Understanding Floating Interest Rates: Definition & How They Work

A floating interest rate refers to a variable interest rate that changes over the duration of the debt obligation. It is the opposite of a fixed interest rate, where the interest rate remains constant throughout the life of the debt. Loans, such as residential mortgages,Mortgage-Backed Security (MBS)A Mortgage-backed Security (MBS) is a debt security that is collateralized by a mortgage or a collection of mortgages. An MBS is an asset-backed security that is traded on the secondary market, and that enables investors to profit from the mortgage business can be acquired at both fixed interest rates as well as at floating interest rates that periodically adjust per interest rate market conditions.

Breaking Down Floating Interest Rate

The change in interest rate with a floating rate loan is typically based on a reference, or “benchmark”, rate that is outside of any control by the parties involved in the contract. The reference rate is usually a recognized benchmark interest rate, such as the prime ratePrime RateThe term “prime rate” (also known as the prime lending rate or prime interest rate) refers to the interest rate that large commercial banks charge on loans and products held by their customers with the highest credit rating., which is the lowest rate that commercial banks charge their most creditworthy customers for loans (typically, large corporations or high net worth individuals).

Floating interest rate debt often costs less than fixed-rate debt, depending on the yield curve. In compensation for lower fixed rate costs, borrowers must bear a higher interest rate risk. Interest rate risk, for bonds, refers to the risk of rates rising in the future. When the yield curve is inverted, then the cost of debtCost of DebtThe cost of debt is the return that a company provides to its debtholders and creditors. Cost of debt is used in WACC calculations for valuation analysis. with floating interest rates may actually be higher than fixed-rate debt. However, an inverted yield curve is the exception rather than the norm.

Floating rates are more likely to be less expensive borrowing in the case of a long-term loan, such as a 30-year mortgage, because lenders require higher fixed rates for longer-term loans, due to the inability to accurately forecast economic conditions over such a long period of time. There is a general assumption that interest rates will rise – or, increase – over time,

Sometimes, a floating interest rate is offered with other special features, such as limits on the maximum interest rate that can be charged, or limits on the maximum amount by which the interest rate can be increased from one adjustment period to the next. These features are mostly found in mortgage loans. Such qualifying clauses in the loan contract are primarily to protect the borrower from the interest rate suddenly increasing to a prohibitive level that would likely cause the borrower to default.

Uses of Floating Interest Rate

There are many uses for a variable interest rate. Some of the most common examples are:

- Floating interest rates are used most commonly in mortgage loans. A reference rateEffective Annual Interest RateThe Effective Annual Interest Rate (EAR) is the interest rate that is adjusted for compounding over a given period. Simply put, the effective or index is followed, with the floating rate calculated as, for example, “the prime rate plus 1%”.

- Credit card companies may also offer floating interest rates. Again, the floating interest rate charged by the bank is usually the prime rate plus a certain spread.

- Floating rate loans are common in the banking industry for large corporate customers. The total rate paid by the customer is decided by adding (or, in rare cases, subtracting) a spread or margin to a specified base rate.

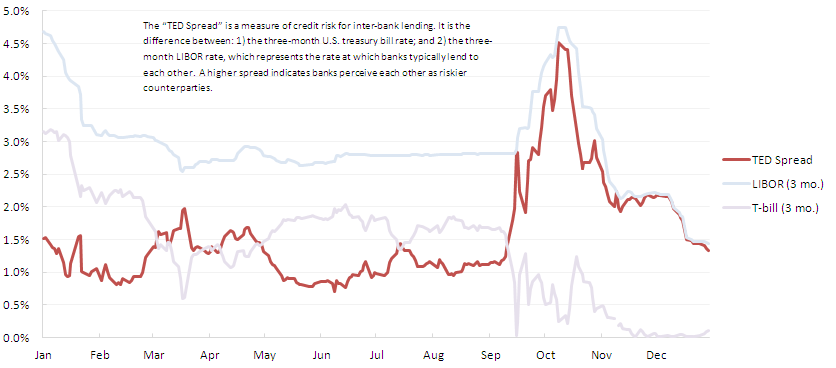

Reference Rate

Changes in the floating interest rate are based on a reference rate. Two of the most common reference rates used with floating interest loans are the prime rate in the U.S. and, in Europe, the London Interbank Offered Rate (LIBOR). The floating rate will be equal to the base rate plus a spread or margin.

