Simple Interest Explained: Calculation, Benefits & Examples

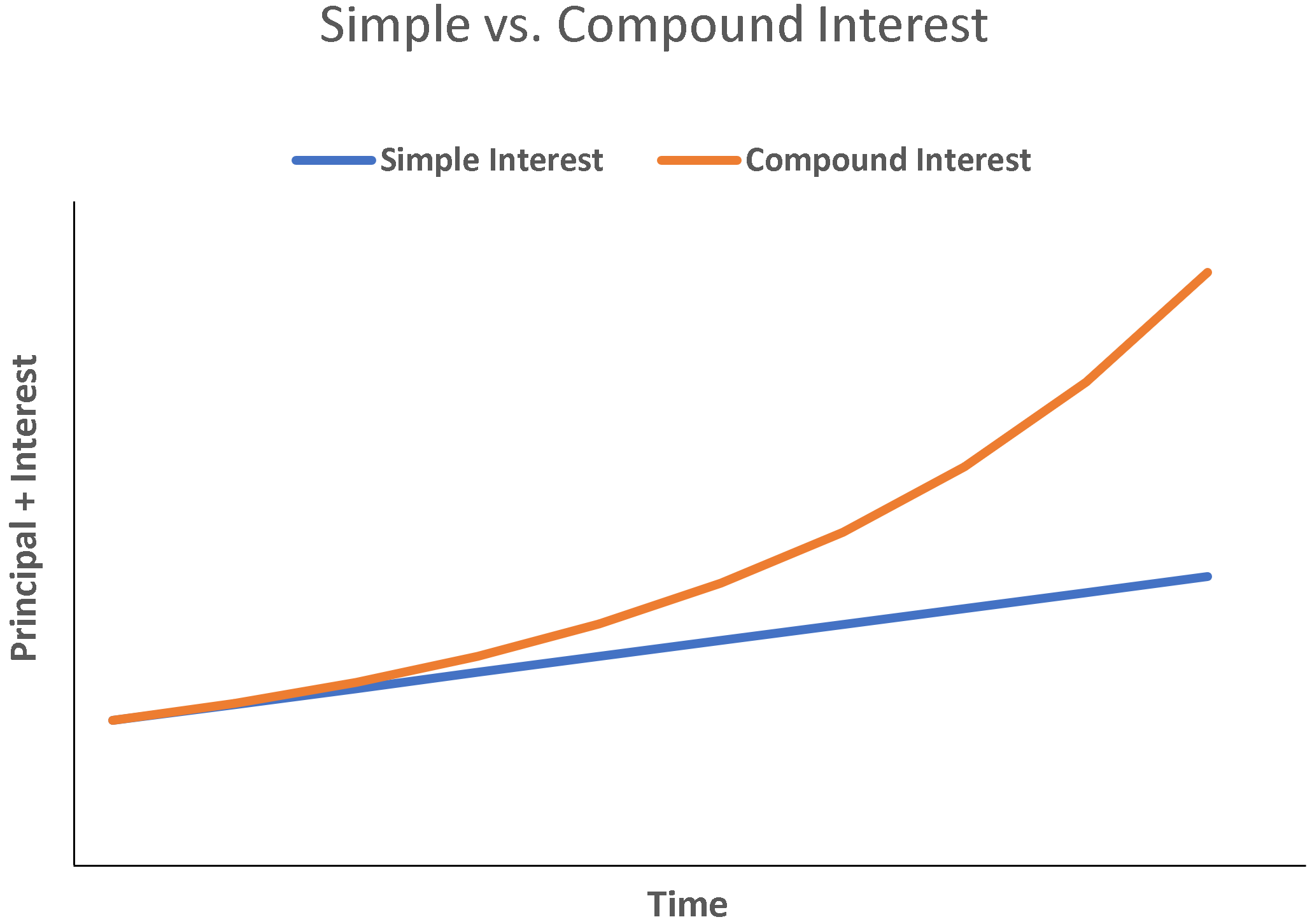

Simple interest is a calculation of interest that doesn’t take into account the effect of compounding. In many cases, interest compounds with each designated period of a loan, but in the case of simple interest, it does not. The calculation of simple interest is equal to the principal amount multiplied by the interest rate, multiplied by the number of periods.

For a borrower, simple interest is advantageous, since the total interest expense will be less without the effect of compounding. For a lender, compound interest is advantageous, as the total interest expense over the life of the loan will be greater.

Simple Interest Formula

Simple Interest: I = P x R x T

Where:

- P = Principal Amount

- R = Interest Rate

- T = No. of Periods

The period must be expressed for the same time span as the rate. If, for example, the interest is expressed in a yearly rate, such as in a 5% per annum (yearly) interest rate loan, then the number of periods must also be expressed in years. Note that sometimes changes to interest rates may be expressed in basis pointsBasis Points (BPS)Basis Points (BPS) are the commonly used metric to gauge changes in interest rates. A basis point is 1 hundredth of one percent. (BPS). It may be worth your while, as a financial professional, to learn how to convert BPS into interest rates.

