Budgetary Slack: Definition, Benefits & Risks

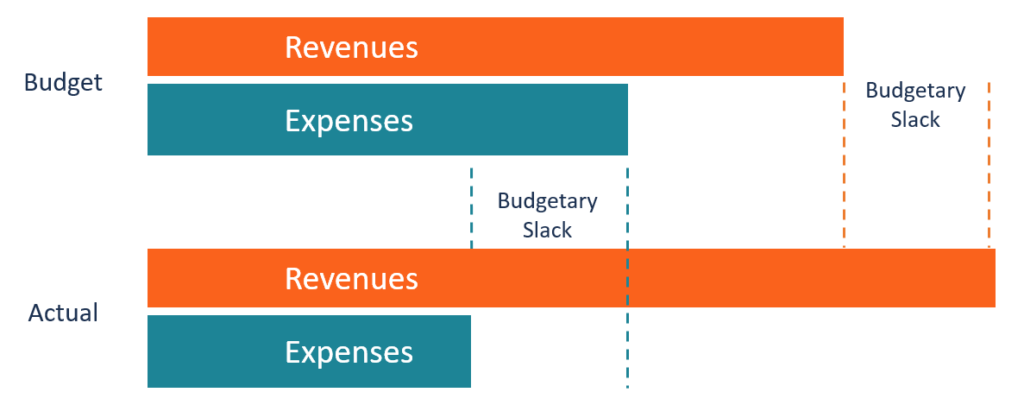

Budgetary slack is the practice of overestimating the expenses and/or underestimating the projected revenuesRevenueRevenue is the value of all sales of goods and services recognized by a company in a period. Revenue (also referred to as Sales or Income) when preparing a budget statement for the next financial period. It is a cushion created by management or lower-level managers to prepare budget estimates that will not be hard to achieve.

In other instances, budgetary slack may be a result of the management adding unverified numbers, especially in highly competitive industries where changes are common. A true budget statement must be honest; it should reflect actual anticipated revenues and expenses.

Causes of Budgetary Slack

The following are some of the common causes of a budgetary slack when preparing an annual budget for the company:

1. Uncertainty on results expected

The managers of a company may face a lot of uncertainty over the results expected in a future period. For example, when the company is introducing a new product line, the managers lack actual data on the kind of results to expect. As a result, they will be conservative when setting up the budget for the coming financial yearFiscal Year (FY)A fiscal year (FY) is a 12-month or 52-week period of time used by governments and businesses for accounting purposes to formulate annual to avoid promising beyond what they can achieve. Budgetary slack may occur when the managers underestimate the expected revenues to remain in a range that is easy to achieve for a new product line.

2. Information asymmetry

Information asymmetry occurs when one party possesses more information about the subject than the other. In such a case, departmental-level managers may be able to access private information about resource requirements, employee productivity, and expenditures which the senior management may not be privy to.

The lower-level managers may take advantage of the information asymmetryAsymmetric InformationAsymmetric information is, just as the term suggests, unequal, disproportionate, or lopsided information. It is typically used in reference to some type of business deal or financial arrangement where one party possesses more, or more detailed, information than the other. to advance their self-interest without the knowledge of the top management. They can set easy-to-achieve revenue targets so that they can be seen to be working hard by the management, even when they are guaranteed to outperform the previous year’s results.

3. Rewards dependent on budget attainment

In organizations where employee awards and payoffs are dependent on budget attainment, lower-level managers may create budget slacks to make the target easy to achieve. The subordinate managers are often under pressure from top management to make sure that the set goals are achieved, which means that they can influence the process to work in their favor.

As the managers perform supervisory roles, they know what is achievable and what resources are required. They would, therefore, present a high budget for expenses while low-balling the expected revenues target at a level that is easily attainable. This would make it easy for them to beat the set targets in every period and enjoy the promised rewards, salary hikes, and job promotions.

How to Prevent Budgetary Slack

The occurrence of budgetary slacks within an organization can result in declining productivity and performance because the employees work towards attaining goals that are within their capability. Implementing the measures below can help reduce budget slacks in an organization:

1. Limiting the number of managers who contribute to the budget

When too many managers are allowed to contribute to the budget model, they may allow too much slack as a way of downplaying their company’s expectations. This will allow too much wastage since the employees lack the motivation to be productive when the targets are easily achievable.

