Cost of Goods Sold (COGS): Definition, Calculation & Importance

Cost of Goods Sold (COGS) measures the “direct cost” incurred in the production of any goods or services. It includes material cost, direct labor cost, and direct factory overheads, and is directly proportional to revenue.

As revenue increases, more resources are required to produce the goods or service. COGS is often the second line item appearing on the income statementIncome StatementThe Income Statement is one of a company's core financial statements that shows their profit and loss over a period of time. The profit or, coming right after sales revenue. COGS is deducted from revenue to find gross profit.

Cost of goods sold consists of all the costs associated with producing the goods or providing the services offered by the company. For goods, these costs may include the variable costs involved in manufacturing products, such as raw materials and labor.

They may also include fixed costs, such as factory overhead, storage costs, and depending on the relevant accounting policies, sometimes depreciation expense.

COGS does not include general selling expenses, such as management salaries and advertising expenses. These costs will fall below the gross profit line under the selling, general and administrative (SG&A) expenseSG&ASG&A includes all non-production expenses incurred by a company in any given period. It includes expenses such as rent, advertising, marketing section.

Purpose of Cost of Goods Sold

The basic purpose of finding COGS is to calculate the “true cost” of merchandise sold in the period. It doesn’t reflect the cost of goods that are purchased in the period and not being sold or just kept in inventory. It helps management and investors monitor the performance of the business.

Accounting for Cost of Goods Sold

IFRSIFRS StandardsIFRS standards are International Financial Reporting Standards (IFRS) that consist of a set of accounting rules that determine how transactions and other accounting events are required to be reported in financial statements. They are designed to maintain credibility and transparency in the financial world and US GAAP allow different policies for accounting for inventory and cost of goods sold. Very briefly, there are four main valuation methods for inventory and cost of goods sold.

- First-in-first-out (FIFO)

- Last-in-first-out (LIFO)

- Weighted average

- Specific identification

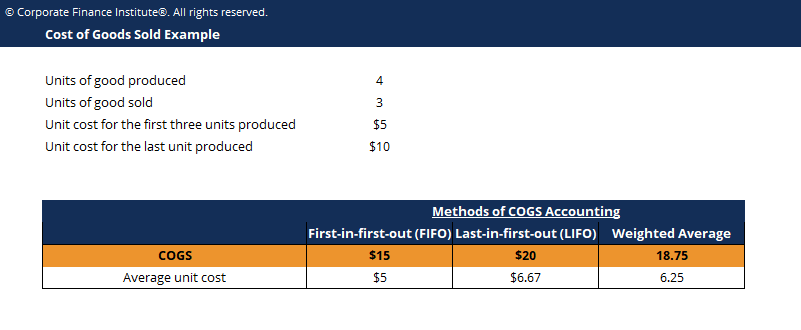

Under FIFO, COGS consists of finished inventory units that were produced first and thus consist of costs incurred first, whereas under LIFO, COGS consists of finished inventory units that were produced last and therefore consists of later or most recent costs. For example, assume that a company purchased materials to produce four units of their goods.

The first three units cost $5 to produce. However, due to rising material prices, the last unit costs $10 to produce. In the subsequent period, the company sold three units. Under FIFO, COGS would consist of the first three units produced, totaling $5 x 3 = $15. Under LIFO, COGS would consist of the last three units produced, totaling $10 x 1 + $5 x 2 = $20.

Under weighted average, the total cost of goods available for sale is divided by units available for sale to find the unit cost of goods available for sale. This is multiplied by the actual number of goods sold to find the cost of goods sold. In the above example, the weighted average per unit is $25 / 4 = $6.25. Thus, for the three units sold, COGS is equal to $18.75.

Specific identification is special in that this is only used by organizations with specifically identifiable inventory. Costs can be directly attributed and are specifically assigned to the specific unit sold. This type of COGS accounting may apply to car manufacturers, real estate developers, and others.

Depending on the COGS classification used, ending inventory costs will obviously differ.

Download the Free Template

Enter your name and email in the form below and download the free template now!

More Resources

Thank you for reading this guide to accounting for the cost of goods sold. CFI is the official provider of the Financial Modeling & Valuation Analyst (FMVA)Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today!®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certificationBecome a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today!. To prepare for the FMVA curriculum, these additional CFI resources will be helpful:

- Fixed and Variable CostsFixed and Variable CostsCost is something that can be classified in several ways depending on its nature. One of the most popular methods is classification according

- Cost of Good ManufacturedCost of Goods Manufactured (COGM)Cost of Goods Manufactured (COGM) is a term used in managerial accounting that refers to a schedule or statement that shows the total

- Job Order Costing GuideJob Order Costing GuideJob Order Costing is used to allocate costs based on a specific job order. This guide will provide the job order costing formula and how to calculate it. As an example, law firms or accounting firms use job order costing because every client is different and unique. Process-costing, on the other hand can be used

- Activity-based Costing GuideActivity-Based CostingActivity-based costing is a more specific way of allocating overhead costs based on “activities” that actually contribute to overhead costs. An activity is

-

Activity Cost Drivers: Definition & Importance for Profitability

An activity cost driver refers to actions that cause variable costsVariable CostsVariable costs are expenses that vary in proportion to the volume of goods or services that a business produces. In oth

-

Understanding Inflation: Causes, Effects & How It Impacts You

Highlights: Inflation occurs when the prices of goods and services increase over a long period of time, causing your purchasing power to decrease. High inflation can occur as the result o

Accounting

- Cost of Goods Sold (COGS): Definition, Calculation & Importance

- Cost of Capital: Definition, Calculation & Importance

- Understanding Allowed Depreciation: Tax Deductions for Businesses

- Understanding Cost of Goods Manufactured (COGM): A Managerial Accounting Guide

- Understanding Inventory: Definition & Importance in Financial Statements

- Marginal Cost: Definition, Calculation & Examples

- Understanding Cost of Goods Sold (COGS): A Key Metric for Profitability

- Cost of Goods Sold (COGS) Deductions: Industries Excluded

- Calculate Cost of Goods Sold (COGS): A Simple Guide for Businesses

-

Understanding Implicit Costs: A Comprehensive Guide

Understanding Implicit Costs: A Comprehensive GuideAn implicit cost is a non-monetary opportunity cost that is the result of a business – rather than incurring a direct, monetary expense – utilizing an asset or resource that it already own...

-

Target Costing: A Comprehensive Guide to Value-Based Pricing

Target Costing: A Comprehensive Guide to Value-Based PricingTarget costing is not just a method of costing, but rather a management technique wherein prices are determined by market conditions, taking into account several factors, such as homogeneous products,...