Net Income After Tax (NIAT): Definition & Importance

Net income after tax (NIAT) is an entity’s profits after deducting all expenses and taxes in a fiscal period. NIAT is also commonly referred to as a company’s bottom-line profitability.

Summary

- Net income after tax (NIAT) is an entity’s profits after deducting all expenses and taxes. It is also referred to as bottom-line profitability.

- NIAT is frequently used in ratio analysis to identify the company’s profitability.

- Net income after tax is either reinvested back into the company, paid out in dividends, or is used to acquire treasury stock.

How to Calculate Net Income After Tax?

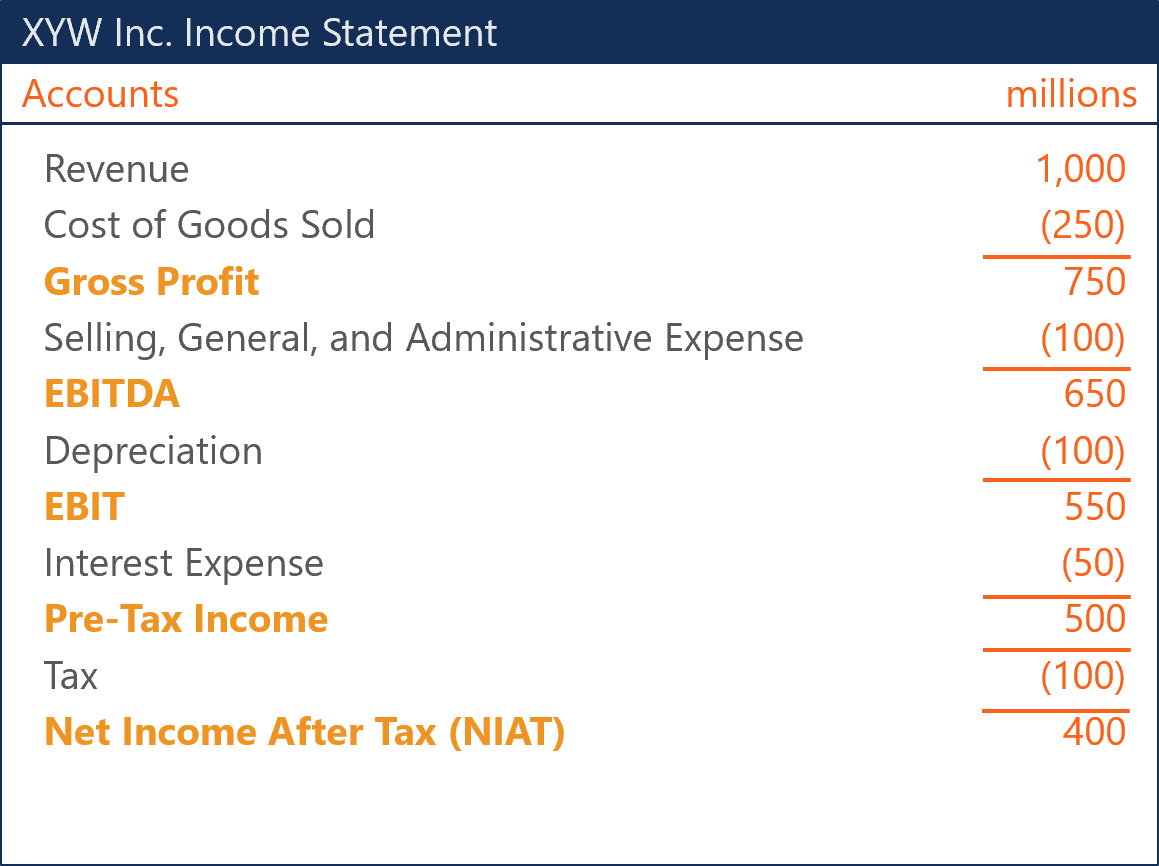

Calculating net income after tax involves deducting all expenses and costs from revenues in a given fiscal period. The expenses and costs are the following:

Cost of Goods Sold (COGS)

The cost of goods sold (COGS) is the carrying value of goods sold in a given period. Recording the cost of goods sold is dependent on the applied inventory valuation method. Generally accepted accounting principles (GAAP)GAAPGAAP, Generally Accepted Accounting Principles, is a recognized set of rules and procedures that govern corporate accounting and financial dictate that inventory can be valued via the specific identification method, average cost basis, or first-in-first-out method.

Selling, General, and Administrative (SG&A) Expense

SG&A expense consists of the direct costs, indirect costs, and overhead costs that are instrumental for the company’s day to day operations. For example, commissions, salaries, insurance, and supplies are also examples of selling, general, and administrative expenses. Alternatively, the SG&A account is also referred to as operating expenses.

Depreciation

The acquisition of tangible assetsTangible AssetsTangible assets are assets with a physical form and that hold value. Examples include property, plant, and equipment. Tangible assets are like PP&E deteriorate with use and eventually wear out. Accountants try to best allocate this deterioration cost across the asset’s useful life in order to faithfully represent the asset’s value.

