Understanding Adjusted Funds From Operations (AFFO) for REITs

Adjusted Funds From Operations (AFFO) is a measure of the financial performance of a REIT, and it is used as an alternative to Funds From Operations (FFO)FFO - Funds From OperationsFFO or Funds From Operations is a measure of cash flow generated from business operations that is often used by Real Estate Investment Trusts - REITS. Funds from operations (FFO) is the actual amount of cash flow generated from core business operations. Guide to FFO. AFFO is a superior measure compared to FFO because the former considers the maintenance costs of the real estate property over its life. The value of AFFO is obtained by making adjustments to the FFO figure to deduct recurring expenditures required to keep the real estate property running and generating revenues.

Another adjustment made to the FFO figure is the straight-lining of rents, which distributes rent expenses over the life of the property. Investors use AFFO as a better indicator of the REIT’s ability to pay dividends from its net earnings.

Summary

- Adjusted Funds From Operations (AFFO) is a measure of the financial performance of a REIT, and it is used as an alternative to Funds From Operations (FFO).

- It is calculated by making adjustments to the FFO value to deduct normalized recurring expenditures and to use straight-lining of rents.

- AFFO is used by investors and analysts to determine a company’s ability to pay dividends to stockholders in the future.

How to Calculate Adjusted Funds From Operations

When calculating the AFFO, the first step is to calculate the funds from operations, which measure the cash flows from a REIT’s leasing activities. The FFO was originally introduced by the National Association of Real Estate Investment Trusts (NAREIT) as a measure of cash flows generated by REITs.

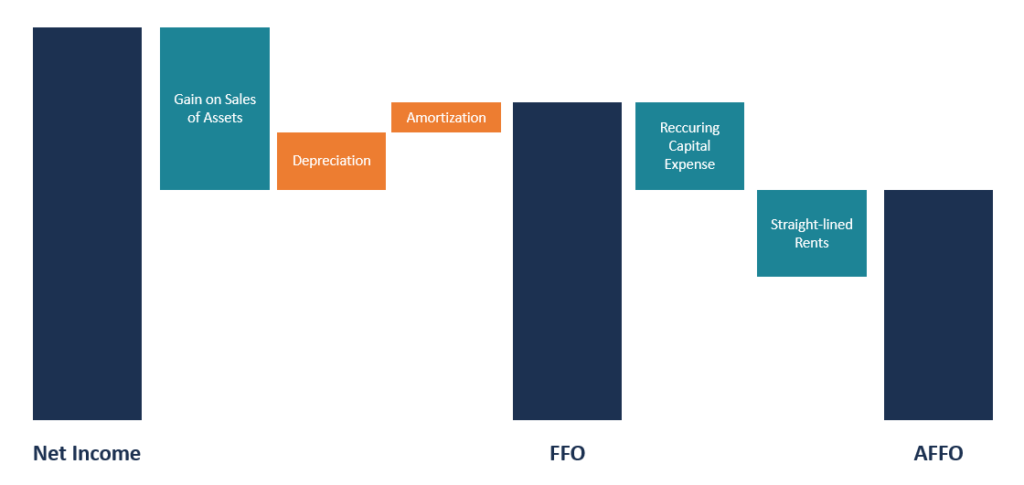

FFO is obtained by deducting any gains on the sale of properties from the net income and adding back the depreciation and amortization costs. The value of the gains on the sale of properties is excluded from the FFO computation because the transactions are one-time events that do not affect the REIT’s future earning’s potential. The FFO’s formula is indicated below:

FFO = Net Income – Gains on Sales of Underlying Assets + Depreciation + Amortization

Once the value of FFO is obtained, any capitalized and amortized recurring expenditures are then deducted. The expenditures include costs that are incurred to maintain the properties owned by the REITReal Estate Investment Trust (REIT)A real estate investment trust (REIT) is an investment fund or security that invests in income-generating real estate properties. The fund is operated and owned by a company of shareholders who contribute money to invest in commercial properties, such as office and apartment buildings, warehouses, hospitals, shopping centers, student housing, hotels. Some of these costs include painting projects, roof replacements, recarpeting, tenant improvements, etc. Another adjustment made to the FFO is the straight-lining of rent, which distributes the rent and lease expenses evenly across the life of the lease.

