Basel I: Understanding Core Banking Regulations & Capital Requirements

Basel I refers to a set of international banking regulations created by the Basel Committee on Bank Supervision (BCBS), which is based in Basel, Switzerland. The committee defines the minimum capital requirements for financial institutions, with the primary goal of minimizing credit riskCredit RiskCredit risk is the risk of loss that may occur from the failure of any party to abide by the terms and conditions of any financial contract, principally,. Basel I is the first set of regulations defined by the BCBS and is a part of what is known as the Basel Accords, which now includes Basel IIBasel IIBasel II is the second set of international banking regulations defined by the Basel Committee on Bank Supervision (BCBS). It is an extension of the regulations for minimum capital requirements as defined under Basel I. The Basel II framework operates under three pillars: Capital adequacy requirements, Supervisory review, and Market discipline. and Basel III. The accords’ essential purpose is to standardize banking practices all over the world.

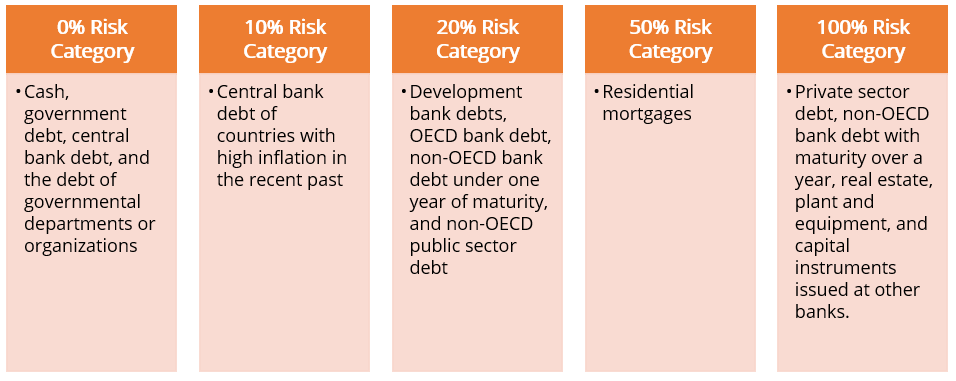

Bank Asset Classification System

The Bank Asset Classification System classifies a bank’s assets into five risk categories on the basis of a risk percentage: 0%, 10%, 20%, 50%, and 100%. The assets are classified into different categories based on the nature of the debtor, as shown below:

Implementation

Basel I primarily focuses on credit risk and risk-weighted assets (RWA)Risk-Weighted AssetsRisk-weighted assets is a banking term that refers to an asset classification system that is used to determine the minimum capital that banks should keep as a reserve to reduce the risk of insolvency. Maintaining a minimum amount of capital helps to mitigate the risks.. It classifies an asset according to the level of risk associated with it. Classifications range from risk-free assets at 0% to risk assessed assets at 100%. The framework requires the minimum capital ratio of capital to RWA for all banks to be at 8%.

Tier 1 capital refers to capital of more permanent nature. It should make up at least 50% of the bank’s total capital base. Tier 2 capital is temporary or fluctuating in nature.

Benefits of Basel I

- Significant increase in Capital Adequacy RatiosCapital Adequacy Ratio (CAR)The Capital Adequacy Ratio (CAR) sets the standards for banks by looking at a bank's ability to pay liabilities and respond to credit risks and operational risks. of internationally active banks

- Competitive equality among internationally active banks

- Augmented management of capital

- A benchmark for financial evaluation for users of financial information

Limitations

- Other kinds of risk, such as market risk, operational risk, liquidity risk, etc. were not taken into consideration.

- Emphasis is put on the book values of assets rather than the market values.

Related Readings

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

- Basel IIIBasel IIIThe Basel III accord is a set of financial reforms that was developed by the Basel Committee on Banking Supervision (BCBS), with the aim of strengthening

- Major Risks for BanksMajor Risks for BanksMajor risks for banks include credit, operational, market, and liquidity risk. Since banks are exposed to a variety of risks, they have well-constructed risk management infrastructures and are required to follow government regulations.

- MIFID IIMiFID IIMiFID II is the revision of the Markets in Financial Instruments Directive (MiFID), originally published in 2004. It is the foundation of financial legislation for the European Union, designed to keep financial markets strong, fair, effective, and transparent.

- Reserve RatioReserve RatioThe reserve ratio – also known as bank reserve ratio, bank reserve requirement, or cash reserve ratio – is the percentage of deposits a financial institution must hold in reserve as cash. The central bank is the institution that determines the required amount of reserve ratio.

-

Return on Total Capital (ROTC): Definition & Calculation

Return on Total Capital (ROTC) is a return on investment ratio that quantifies how much return a company has generated through the use of its capital structureCapital StructureCapital structure refers

-

ROIC: Understanding Return on Invested Capital - Definition & Calculation

ROIC stands for Return on Invested Capital and is a profitability or performance ratio that aims to measure the percentage return that a company earns on invested capitalStockholders EquityStockholder

finance

- Capital Appropriation: Definition, Process & Examples

- Basel II: Understanding International Banking Regulations

- Understanding Capital: Types, Categories & Value Creation

- Capital Rationing: Definition, Strategy & Impact on Investment Decisions

- Cost of Capital: Definition, Calculation & Importance

- Venture Capital: Funding Startups & Understanding Equity

- Understanding Capital Losses: Definition, Calculation & Examples

- Understanding Mispricing: Market Prices vs. True Value

- Understanding Intellectual Capital: Definition & Value

-

Invested Capital: Definition & How It Fuels Business Growth

Invested Capital: Definition & How It Fuels Business GrowthInvested capital is the investment made by both shareholdersShareholderA shareholder can be a person, company, or organization that holds stock(s) in a given company. A shareholder must own a minimum ...

-

Return on Invested Capital (ROIC): Definition & Calculation

Return on Invested Capital (ROIC): Definition & CalculationReturn on Invested CapitalInvested CapitalInvested capital is the investment made by both shareholders and debtholders in a company. When a company needs capital to expand, it can obtain it either by ...