Understanding Audit Opinions: Types and What They Mean

In the independent auditor’s reportAuditor's ReportAn independent Auditor’s Report is an official opinion issued by an external or internal auditor as to the quality and accuracy of the, an auditor can issue one of five different opinions:

- Clean (unqualified) opinion;

- Qualified opinion due to a GAAP departure;

- Qualified opinion due to a scope limitation;

- Adverse opinion due to a GAAP departure; and

- Disclaimer of opinion due to a scope limitation.

A clean (unqualified) opinion refers to financial statementsAudited Financial StatementsPublic companies are obligated by law to ensure that their financial statements are audited by a registered CPA. The purpose of the that are “presented fairly, in all material respects…”. Deviations from a clean opinion (where the financial statements are not presented fairly) result in a reservation (modification) in the independent auditor’s report.

Summary

- In the independent auditor’s report, an auditor can issue one of five different opinions.

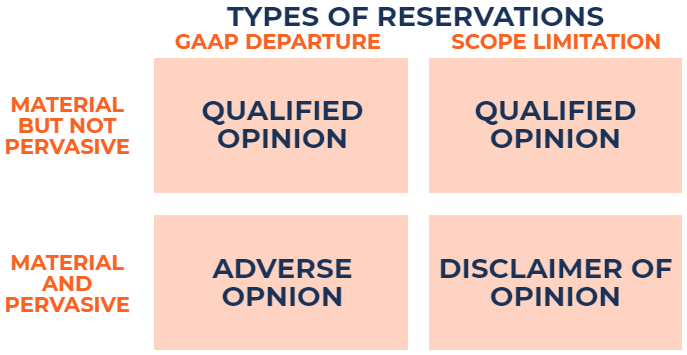

- There are two types of reservations that can be made: a GAAP departure or a scope limitation.

- The opinion issued depends on the type of reservation, which depends upon (1) materiality, and (2) pervasiveness.

Understanding Reservations in an Independent Auditor’s Report

There are two types of reservations:

1. GAAP departure

Situations where the financial statements deviate from the established accounting criteria. For example, a company that uses an incorrect accounting method faces a GAAP departure.

2. Scope limitation

Situations where the auditor is unable to obtain sufficient appropriate audit evidence to base the audit on. This presents a scope limitation.

In addition, the type of opinion, based on the reservation made, depends on two factors:

1. Materiality

Misstatements to the financial statements are considered material if the misstatements (individually or in aggregate), are expected to influence the decisions made by users who rely on the financial statements.

2. Pervasiveness

Misstatements to the financial statements are considered pervasive if the misstatements affect a substantial portion of the financial statements.

What is a Qualified Opinion?

A qualified opinion can be issued due to a GAAP departure or a scope limitation. In both cases, the misstatements are material but not pervasive. In other words, there is a material impact on the financial statements, but the misstatements are not widespread (do not affect a large number of accounts).

Example 1: Qualified opinion due to a GAAP departure

The auditor noticed that the inventory of ABC Company faces a write-down due to obsolescence. However, the company refuses to write down the inventory. In such a scenario, a GAAP departure reservation is made. Since only the inventory and cost of goods soldCost of Goods Sold (COGS)Cost of Goods Sold (COGS) measures the “direct cost” incurred in the production of any goods or services. It includes material cost, direct accounts are wrong, a qualified opinion due to a GAAP departure would be issued.

Example 2: Qualified opinion due to a scope limitation

The auditor wants to send out confirmation letters to customers for the accounts receivable balance as audit evidence. However, ABC Company does not want the auditor to do so. In such a scenario, a scope limitation reservation is made. Since the auditor has been unable to verify the accounts receivable, a qualified opinion due to a scope limitation would be issued.

What is an Adverse Opinion?

An adverse opinion can only be issued due to a GAAP departure. In such a case, the misstatements are both material and pervasive. In other words, there is a material impact on the financial statements, and the misstatements affect a large number of accounts.