The formula for AFFO is given below:

AFFO = FFO – Recurring Capital Expenditures – Straight-lined Rents

Practical Example of AFFO

During the last reporting period, ABC Limited reported a net income of $2.5 million. It also incurred $100,000 and $150,000 in the form of depreciation and amortizationAmortizationAmortization refers to the process of paying off a debt through scheduled, pre-determined installments that include principal and interest costs, respectively, during the period. The company also made a profit of $500,000 from the sale of two properties in its portfolio. It also incurred an $80,000 loss on the sale of another property during the same period.

In the same period, ABC Limited also reported straight-lined rents of $130,000 and recurring capital expenditures of $200,000, which were incurred when making roof repairs, HVAC replacements, carpeting, and other structural improvements to the properties it owns.

Using the information above, we can calculate the AFFO as follows:

Step 1: Calculate the value of the FFO.

FFO = $2,500,000 + $100,000 + $150,000 – ($500,000 – $80,000)

FFO = $2,750,000 – $420,000

FFO = $2,330,000

Step 2: Deduct recurring capital expenditures and straight-lined rents from the value of FFO.

AFFO= FFO – Capital Expenditures – Straight-line Rent Adjustments

AFFO = $2,330,000 – $200,000 – $130,000

AFFO = $2,000,000

FFO vs. AFFO

According to NAREIT, FFO is the most commonly accepted measure of a REIT’s operating performance. It equals the value of net income plus the depreciation and amortization of the property and excludes the gains or losses on the sale of properties owned by the REIT. NAREIT provides guidelines on how REITs should calculate their FFO. However, it only serves as a supplementary figure, and companies can use different FFO formulas to report information. Also, FFO comes with weaknesses, and the AFFO attempts to address some of the shortcomings.

AFFO was introduced to solve some of the weaknesses of FFO, and it is considered a better measure of residual cash flow for shareholders. It deducts the cost of running the portfolio of properties from the FFO. The costs deducted are the costs that the company must pay to keep the business running, and such costs cannot be paid out to shareholders as dividends. The costs include the normalized recurring expenditures that are capitalized and amortized, as well as the straight-lining of rents.

The value of the AFFO provides investors with a clearer picture of the REIT’s dividend-paying ability. Also, unlike FFO, NAREIT lacks a specific definition of AFFO, and it means that REITs enjoy greater flexibility on what adjustments to make to the FFO to get the final AFFO value.

Additional Resources

CFI offers the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

- All Risks Yield (ARY)All Risks Yield (ARY)All Risks Yield (ARY) is a conventional real estate metric that uses annual rental revenue to determine the capital value of an investment.

- Free Cash Flow FormulaFree Cash Flow (FCF) FormulaThe FCF Formula = Cash from Operations - Capital Expenditures. FCF represents the amount of cash flow generated by a business after deducting CapEx

- Operating IncomeOperating IncomeOperating income is the amount of revenue left after deducting the operational direct and indirect costs from sales revenue.

- Rent ExpenseRent ExpenseRent expense refers to the total cost of using rental property for each reporting period. It is typically among the largest expenses that

-

Crypto Hedge Funds: Navigating the Emerging Market

Traditional hedge funds have been active in the financial markets for several years, allowing investors to practically invest in every asset class such as fixed income, equity, currency, and commodi

-

Quantitative Funds (Quant Funds): An In-Depth Explanation

In the wealth and asset management company, investments are managed by fund managers. They are aided by teams of research analysts in analyzing diverse and voluminous information. Investment strategie

finance

- Mutual Funds: A Beginner's Guide to Diversified Investing

- P/AFFO Explained: Understanding REIT Financial Health

- P/FFO vs. P/AFFO: Understanding REIT Valuation Metrics

- Mutual Funds Explained: A Beginner's Guide to Investing

- Vulture Funds Explained: Investing in Distressed Debt

- Discontinued Operations: Definition & Accounting Treatment

- FFO Explained: Understanding Funds From Operations for Real Estate Investors

- Slush Funds: Definition, Purpose, and Illicit Uses

- Segregated Funds: Understanding Insurance-Backed Investments

-

Business Operations: Definition, Activities & Optimization

Business Operations: Definition, Activities & OptimizationBusiness operations refer to activities that businesses engage in on a daily basis to increase the value of the enterprise and earn a profit. The activities can be optimized to generate sufficient rev...

-

Municipal Bonds: Tax-Advantaged Investing Explained

Municipal Bonds: Tax-Advantaged Investing ExplainedMunicipal bonds represent an attractive investment for individuals, especially for people in high income brackets, looking for assets that provide tax-advantaged income.What makes these types of bond...