For example, interest on a debt may be priced at the six-month LIBOR + 2%. This simply means that, at the end of every six months, the rate for the following period will be decided on the basis of the LIBOR at that point, plus the 2% spread. Floating interest rates may be adjusted quarterly, semi-annually, or annually.

Advantages of Floating Interest Rate

The following are the benefits of a variable interest rate:

- Generally, floating interest rates are lower compared to the fixed ones, hence, helping in reducing the overall cost of borrowing for the debtor.

- There is always a chance of unexpected gains. With higher risk also comes the prospect of future gains. The borrower will enjoy a benefit if interest rates decline, because the floating rate on his loan will go down. The lender will enjoy additional profit if interest rates rise, because he can then raise the floating rate charged to the borrower.

Disadvantages

The following are the potential disadvantages of a variable interest rate loan:

- The interest rate depends largely on market situations which can prove to be dynamic and unpredictable. Hence, the interest rate may increase to a point that the loan may become difficult to repay.

- The unpredictability of interest rate changes makes budgeting more difficult for the borrower. It also makes it harder for the lender to accurately forecast future cash flows.

- In times of unfavorable market conditions, financial institutions try to play it safe by putting the burden on customers. They will charge high premiums over the benchmark rate, ultimately affecting the pockets of borrowers.

Summary

Interest rates are some of the most influential components in the economy. They help in shaping day-to-day decisions of individuals and corporations, such as determining whether it’s a good time to buy a house, take out a loan, or put money in savings. The level of interest rates is inversely proportional to the level of borrowing, which, in turn, affects economic expansion. Interest rates influence stock prices, bond markets, and derivatives trading.

Related Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Debt ScheduleDebt ScheduleA debt schedule lays out all of the debt a business has in a schedule based on its maturity and interest rate. In financial modeling, interest expense flows

- Cost of DebtCost of DebtThe cost of debt is the return that a company provides to its debtholders and creditors. Cost of debt is used in WACC calculations for valuation analysis.

- Interest PayableInterest PayableInterest Payable is a liability account shown on a company’s balance sheet that represents the amount of interest expense that has accrued

- Fixed IncomeTrading & InvestingCFI's trading & investing guides are designed as self-study resources to learn to trade at your own pace. Browse hundreds of articles on trading, investing and important topics for financial analysts to know. Learn about assets classes, bond pricing, risk and return, stocks and stock markets, ETFs, momentum, technical

-

Understanding Interest Rate Options: A Comprehensive Guide

Interest rate options are a type of derivative that is based on the value of interest rates. They are generally tied to interest rate products like Treasury notes. Interest rate options are generally

-

Interest Rate Parity Explained: A Comprehensive Guide

Interest rate parity connects the interest rates, spot exchange rates and forward exchange rates in a single comparison. The theory is that the differential between the interest rates of two cou

finance

- Relative Interest Rates: Understanding Their Impact on the Economy

- Debentures Explained: A Comprehensive Guide to Unsecured Corporate & Government Debt

- Understanding Interest Rates: A Comprehensive Guide

- Understanding Interest Rate Risk: Definition & Impact

- Interest Rate Swaps: A Comprehensive Guide

- Simple Interest Explained: Calculation, Benefits & Examples

- Floating Rate Funds: Understanding & Investing in Variable Interest Rates

- Floating Rate Notes (FRNs): Explained - How They Work & Benefits

- Interest Rate Collar: Definition, Strategy & Benefits

-

Understanding Good Loan Interest Rates: What to Expect

Understanding Good Loan Interest Rates: What to ExpectWhat Is a Good Loan Interest Rate? What makes an interest rate "good" varies with the type of loan, and it changes over time. At different points in the 21st century, for instance, ...

-

Interest Rate Call Options: Understanding & Benefits

Interest Rate Call Options: Understanding & BenefitsAn interest rate option is a derivative whose contract value is based on interest rates. There are two types of interest rate options, calls and puts. An interest rate call option gives the individual...