Example: Adverse opinion due to a GAAP departure

The auditor believes ABC Company faces a going concernGoing ConcernThe going concern principle assumes that any organization will continue to operate its business for the foreseeable future. The principle purports that every decision in a company is taken with the objective in mind of running the business rather than that of liquidating it. issue and is unable to survive another year. The company disagrees and prepares its financial statements on a historical cost basis instead of on a liquidation basis. In such a scenario, a GAAP departure reservation is made. Since ABC Company prepared its financial statements on a historical cost basis, the majority of the company’s accounts are incorrect. An adverse opinion due to a GAAP departure would be issued.

What is a Disclaimer of Opinion?

A disclaimer of opinion can only be issued due to a scope limitation. In this case, the misstatements are material and pervasive. In other words, the auditor is unable to collect sufficient appropriate audit evidence to base its audit on and, as a result, a large number of accounts are not verifiable.

Example: Disclaimer of opinion due to a scope limitation

The auditor is looking to review the company’s minutes book, which contains important information regarding the board of directors meeting and the audit committee. ABC Company does not permit the auditor to review the minutes book. In such a scenario, a disclaimer of opinion reservation is made. Since the auditor is unable to access the minutes book, a majority of the company’s accounts cannot be verified. A disclaimer of opinion due to a scope limitation would be issued.

Related Readings

CFI offers the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

- Forensic AccountingForensic AccountingForensic accounting is the investigation of fraud or financial manipulation by performing extremely detailed research and analysis of financial information. Forensic accountants are often hired to prepare for litigation related to insurance claims, insolvency, embezzlement, fraud - any type of financial theft.

- IFRS vs. US GAAPIFRS vs. US GAAPThe IFRS vs US GAAP refers to two accounting standards and principles adhered to by countries in the world in relation to financial reporting

- Threats to Auditor IndependenceThreats to Auditor IndependenceIn the auditing profession, there are five major threats that may compromise an auditor’s independence. If an auditor is exposed to a certain

- Top Accounting ScandalsTop Accounting ScandalsThe last two decades saw some of the worst accounting scandals in history. Billions of dollars were lost as a result of these financial disasters. In this

-

Dogs of the Dow: A Dividend Stock Investing Strategy

The Dogs of the Dow refers to a stock-picking strategy that uses the ten highest dividend-yielding stocks from the Dow Jones Industrial Average (DJIA)Dow Jones Industrial Average (DJIA)The Dow Jones I

-

![U.S. Voter Requirements: Eligibility & Registration - [Year]](https://www.etffin.com/article/uploadfiles/202110/2021101111112439_S.png)

U.S. Voter Requirements: Eligibility & Registration - [Year]

To vote in a U.S. election, the basic requirements are simple. You have to be … A United States citizenAt least 18 years old on or before Election DayRegistered to vote by your

Accounting

- Understanding Bank Drafts: Types, Security & How They Work

- Understanding Corporate Stock Classes: Common vs. Preferred

- Understanding Security Types: A Comprehensive Guide

- Understanding Depreciation Methods: A Comprehensive Guide

- Understanding Asset Types: A Comprehensive Guide

- Understanding Liability Types: Current, Non-Current & Contingent

- Understanding Business Structures: A Comprehensive Guide

- Understanding Life Insurance Types: Term vs. Whole Life & More

- Governance Tokens: Risks and Realities in DeFi

-

Understanding the S&P Sectors: A Comprehensive Guide

Understanding the S&P Sectors: A Comprehensive GuideThe S&PS&P – Standard and PoorsStandard & Poor’s is an American financial intelligence company that operates as a division of S&P Global. S&P is a market leader in the ...

-

Understanding SIP Variations: A Comprehensive Guide for Indian Investors

Understanding SIP Variations: A Comprehensive Guide for Indian InvestorsPeople wanting to invest in mutual funds through SIP often know about only the basic SIP. But to meet the investment needs of the investors, fund houses have now introduced different SIP variations. T...