If the interest rate is expressed as an annual figure, but the relevant time period is less than a year, then the interest rate must be prorated for one year. For example, if the interest rate is 8% per year, but the calculation in question calls for a quarterly interest rate, then the relevant interest rate is 2% per quarter. The 2% per quarter is equivalent to a simple interest rate of 8% per year. It is not the same, however, in the case of compounded interest.

Simple Interest Examples

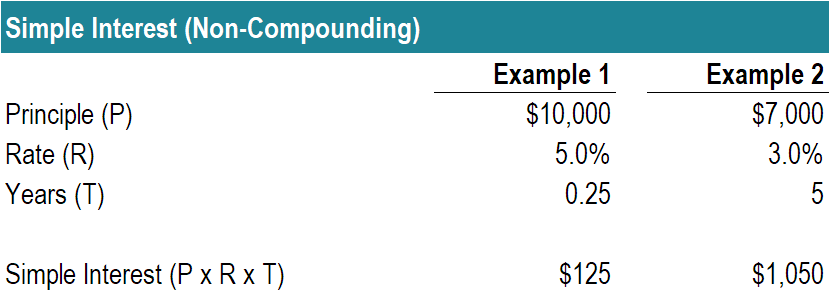

Example #1

Mr. Albertson plans to place his money in a certificate of deposit that matures in three months. The principal is $10,000 and 5% interest is earned annually. He wants to calculate how much interest he will earn in those three months.

I = P x R x T

I = $10,000 x 5%/year x 3/12 of a year

I = $125

Example #2

Sara wants to borrow money from her mother, and she is offered a five-year, non-compounding loan of $7,000, with a 3% annual interest rate. What is Sara’s total interest expense?

I = P x R x T

I = $7,000 x 3%/year * 5 years

I = $1,050

Common Applications of Simple Interest

Simple interest has many real-life applications, such as the following:

#1 Bonds

Bonds pay non-compounding interest in the form of a coupon payment. These coupon payments are not automatically reinvested/compounded and therefore are an example of simple interest.

#2 Mortgages

It may be surprising to learn that most mortgages are based on non-compounding interest. Even though the principal payments vary, the interest is always considered as currently paid in full, and thus there is no compounding effect on the interest itself.

Download the Free Template

Enter your name and email in the form below and download the free template now!

Additional Resources

Thank you for reading CFI’s guide to non-compounding interest. CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional CFI resources will be very helpful:

- Effective Annual Interest RateEffective Annual Interest RateThe Effective Annual Interest Rate (EAR) is the interest rate that is adjusted for compounding over a given period. Simply put, the effective

- Interest PayableInterest PayableInterest Payable is a liability account shown on a company’s balance sheet that represents the amount of interest expense that has accrued

- What is Financial ModelingWhat is Financial ModelingFinancial modeling is performed in Excel to forecast a company's financial performance. Overview of what is financial modeling, how & why to build a model.

- Financial Modeling ResourcesFinancial ModelingFree financial modeling resources and guides to learn the most important concepts at your own pace. These articles will teach you financial modeling best practices with hundreds of examples, templates, guides, articles, and more. Learn what financial modeling is, how to build a model, Excel skills, tips and tricks

-

Basis Point (bp): Understanding Interest Rate Fluctuations

A Basis Point, often referred to as a Beep (using the notation bp), is a measurement of one-hundredth of a percent or one ten-thousandth and is a term commonly used in financeFinance OverviewFinance i

-

Interest Rate Parity Explained: A Comprehensive Guide

Interest rate parity connects the interest rates, spot exchange rates and forward exchange rates in a single comparison. The theory is that the differential between the interest rates of two cou

finance

- Relative Interest Rates: Understanding Their Impact on the Economy

- Debentures Explained: A Comprehensive Guide to Unsecured Corporate & Government Debt

- Understanding Floating Interest Rates: Definition & How They Work

- Understanding Interest Rates: A Comprehensive Guide

- Understanding Interest Rate Risk: Definition & Impact

- Interest Rate Swaps: A Comprehensive Guide

- Interest Rate Collar: Definition, Strategy & Benefits

- Understanding Interest Rate Sensitivity: A Key Concept for Investors

- Interest Rate Caps: Understanding Protection for Adjustable-Rate Loans

-

Interest Rate Call Options: Understanding & Benefits

Interest Rate Call Options: Understanding & BenefitsAn interest rate option is a derivative whose contract value is based on interest rates. There are two types of interest rate options, calls and puts. An interest rate call option gives the individual...

-

Understanding Interest Rate Options: A Comprehensive Guide

Understanding Interest Rate Options: A Comprehensive GuideInterest rate options are a type of derivative that is based on the value of interest rates. They are generally tied to interest rate products like Treasury notes. Interest rate options are generally ...