Modified Accrual Accounting: A Comprehensive Guide

Modified accrual accounting refers to an accounting method that combines cash-basis accounting and accrual-basis accounting. It follows the cash-basis method to record short-term events and follows the accrual method to record long-term events.

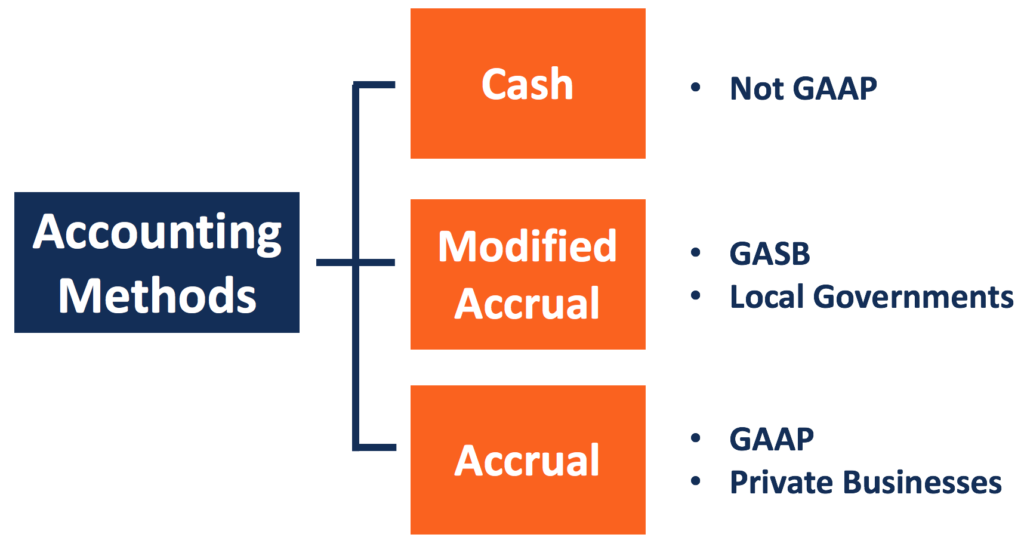

The modified accrual method of accounting is created by the Government Accounting Standards Board (GASB). It does not comply with the Generally Accepted Accounting Principles (GAAP)GAAPGAAP, Generally Accepted Accounting Principles, is a recognized set of rules and procedures that govern corporate accounting and financial or the International Financial Reporting Standards (IFRS).

Summary

- Modified accrual accounting follows the cash-basis method to record short-term events. It follows the accrual method to record long-term events.

- The modified accrual accounting method recognizes revenues when they are available and measurable. It recognizes expenditures as they are incurred.

- The method does not comply with GAAP, so it is not used by public companies.

Basic Rules of Modified Accrual Accounting

The modified accrual accounting combines the features of the cash method and the accrual method. Under the cash method of accounting, revenues, and expenses are recorded when the cash is received or paid.

Under the accrual method, revenues are recorded when they are earned (goods or services are delivered), and expenses are recorded when they are incurred (products are consumed). Modified accrual accounting distinguishes short-term and long-term events and recognizes them in different ways.

Short-Term Events

Modified accrual accounting follows cash-basis accounting to report short-term events. The short-term items on the balance sheet include account receivables, inventory, and account payables. The economic events that affect the items are regarded as short-term events.

The events are recorded when the cash balance is changed. Therefore, almost all the income statement items are recorded in cash-basis accounting. The short-term assets and liabilities are no longer recorded on the balance sheet.

Long-Term Events

Fixed assetsFixed AssetsFixed assets refer to long-term tangible assets that are used in the operations of a business. They provide long-term financial benefits (PP&E) and long-term debts are some examples of long-term assets and liabilities. In contrast to short-term events, economic events that affect the items, or affect more than one accounting period, are known as long-term events.

Modified accrual accounting treats long-term events as accrual accounting does. Long-term assets and liabilities are recorded on the balance sheet. DepreciationDepreciation MethodsThe most common types of depreciation methods include straight-line, double declining balance, units of production, and sum of years digits., amortization, and debt repayments are reported over the life of the assets and debts.

