which is an acronym of London Interbank Offer Rate, refers to the interest r

invest

- Relative Interest Rates: Understanding Their Impact on the Economy

- Debentures Explained: A Comprehensive Guide to Unsecured Corporate & Government Debt

- Understanding Floating Interest Rates: Definition & How They Work

- Understanding Interest Rates: A Comprehensive Guide

- Understanding Interest Rate Risk: Definition & Impact

- Interest Rate Swaps: A Comprehensive Guide

- Simple Interest Explained: Calculation, Benefits & Examples

- Interest Rate Collar: Definition, Strategy & Benefits

- Interest Rate Caps: Understanding Protection for Adjustable-Rate Loans

-

Interest Rate Parity Explained: A Comprehensive Guide

Interest Rate Parity Explained: A Comprehensive GuideInterest rate parity connects the interest rates, spot exchange rates and forward exchange rates in a single comparison. The theory is that the differential between the interest rates of two cou...

-

Understanding the Policy Interest Rate: Its Impact on the Economy

Three more sleep inducing words have perhaps never been strung together, but the policy interest rate is actually pretty exciting insofar as it's a little number that has a profound effect on a c...