Limiting the number of managers who prepare the budgets to a few aggressive managers can help reduce the slack. The managers will put the expectations high to create a challenge for the employees to move out of their comfort zone and work towards attaining those goals. If the employees are unable to achieve that target, they will be motivated to attempt the challenge again in the next financial period.

2. A budget should not be the basis for evaluating performance

Most organizations use the budget as a tool to measure how well the employees performed in a given period. Employees who are found to have achieved their targets are rewarded with bonuses and payoffs, whereas those who are unable to achieve the targets are reprimanded.

However, this encourages employees to create a budgetary slack that allows them easily achievable targets so that they can be rewarded in every financial period. Removing any link between performance, bonuses, and the budget can reduce the motivation to cheat the system and benefit from a performance-based reward.

Disadvantages of Budgetary Slack

A budgeting slack comes with the following disadvantages:

1. Underestimating profits portrays the business as struggling

When the subordinate managers continually create easy targets, the business will be seen as underperforming in a highly competitive market. Even when the business is on track to hit new highs, the managers will use up the additional revenues left in the budget because of the budgetary slack made to the budget.

Such a practice will portray the business as struggling and may force high-performing employees to jump ship to stronger competitors. Artificially slowing down the growth may also adversely affect the company’s performance. Shareholders will start casting doubt on the company’s ability to continue generating revenues.

2. Understating revenues will affect other activities of the business

When the budget estimates for the next financial year show that the revenues are lower than what the top management projected, the company will cut the expense budget for important functions such as marketing and advertising, research and developmentResearch and Development (R&D)Research and Development (R&D) is a process by which a company obtains new knowledge and uses it to improve existing products and introduce, production, and administrative expensesSG&ASG&A includes all non-production expenses incurred by a company in any given period. It includes expenses such as rent, advertising, marketing. Slashing the expense budgets will affect the long-term viability of the business.

For example, reducing the expense budget for the marketing department will limit the company’s potential to get new customers and even retain existing customers, which is critical to the ongoing profitability of the business.

Additional Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Budget VarianceBudget VarianceBudget variance deals with a company’s accounting discrepancies. The term is most often used in conjunction with a negative scenario. An example is when a company fails to accurately budget for their expenses – either for a given project or for total quarterly or annual expenses.

- Capital Budgeting Best PracticesCapital Budgeting Best PracticesCapital budgeting refers to the decision-making process that companies follow with regard to which capital-intensive projects they should pursue. Such capital-intensive projects could be anything from opening a new factory to a significant workforce expansion, entering a new market, or the research and development of new products.

- Project BudgetProject BudgetThe Project Budget is a tool used by project managers to estimate the total cost of a project. A project budget template includes a detailed estimate of all costs that are likely to be incurred before the project is completed.

- Revenue Variance AnalysisRevenue Variance AnalysisRevenue Variance Analysis is used to measure differences between actual sales and expected sales, based on sales volume metrics, sales mix

-

Zero-Based Budgeting: A Comprehensive Guide for Businesses

Zero-based budgeting is a type of budgeting that is used by many different companies in the world today. Here are the basics of zero-based budgeting and how it can help you as a company. Zero-Bas

-

Incremental Budgeting: Pros, Cons & Why It's Often Problematic

Incremental budgeting is a type of budgeting that adds a certain amount of capital to a previous periods budget in order to allow for slight increases. This type of budget is simple, but it also

finance

- Advertising Budget: Definition, Planning & Best Practices

- Understanding Balanced Budgets: Definition & Importance

- Budgeting Explained: A Comprehensive Guide for Individuals & Businesses

- Understanding Budget Deficits: Causes, Effects & Solutions

- Budget Variance Explained: Causes, Types & Analysis

- Business Budgeting: A Comprehensive Guide to Planning & KPIs

- Negotiated Budgeting: A Collaborative Approach to Financial Planning

- Participative Budgeting: Definition, Benefits & Implementation

- Project Budget: Definition, Template & Cost Estimation

-

Rollover Budget: How It Works & Benefits for Financial Planning

Rollover Budget: How It Works & Benefits for Financial PlanningYoung couple going over budget at table A rollover budget is when the budget category totals rollover into the next month. This means you could start the month in the negative if you have ove...

-

Understanding Money Managers: Services & Benefits

Understanding Money Managers: Services & BenefitsA money manager is a person or entity that manages the financial assetsFinancial AssetsFinancial assets refer to assets that arise from contractual agreements on future cash flows or from owning equit...