Cost Recovery Method: Understanding Revenue Recognition

The cost recovery method of revenue recognitionRevenue RecognitionRevenue recognition is an accounting principle that outlines the specific conditions under which revenue is recognized. In theory, there is a is a concept in accounting that refers to a method in which a business does not recognize profit related to a sale until the cash collected exceeds the cost of the good or service sold. In other words, using this method, profits are only recognized when cash payments have recovered the seller’s cost.

Intuition Behind the Cost Recovery Method

The cost recovery method is a method of revenue recognition in which there is uncertainty. Therefore, it is used to account for revenue when revenue streams from a sale cannot be accurately determined. Accounting standards IAS 18 require a company to recognize revenue only when the amount is measurable and cash flows are probable. The underlying concept behind this method is as follows:

Net profit is not recognized until the cash collected exceeds the cost of the item and/or service sold.

Example

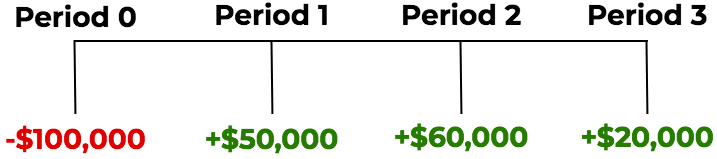

Shiny Clothes Ltd. is a retail store that recently purchased inventory costing $100,000. The retail store sells its inventoryInventoryInventory is a current asset account found on the balance sheet, consisting of all raw materials, work-in-progress, and finished goods that a to multiple customers for a total sale price of $130,000 – implying a $30,000 profit. The sales were made on credit, and Shiny Clothes Ltd. does not know the recovery rate of their sales to customers. The company decides to use the cost recovery method to recognize revenue.

The retail store made sales of $100,000 in period 0 and received cash flows from sales of $50,000, $60,000, and $20,000 in the following three periods, respectively. The cash flows from the sale of $100,000 inventory are shown as follows:

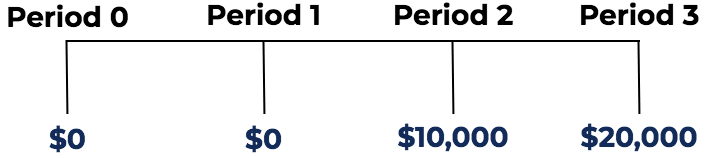

Recall that costs must be covered before any profit is recognized. In the scenario above, Shiny Clothes Ltd. would start recognizing profit in period 2 when the money inflow exceeds the cost of the sale. Profit for the sale of inventory under the cost recovery method would be recognized as follows:

Journal Entries for the Cost Recovery Method

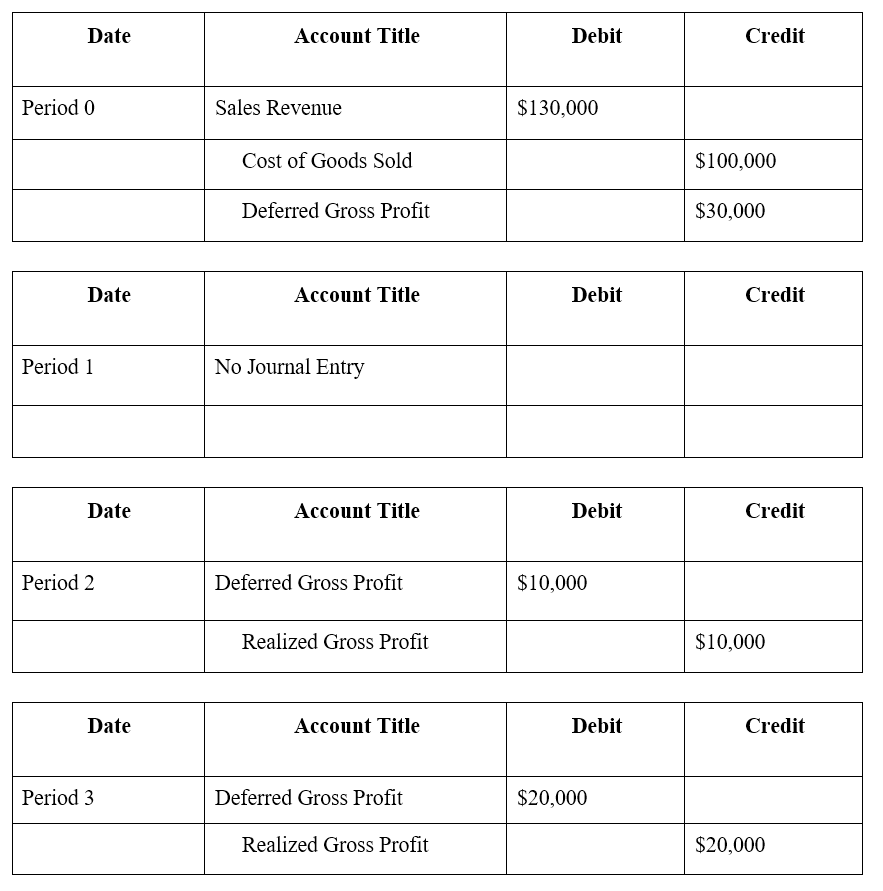

With reference to the example above, the journal entriesJournal Entries GuideJournal Entries are the building blocks of accounting, from reporting to auditing journal entries (which consist of Debits and Credits) for Shiny Clothes Ltd for the sale of $100,000 worth of inventory would be as follows:

Learn more with CFI’s Free Accounting Courses.

Impact of the Cost Recovery Method on a Company’s Earnings

If we accounted for the sale by Shiny Clothes Ltd. as a regular sale, the amount of profit recognized would be $30,000 in period 0. It would result in an immediate impact on a company’s earnings:

Period 1: +$30,000 in earnings

However, with the cost recovery method, there is uncertainty in the collection of money resulting from the sale. Therefore, no earnings will be recognized until the cash inflows exceed the cost. In the example above with Shiny Clothes Ltd., under the cost recovery method, the company’s earnings will be impacted as follows:

- Period 0: No effect

- Period 1: No effect

- Period 2: +$10,000 in earnings

- Period 3: +$20,000 in earnings

Additional Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today!®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Analysis of Financial StatementsAnalysis of Financial StatementsHow to perform Analysis of Financial Statements. This guide will teach you to perform financial statement analysis of the income statement,

- Cash Flow StatementCash Flow StatementA cash flow Statement contains information on how much cash a company generated and used during a given period.

- Deferred RevenueDeferred RevenueDeferred revenue is generated when a company receives payment for goods and/or services that it has not yet earned. In accrual accounting,

- Accounting Fundamentals Course

-

Marginal Cost: Definition, Calculation & Examples

Marginal cost represents the incremental costs incurred when producing additional units of a good or service. It is calculated by taking the total change in the cost of producing more goods and dividi

-

Nonaccrual Experience Method (NAE): Definition & Eligibility

The nonaccrual experience method (NAE) is a tax accounting procedure that the Internal Revenue Code (IRC) uses for handling bad debts. The procedure can only be applied to bad debts for services that

Accounting

- Bitcoin Mining Costs: A Comprehensive Breakdown (2024)

- Understanding the Cost of Preferred Stock: A Key Capital Metric

- Direct Capitalization Method: Definition & Application

- Understanding the Completed Contract Method: Revenue Recognition Explained

- Consolidation Method Explained: A Comprehensive Guide

- Cost Method Explained: Accounting & Investment Strategies

- Direct Method for Cash Flow Statements: A Comprehensive Guide

- High-Low Method: Understanding & Application in Cost Accounting

- Variable Cost Ratio: Definition, Calculation & Importance

-

Understanding Accounting Methods: Cash vs. Accrual

Understanding Accounting Methods: Cash vs. AccrualAn accounting method refers to a set of rules that a company adheres to when keeping its financial records and reporting financial transactions. The transactions are recorded in a manner that accurate...

-

Understanding the Annualized Income Installment Method (AIIM)

Understanding the Annualized Income Installment Method (AIIM)The Annualized Income Installment Method (AIIM) is a method used to calculate the amount of taxes payable by a business during a tax year. Taxes are typically paid in installments quarterly, but some ...