Understanding Net Income: A Comprehensive Guide

Net income is the amount of accounting profit a company has left over after paying off all its expenses. Net income is found by taking sales revenueSales RevenueSales revenue is the income received by a company from its sales of goods or the provision of services. In accounting, the terms "sales" and and subtracting COGS, SG&ASG&ASG&A includes all non-production expenses incurred by a company in any given period. It includes expenses such as rent, advertising, marketing, depreciation, and amortization, interest expenseInterest ExpenseInterest expense arises out of a company that finances through debt or capital leases. Interest is found in the income statement, but can also, taxes and any other expenses.

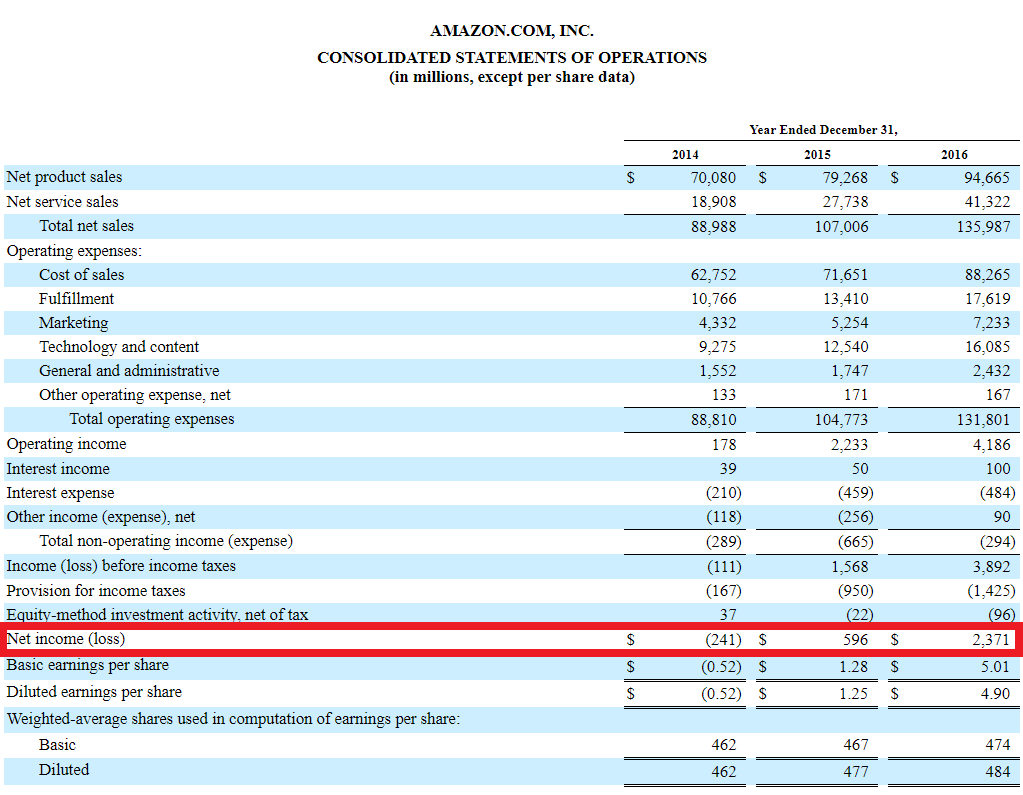

Net income is the last line item on the income statementIncome StatementThe Income Statement is one of a company's core financial statements that shows their profit and loss over a period of time. The profit or proper. Some income statements, however, will have a separate section at the bottom reconciling beginning retained earnings with ending retained earnings, through net income and dividends.

Other Names for Net Income

The bottom line of a company’s income statement has three commonly used names, which include:

- Net Income

- Net Profit

- Net Earnings

All three of these terms mean the same thing, which can sometimes be confusing for people who are new to finance and accounting.

In this article, we use all three terms interchangeably.

Download the Free Template

Enter your name and email in the form below and download the free template now!

Ties to Other Financial Statements

The net income is very important in that it is a central line item to all three financial statementsThree Financial StatementsThe three financial statements are the income statement, the balance sheet, and the statement of cash flows. These three core statements are. While it is arrived at through the income statement, the net profit is also used in both the balance sheet and the cash flow statement.

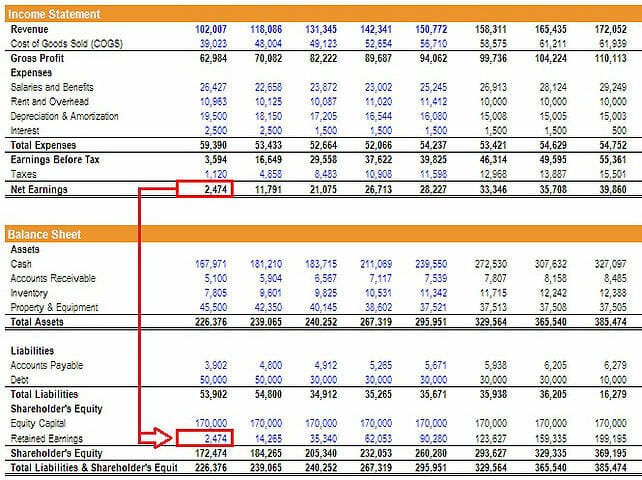

Net income flows into the balance sheet through retained earnings, an equity account. This is the formula for finding ending retained earnings:

Ending RE = Beginning RE + Net Income – Dividends

Assuming there are no dividends, the change in retained earnings between periods should equal the net earnings in those periods. If there is no mention of dividends in the financial statements, but the change in retained earnings does not equal net profit, then it’s safe to assume that the difference was paid out in dividends.