However, there are some differences between modified accrual accounting and full accrual accounting in terms of recognizing the current portion of long-term debt. In full accrual accounting, the portion is recognized in the period and value when it is incurred. Modified accrual accounting recognizes the current portion of long-term debt as it matures. It can also be reported to the extent of liquidation with available financial resources that are expendable.

Revenues and Expenditures

Modified accrual accounting recognizes revenues when they are available and can be reasonably estimated. Revenues are available when they can finance the current expenditures paid within 60 days. Expenditures are reported in the same way as accrual accounting. They are recognized in the period when they are incurred, regardless of when the cash payments take place.

Some items take on different names in modified accrual accounting. For example, net incomeNet IncomeNet Income is a key line item, not only in the income statement, but in all three core financial statements. While it is arrived at through is named as excess or deficiency, and expenses are named as expenditures.

Modified Accrual Accounting and the GASB

Like the cash-basis accounting method, modified accrual accounting does not comply with the GAAP or IFRS. Thus, for-profit public companies do not use the cash-basis method; some may use it for internal reference.

Modified accrual accounting is set by the GASB with the purpose to measure the current-year revenues, expenditures, and financial resources in government funds.

The accounting purpose and requirements of government agencies are different from those of non-governmental entities. A company uses the accrual method to record its business activities and show its financial health to stakeholders more accurately.

A local government agency focuses on reflecting whether the current-year revenues are enough to cover the current-year expenditure. It tells whether the government is experiencing a surplus or deficit. A government agency should also be able to track whether it is using its financial resources according to the budget plan. The modified accrual method can meet such requirements.

By recording short-term events on a cash basis, the modified accrual method reflects the recent revenues and expenditures more clearly. The government agency can also categorize the fund into its internal entities. It helps the local government to better track whether it is spending the money as planned. It is also easier for the government to adjust its budget.

More Resources

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

- Accrued ExpenseAccrued ExpenseAccrued expense is a concept in accrual accounting that refers to expenses that are recognized when incurred but not yet paid. In some

- IFRS vs US GAAPIFRS vs. US GAAPThe IFRS vs US GAAP refers to two accounting standards and principles adhered to by countries in the world in relation to financial reporting

- Nonaccrual Experience Method (NAE)Nonaccrual Experience Method (NAE)The nonaccrual experience method (NAE) is a tax accounting procedure that the Internal Revenue Code (IRC) uses for handling bad debts.

- Projecting Income Statement Line ItemsProjecting Income Statement Line ItemsWe discuss the different methods of projecting income statement line items. Projecting income statement line items begins with sales revenue, then cost

-

Modified Cash Basis Accounting: A Comprehensive Guide

Modified cash basis refers to an accounting method that utilizes the features of both the accrual and cash basis methods. It is also called hybrid accounting, where the cash basis of accounting is use

-

Payroll Accounting: A Comprehensive Guide for Businesses

Payroll accounting is essentially the calculation, management, recording, and analysis of employees’ compensationRemunerationRemuneration is any type of compensation or payment that an individua

Accounting

- Accounting Explained: Understanding Financial Records & Reporting

- Accounting Conservatism: Definition, Examples & Importance

- Accounting vs. Tax Depreciation: Key Differences Explained

- Understanding Accounting Income: A Key Financial Metric

- Understanding Accounting Methods: Cash vs. Accrual

- Accrual Accounting Explained: A Comprehensive Guide

- Accrual Accounting Principle: Definition & Explanation

- Hedge Accounting Explained: A Comprehensive Guide

- Understanding Inflation Accounting: A Guide for Multinational Corporations

-

Free Accounting Software: A Comprehensive Guide for Businesses

Free Accounting Software: A Comprehensive Guide for BusinessesFree accounting software provides businesses from sole proprietors to and small- and medium-sized enterprises (SMEs)Small and Medium-sized Enterprises (SMEs)SMEs, or small and medium-sized enterprises...

-

Managerial Accounting: Definition, Uses, and Differences from Financial Accounting

Managerial Accounting: Definition, Uses, and Differences from Financial AccountingManagerial accounting (also known as cost accounting or management accounting) is a branch of accounting that is concerned with the identification, measurement, analysis, and interpretation of account...