Held-to-Maturity Securities: Definition & Key Differences

Held to maturity securities are securities that companies purchase and intend to hold until they mature. They are unlike trading securitiesTrading SecuritiesTrading securities are securities purchased by a company for the purpose of realizing a short-term profit. The securities are issued within the company's industry, or available for sale securitiesAvailable for Sale SecuritiesAvailable for sale securities are the default categorization of securities that companies decide to invest in for the purposes of benefiting their financial position. Unlike trading securities, available for sale securities are not bought or sold for the sole purpose of realizing a short-term capital gain., where companies don’t usually hold on to securities until they reach maturity.

Companies mostly use held to maturity securities to protect themselves against interest rate fluctuations, diversify their investment portfolios, and realize a small, low-risk capital gain over a longer period of time. The investments usually comprise debt instruments, such as government bonds or corporate bondsBondsBonds are fixed-income securities that are issued by corporations and governments to raise capital. The bond issuer borrows capital from the bondholder and makes fixed payments to them at a fixed (or variable) interest rate for a specified period..

Pros and Cons of Held to Maturity Securities

Pros

- Securities that are to be held until maturity are usually very low risk. Assuming that the bond issuer does not default, returns are essentially guaranteed.

- They are not susceptible to news events or industry trends since the returns on a bond are already pre-specified at the time of purchase (i.e., the coupon payments, face value, and maturity date).

- Investors can plan their investment portfolios for the long term and count on bonds as lower-betaBeta CoefficientThe Beta coefficient is a measure of sensitivity or correlation of a security or an investment portfolio to movements in the overall market. securities that will diversify the risk that their portfolio faces.

Cons

- Held to maturity securities bite into the company’s liquidity. Since companies make the commitment to hold these securities until maturity, they cannot really count on these securities to be sold if cash is needed in the short term.

- As discussed above, the returns on these securities are pre-determined, meaning that while there is downside protection, there is limited upside potential. If financial markets generally go up, the company’s returns will not be positively affected.

Accounting Treatment

The biggest difference between held to maturity securities and the other security types mentioned above is their accounting treatment. As opposed to being recorded and updated on the company’s balance sheet according to the security’s fair market value, held to maturity securities are recorded at their original purchase cost. It means that from one accounting period to another, the value of the securities on the company’s balance sheet will remain constant.

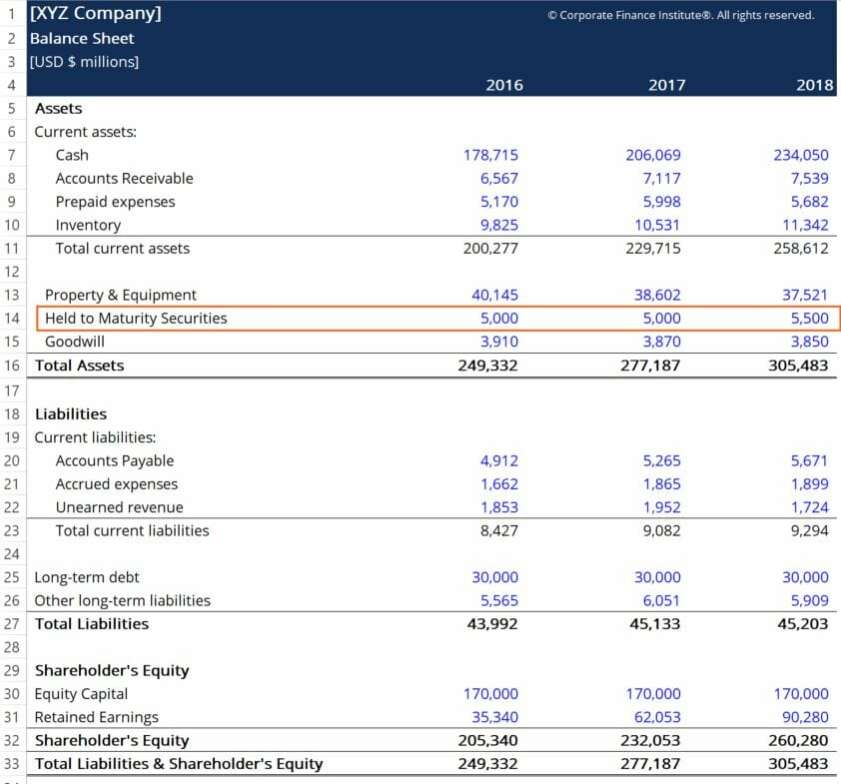

Any gains or losses resulting from changes in interest ratesInterest RateAn interest rate refers to the amount charged by a lender to a borrower for any form of debt given, generally expressed as a percentage of the principal. (for bonds and other debt instruments) will be recorded when the securities reach maturity. Below is an example of how a 2-year bond will appear on a company’s balance sheet:

Upon purchase, the offsetting account will likely be cash, as the company likely bought the securities with cash. Here, we can see that no changes are recorded in the 2017 accounting period, despite any changes in the security’s fair value during that time period. For example, if interest rates fell sharply in 2016, which would cause a rise in the bond’s market value, there was no accounting of the change in the company’s balance sheet.

