Understanding Minimum Lease Payments: Definition & Importance

The minimum lease payment is the minimum amount a lessee can pay over the term or lifetime of the lease. The present value of minimum lease payments determines the value of the lease, which is then recorded in the accounting books of a company.

Minimum lease payments are also very important in determining the classification of the lease – whether it should be an operating lease or a capital lease. It is important because an operating leaseOperating LeaseAn operating lease is an agreement to use and operate an asset without ownership. Common assets that are leased include real estate, is treated as an expense and would not be included in the assets of a company, whereas a capital lease would be included in the assets of a company. Minimum lease payments are integral for the accounting practices of a company and a key part of corporate accounting.

Minimum Lease Payments and Accounting Standard Setting Boards

The method for calculating minimum lease payments varies with different accounting standard setting boards, along with the classification of a lease being a capital lease or operating leaseCapital Lease vs Operating LeaseThe difference between a capital lease vs operating lease - A capital lease (or finance lease) is treated like an asset on a company’s. Furthermore, classification standards of operating leases and capital leases are frequently revised. It is recommended that you visit the appropriate accounting standard board’s website to stay up-to-date on current regulations.

How to Calculate a Minimum Lease Payment?

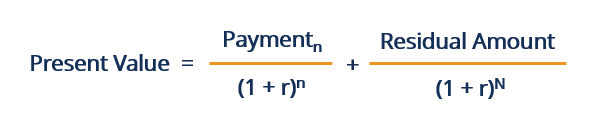

One method of calculating the present value of minimum lease payments is below:

Where:

- PV – Present Value of minimum lease payment

- Paymentn – The lease payment for period n

- r – The corresponding interest rate

- Residual Amount – Estimated value of asset once the lease is over

- N – The total amount of periods in the lease contract

Conclusively, the present value of the minimum lease payment is simply the sum of all of the lease payments that are to be made in the future, in today’s dollar terms, added to the value of the estimated value of the leased asset once the lease is over.

The reason the payments and residual amount is divided by 1 plus the interest rate adjusted for time, is to bring the terms into today’s dollars. To adjust for the timing of the payments and residual amount, you must power the term (1+r) to the value of the period in which the payment and/or the residual amount occurs.

Numerical Example

A numerical example of a minimum lease payment is very useful to understand the workings of the equation above.

The following is an example:

- Three-year lease

- Annual payments of $100

- Annual interest rate of 5%

- Residual amount of $50

PV of Payment 1: $100 / (1 + 5%) = $95.24

PV of Payment 2: $100 / [(1 + 5%) ^ 2] = $90.70

PV of Payment 3: $100 / [(1+5%) ^ 3] = $86.38

Sum of PV’s: $95.24 + $90.70 + $86.38 = $272.32

PV of Residual Amount: $50 / [(1 + 5%) ^ 3] = $43.19

PV of Minimum Lease Payment: $43.19 + $272.32 = $315.51

In the example above, we first take the present value of all of the annual lease payments individually. Then, we add them. Finally, we take the present value of the residual amount and add that to the sum of the present value of the annual lease payments.

It is important to notice the periodicity of the annual lease payments and the terms in which the interest rate is stated in. In such a case, the interest rate is stated in an APR (annual percentage rate) format.

The lease payments are also annual. Thus, no adjustments to the interest rate are needed. However, if the given interest rate was semi-annual or the lease payments were semi-annual, you would need to adjust the interest rate. A general rule of thumb is to match the periodicity of the interest rate to that of the periodicity of the lease payments.

Minimum Lease Payment Using Annuities

Calculating the present value of minimum lease payments can also be achieved using an annuityAnnuityAn annuity is a financial product that provides certain cash flows at equal time intervals. Annuities are created by financial institutions, primarily life insurance companies, to provide regular income to a client. formula. It holds because the periodicity of the lease payments is typically evenly spaced out. Below is an example of using an annuity to solve the above problem.

PV of Annuity of Annual Lease Payments: $100 * [1– (1+ 5%) ^ (-3)] / 5% = $272.32

PV of Residual Amount: $50 / [(1 + 5%) ^ 3] = $43.19

PV of Minimum Lease Payment: $43.19 + $272.32 = $315.51

Related Readings

CFI offers the Capital Markets & Securities Analyst (CMSA)™Program Page - CMSAEnroll in CFI's CMSA® program and become a certified Capital Markets &Securities Analyst. Advance your career with our certification programs and courses. certification program for those looking to take their careers to the next level. To keep learning, the following readings will be helpful:

- Lease AccountingLease AccountingLease accounting guide. Leases are contracts in which the property/asset owner allows another party to use the property/asset in exchange for money or other assets. The two most common types of leases in accounting are operating and financing (capital leases). Advantages, disadvantages, and examples

- Net Present Value (NPV)Net Present Value (NPV)Net Present Value (NPV) is the value of all future cash flows (positive and negative) over the entire life of an investment discounted to the present.

- Lease ClassificationsLease ClassificationsLease classifications include operating leases and capital leases. A lease is a type of transaction undertaken by a company to have the right to use an asset. In a lease, the company will pay the other party an agreed upon sum of money, not unlike rent, in exchange for the ability to use the asset.

- Lessor vs. LesseeLessor vs LesseeThere are two principal parties in a lease agreement, and every finance professional needs to know how to differentiate between the lessor vs

-

Balloon Payments on Car Leases: Explained & Should You Choose One?

A balloon payment is a larger-than-normal payment due at the end of a lease or loan. Similar to an actual balloon, your payment at the end of your lease or loan becomes “inflated”

-

Electronic Payments: Powering Global E-commerce Growth

In 2019, global online retail sales hit the 3 trillion-dollar mark. In 2020, e-retail became a lifeline for millions of people navigating lockdowns. Businesses throughout the world have had to rethi

Accounting

- Understanding Arrears: Definition, Causes & Management

- Automatic Bill Payment: A Comprehensive Guide

- Understanding Down Payments: A Comprehensive Guide

- Understanding Minimum Monthly Payments: A Comprehensive Guide

- Principal Payments Explained: Understanding Loan Repayment

- Stop Payment Orders: Definition, Process & How to Request

- Understanding Leases: Types, Classifications, and Key Concepts

- Net Lease Explained: Understanding Landlord & Tenant Responsibilities

- Operating Lease Explained: Benefits & How They Work

-

Single Payment Loans: Definition, How They Work & Key Features

Single Payment Loans: Definition, How They Work & Key FeaturesA single payment loan is a type of loan that is commonly offered in the banking industry today. Here are the basics of the single payment loan and how it works. Single Payment Loan With a single...

-

Medical Payments Coverage: What It Is & How It Protects You

Medical Payments Coverage: What It Is & How It Protects YouIf you or your passengers are injured in a car accident, medical payments coverage can help you pay for the medical expenses — no matter who’s at fault. Medical payments coverage —...