Target Costing: A Comprehensive Guide to Value-Based Pricing

Target costing is not just a method of costing, but rather a management technique wherein prices are determined by market conditions, taking into account several factors, such as homogeneous products, level of competition, no/low switching costsCost of Goods Manufactured (COGM)Cost of Goods Manufactured (COGM) is a term used in managerial accounting that refers to a schedule or statement that shows the total for the end customer, etc. When these factors come into the picture, management wants to control the costs, as they have little or no control over the selling priceAccountingOur Accounting guides and resources are self-study guides to learn accounting and finance at your own pace. Browse hundreds of guides and resources..

CIMA defines target cost as “a product cost estimate derived from a competitive market price.”

Target Costing = Selling Price – Profit Margin

Why Target Costing?

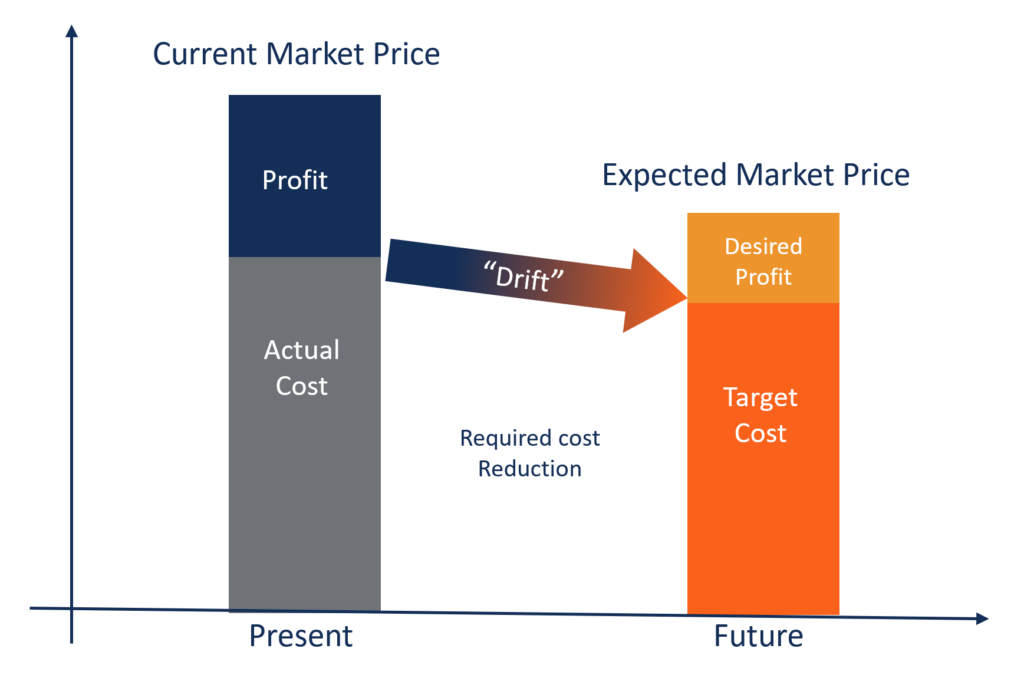

In industries such as FMCG (Fast Moving Consumer Goods), construction, healthcare, and energy, competition is so intense that prices are determined by supply and demand in the market. Producers can’t effectively control selling prices. They can only control, to some extent, their costs, so management’s focus is on influencing every component of product, service, or operational costs.

The key objective of target costing is to enable management to use proactive cost planning, cost management, and cost reduction practices where costs are planned and calculated early in the design and development cycle, rather than during the later stages of product development and production.

Key Features of Target Costing:

- The price of the product is determined by market conditions. The company is a price taker rather than a price maker.

- The minimum required profit margin is already included in the target selling price.

- It is part of management’s strategy to focus on cost reduction and effective cost management.

- Product design, specifications, and customer expectations are already built-in while formulating the total selling price.

- The difference between the current cost and the target cost is the “cost reduction,” which management wants to achieve.

- A team is formed to integrate activities such as designing, purchasing, manufacturing, marketing, etc., to find and achieve the target cost.

Advantages of Target Costing:

- It shows management’s commitment to process improvements and product innovation to gain competitive advantages.

- The product is created from the expectation of the customer and, hence, the cost is also based on similar lines. Thus, the customer feels more value is delivered.

- With the passage of time, the company’s operations improve drastically, creating economies of scale.

- The company’s approach to designing and manufacturing products becomes market-driven.

- New market opportunities can be converted into real savings to achieve the best value for money rather than to simply realize the lowest cost.

Example:

ABC Inc. is a big FMCG player that operates in a very competitive market. It sells packaged food to end customers. ABC can only charge $20 per unit. If the company’s intended profit margin is 10% on the selling price, calculate the target cost per unit.

Solution:

Target Profit Margin = 10% of 20 = $2 per unit

Target Cost = Selling Price – Profit Margin ($20 – $2)

Target Cost = $18 per unit

Download the Free Template

Enter your name and email in the form below and download the free template now!

Related Reading

CFI is the official global provider of the Financial Modeling and Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification, designed to transform anyone into a world-class financial analyst.

If you’re interested in advancing your career in corporate finance, these CFI articles will help you on your way:

- Cost of Goods ManufacturedCost of Goods Manufactured (COGM)Cost of Goods Manufactured (COGM) is a term used in managerial accounting that refers to a schedule or statement that shows the total

- Fixed and Variable CostsFixed and Variable CostsCost is something that can be classified in several ways depending on its nature. One of the most popular methods is classification according

- Contribution MarginContribution MarginContribution margin is a business’ sales revenue less its variable costs. The resulting contribution margin can be used to cover its fixed

- Marginal Cost FormulaMarginal Cost FormulaThe marginal cost formula represents the incremental costs incurred when producing additional units of a good or service. The marginal cost

-

Understanding Cost of Production: A Comprehensive Guide

Cost of production refers to the total cost incurred by a business to produce a specific quantity of a product or offer a service. Production costs may include things such as labor, raw materials, or

-

Understanding Cost Structure: Fixed vs. Variable Costs

Cost structure refers to the various types of expenses a business incurs and is typically composed of fixed and variable costsFixed and Variable CostsCost is something that can be classified in severa

Accounting

- Cost of Capital: Definition, Calculation & Importance

- Absorption Costing: A Comprehensive Guide for Businesses

- Understanding Allowed Depreciation: Tax Deductions for Businesses

- Backflush Costing: Definition, Benefits & Implementation

- Capitalized Costs Explained: Definition & Examples

- Cost Allocation: Definition, Methods & Importance

- Cost Drivers: Understanding What Impacts Your Business Expenses

- Depreciated Cost Explained: Calculation & Importance

- Marginal Cost: Definition, Calculation & Examples

-

Activity-Based Budgeting (ABB): A Comprehensive Guide

Activity-Based Budgeting (ABB): A Comprehensive GuideActivity-based budgeting (ABB) is a budgeting method where activities are thoroughly analyzed to predict costs. ABB does not take historical costs into account when creating a budget. Summa...

-

Cost of Equity: Definition, Calculation & Importance

Cost of Equity: Definition, Calculation & ImportanceCost of Equity is the rate of return a company pays out to equity investors. A firm uses cost of equity to assess the relative attractiveness of investments, including both internal projects and exter...