In 2018, the company saw a net addition of $500 million in held to maturity securities, which was likely a purchase of additional securities.

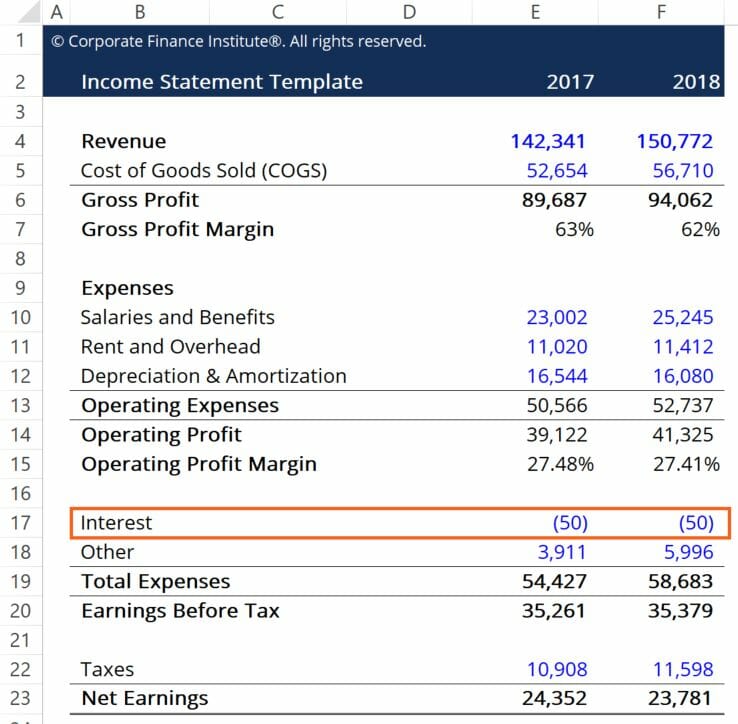

Interest payments made to the debt-holding company will appear in the company’s income statement on a periodic basis. Let’s assume that the bonds pay a 10% annual coupon rate, which equates to $50 million in additional income each year. Here’s how this would look on a company’s income statement:

Here, we can see how the 10% coupon is captured in the interest line item. For simplicity, it is assumed that the company does not have any other interest revenues. The interest income from coupon payments is recorded as a credit or negative expense in the Total Expenses grouping of the Income Statement.

Additional Resources

CFI offers the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To learn more about related topics, check out the following CFI resources:

- Budgeting and Forecasting Course – CFI

- Accounting Fundamentals Course – CFI

- IFRS StandardsIFRS StandardsIFRS standards are International Financial Reporting Standards (IFRS) that consist of a set of accounting rules that determine how transactions and other accounting events are required to be reported in financial statements. They are designed to maintain credibility and transparency in the financial world

- Cash Flow Statement Cash Flow StatementA cash flow Statement contains information on how much cash a company generated and used during a given period.

-

Disgorgement Explained: Legal Remedy for Illegal Profits

In legal terms, disgorgement is an action where something is given up – namely, profits – because they have been obtained illegally or unethically. The court system orders the individual o

-

Understanding Held Orders: A Quick Guide for Traders

A held order refers to a market order that should be executed promptly with no hesitation. When a trader receives instructions by way of a held order, implementation time is instant, as the order need

Accounting

- Marketable Securities: Definition & Types | [Your Brand/Company Name]

- Capital Markets Explained: Investing in Equity & Debt

- Commodity-Linked Securities: Explained | Investment Guide

- Understanding Distressed Securities: Risks & Opportunities

- Hybrid Securities: A Comprehensive Guide to Balanced Investments

- Non-Marginable Securities: Definition & Investing Implications

- Understanding Equity Issuance Fees: Costs of Raising Capital

- Trading Securities: Definition, Types & Short-Term Investment Strategies

- Securities Explained: A Beginner's Guide to Stocks, Bonds & More

-

Understanding Depositories: Secure Storage for Financial Securities

Understanding Depositories: Secure Storage for Financial SecuritiesA Depository refers to a place or entity that holds financial securities in a dematerialized form. A bank, organization, or any institution holding and assisting in security trading is referred to as ...

-

Private REITs vs. Publicly Traded REITs: A Comprehensive Comparison

Private REITs vs. Publicly Traded REITs: A Comprehensive ComparisonThe article below covers private REITs vs publicly traded REITs. Real estate investment trusts (REITs) can be classified into either private or public, traded or non-traded. REITs specifically invest ...