In the cash flow statement, net earnings are used to calculate operating cash flows using the indirect method. Here, the cash flow statement starts with net earnings and adds back any non-cash expenses that were deducted in the income statement. From there, the change in net working capitalNet Working CapitalNet Working Capital (NWC) is the difference between a company's current assets (net of cash) and current liabilities (net of debt) on its balance sheet. is added to find cash flow from operations.

Profitability and Return on Equity

Net earnings are also used to determine the net profit margin. This is a handy measure of how profitable the company is on a percentage basis, when compared to its past self or to other companies.

Net profit margin is also used in the DuPont method for decomposing return on equity – ROEReturn on Equity (ROE)Return on Equity (ROE) is a measure of a company’s profitability that takes a company’s annual return (net income) divided by the value of its total shareholders' equity (i.e. 12%). ROE combines the income statement and the balance sheet as the net income or profit is compared to the shareholders’ equity.. The basic DuPont formula splits ROE out into three components:

ROE = Net Profit Margin x Total Asset Turnover x Financial Leverage

Analyzing a company’s ROE through this method allows the analyst to determine the company’s operational strategy. A company with high ROE due to high net profit margins, for example, can be said to operate a product differentiation strategy.

Net Income vs. Cash Flow

Net income is an accounting metric and does not represent the economic profit or cash flowValuationFree valuation guides to learn the most important concepts at your own pace. These articles will teach you business valuation best practices and how to value a company using comparable company analysis, discounted cash flow (DCF) modeling, and precedent transactions, as used in investment banking, equity research, of a business.

Since net profit includes a variety of non-cash expenses such as depreciation, amortization, stock-based compensation, etc., it is not equal to the amount of cash flow a company produced during the period.

For this reason, financial analysts go to great lengths to undo all of the accounting principles and arrive at cash flow for valuing a company.

To learn more, explore CFI’s financial modeling courses.

Additional Resources

CFI’s mission is to help anyone become a world-class financial analystThe Analyst Trifecta® GuideThe ultimate guide on how to be a world-class financial analyst. Do you want to be a world-class financial analyst? Are you looking to follow industry-leading best practices and stand out from the crowd? Our process, called The Analyst Trifecta® consists of analytics, presentation & soft skills. The CFI resources below are designed to give you the tools and training you need to become a great financial analyst:

- How the 3 Statements are Linked (free webinar)CFI Webinar - Link the 3 Financial StatementsThis CFI quarterly webinar provides a live demonstration of how to link the 3 financial statements in Excel. Learn the formulas and proper linking procedure

- Depreciation ExpenseDepreciation ExpenseWhen a long-term asset is purchased, it should be capitalized instead of being expensed in the accounting period it is purchased in.

- Valuation MethodsValuation MethodsWhen valuing a company as a going concern there are three main valuation methods used: DCF analysis, comparable companies, and precedent transactions

- Financial Modeling GuideFree Financial Modeling GuideThis financial modeling guide covers Excel tips and best practices on assumptions, drivers, forecasting, linking the three statements, DCF analysis, more

-

EBITDA Explained: Understanding Earnings Before Interest, Taxes, Depreciation & Amortization

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization and is a metric used to evaluate a company’s operating performance. It can be seen as a proxy for cash flowCash

-

Understanding Income: Definition, Types & Uses

Income refers to the money that is earned by an individual for providing a service or as an exchange for providing a product. The income earned by an individual is used to fund their day-to-day expend

Accounting

- Net Income Attributable to Shareholders: Definition & Significance

- Profitability Ratios: Understanding Your Company's Profitability

- Net Interest Income (NII): Definition & Calculation

- Understanding Net of Tax: Definition & Calculation

- Understanding Net Investment Income (NII): Definition & Calculation

- Understanding Accounting Income: A Key Financial Metric

- Accrued Income Explained: Definition & Accounting

- Gross vs. Net: Understanding the Difference - Definitions & Examples

- Net Income Explained: A Comprehensive Guide for Businesses & Individuals

-

Understanding Discretionary Income: Definition & Examples

Understanding Discretionary Income: Definition & ExamplesDiscretionary income is the amount of income that is left for an individual, household, or business after paying the necessary or essential expenses. Necessary expenses are expenses that ar...

-

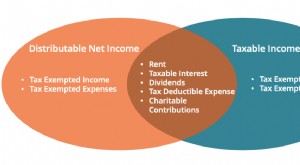

Understanding Distributable Net Income (DNI): A Comprehensive Guide

Understanding Distributable Net Income (DNI): A Comprehensive GuideDistributable Net Income (DNI) is a term that describes the portion of a trust’s income allotted to the beneficiaries. The calculation of DNI is performed to distribute the income of the trust b...