Interest Expense

Interest expense refers to the cost of borrowing for the debtor. It is accrued and expensed over time. Each debt payment is made up of principal repayment and interest expense.

Net Income After Tax in Ratio Analysis

Net income after tax is often used in relation to other account balances to interpret the company’s ability to generate profit. There are primarily two ways net income after tax is used in an analysis to interpret a company’s profitability.

Firstly, through the calculation of return ratios, analysts can quantify a company’s ability to generate profit given asset investments and equity financing. Secondly, profitability can be assessed relative to revenues generated.

Return on Assets

Return on assets (ROA) shows the ratio of net income after tax relative to the company’s total asset balance over a given period. The application of ROA expresses how much after-tax profit a company earns for every dollar of assets it holds. The lower the after-tax profit is relative to the total asset balance, the more intensive the assets are.

Return on Equity

Return on equity (ROE) expresses net income after tax as a ratio of shareholder’s equity over a given period. ROE is simply the rate of return the company generates with its equity capital raising. It is frequently used in profitability analysis to indicate a company’s ability to generate profits without utilizing debt.

Net Profit Margin

Net profit margin refers to a company’s bottom-line profitability. It is the ratio of net income after tax over total sales over a given period. A net profit margin indicates what percentage of revenues are profit, and therefore, demonstrates how efficient a company is in converting sales to after-tax profits.

What is Net Income After Tax Used For?

There are three primary ways net income after tax is used:

1. Reinvestment

Companies can choose to reinvest net income after tax back into the company. It often signifies to investors of a company’s strong growth prospects. Specifically, investors believe that the company is holding positive net present value projects in its pipeline and can generate further returns on their investment.

2. Dividends

Dividends can be a very attractive characteristic of equity ownership for investors who value cash flows rather than growth prospects. Furthermore, a company that pays consistent dividends is generally very stable. However, some investors see dividend payouts to symbolize that the company lacks positive net present value projects in its pipeline.

3. Share Repurchase

Repurchasing stock is known as negative share issuance, and the shares are held in the company’s treasury. An increase in treasury stock indicates a reduction in the number of shares outstanding.

There are two primary reasons why a company would purchase its own shares on the secondary marketSecondary MarketThe secondary market is where investors buy and sell securities from other investors. Examples: New York Stock Exchange (NYSE), London Stock Exchange (LSE).. Firstly, the company could be trying to fend off other companies from taking a controlling equity stake. Secondly, the company may believe the shares are trading at a discount and buying them will create more shareholder value then investing in internal projects.

Additional Resources

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

- Treasury StockTreasury StockTreasury stock, or reacquired stock, is a portion of previously issued, outstanding shares of stock that a company repurchased from shareholders.

- Dividend vs Share Buyback/RepurchaseDividend vs Share Buyback/RepurchaseShareholders invest in publicly traded companies for capital appreciation and income. There are two main ways in which a company returns profits to its shareholders – Cash Dividends and Share Buybacks. The reasons behind the strategic decision on dividend vs share buyback differ from company to company

- Ratio AnalysisRatio AnalysisRatio analysis refers to the analysis of various pieces of financial information in the financial statements of a business. They are mainly used by external analysts to determine various aspects of a business, such as its profitability, liquidity, and solvency.

- Net Present Value (NPV)Net Present Value (NPV)Net Present Value (NPV) is the value of all future cash flows (positive and negative) over the entire life of an investment discounted to the present.

-

Understanding Net Monthly Income: Definition & Calculation

Your net pay is the amount you take home after all deductions. Net income is the amount of a person's paycheck that remains after the employer withholds taxes and deductions. Self-employe

-

EBT vs. Pretax Income: Understanding the Difference

Actually, there is no difference between earnings before tax (EBT) vs pretax income. Both terms denote the same concept and can be used interchangeably.Essentially, EBT or pretax income is a measure o

Accounting

- Understanding After-Tax Operating Income (ATOI): Definition & Significance

- Understanding Federal Income Tax: A Comprehensive Guide

- Understanding Income Tax: A Comprehensive Guide for Individuals & Businesses

- Understanding Net of Tax: Definition & Calculation

- Annualized Income: Definition, Calculation & Tax Implications

- Negative Income Tax: A Comprehensive Explanation

- Understanding Net Income: A Comprehensive Guide

- Understanding Net Operating Loss (NOL) Deductions | IRS.gov

- Net Income Explained: A Comprehensive Guide for Businesses & Individuals

-

Understanding Net Investment Income (NII): Definition & Calculation

Understanding Net Investment Income (NII): Definition & CalculationNet investment income (NII) is the total income before taxes that an investor receives on their portfolio of investment assets. NII is generated from dividends, capital gainsCapital GainA capital gain...

-

Understanding Earnings Before Tax (EBT): Definition & Importance

Understanding Earnings Before Tax (EBT): Definition & ImportanceEarnings before tax, or pre-tax income, is the last subtotal found in the income statement Income StatementThe Income Statement is one of a companys core financial statements that shows their profit a...