Participative Budgeting: Definition, Benefits & Implementation

Participative budgeting is a budgeting process in which the people who are in the lower levels of management are involved in the budget preparation process. Unlike the imposed budgetingImposed BudgetingImposed budgeting, also known as top-down budgeting, is the process wherein the top management of a company prepares a budget and then imposes it on lower-level managers for implementation. It starts at the top, where the budget is prepared by senior management process, participative budgeting shares the responsibility with lower-level managers to give them a sense of ownership in the business.

Participative budgeting also tends to produce budgets that are more achievable since lower-level employees are better positioned to inform their supervisors where funds need to be allocated. When an organization implements participative budgeting, it shows the top management’s confidence in its staff. The employees’ sense of ownership gives them the motivation to work hard and attain the goals that they helped prepare.

How It Works

A budget faces a higher chance of being achievable if the people preparing the budget are knowledgeable about the costs that are incurred within the organization. While the top management may possess the necessary information about the running of the company, they may not be privy to the costs incurred at the departmental level. It means that they may underestimate the costs or overestimate the projected revenuesEarnings GuidanceAn earnings guidance is the information provided by the management of a publicly traded company regarding its expected future results, including estimates. It will eventually affect the running of the department due to cash shortfalls. However, involving the subordinate managers to coordinate the budget preparation process will benefit the company since these managers have better information about the running of their respective departments.

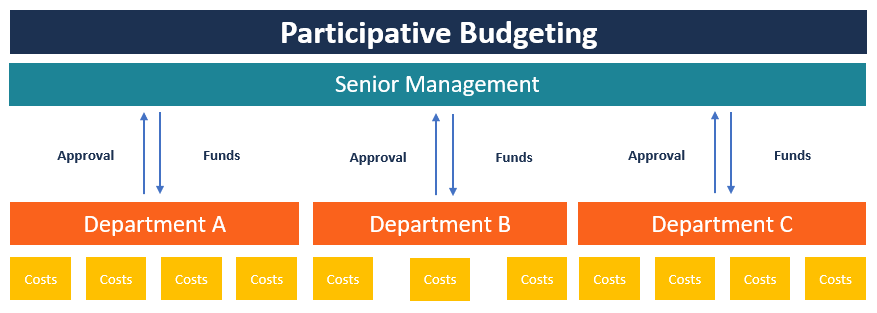

A participative budgeting process will be more effective when the organization adopts a system of checks and balances to prevent unruly managers from abusing their power. Since the budget moves from the lower managers to the middle and then to the top management, the budget draft can be reviewed at each level of management, with the top managers having the final say.

At each managerial level of review, the managers are interested in identifying any costs that may result in wastage and inefficiencies in the company. Before any changes are made to the budget draft, the lower-level managers must be involved to give their reasons for making certain suggestions in the budget. This will result in the effective use of funds when the managers work hand-in-hand with the accounting staff.

Advantages of Participative Budgeting

The following are some of the benefits of implementing a participative budgeting approach in an organization:

1. Transfer of information upwards

One of the advantages of participative budgeting is the sharing of information from departmental-level managers to top management. It means that subordinate managers are given the opportunity to present their views on certain organizational issues.

The managers also get a chance to discuss the difficulties that they encounter in budget preparation and brainstorm ways of solving the problems. Both the top managers and the subordinates are also able to share their points of view on certain issues of interest.

2. Employee motivation

When employees are involved in the budget preparation process, they get to own a part of the budgeting process. It gives them a sense of ownership when their suggestions are taken into account by senior management. They also feel appreciated by management when they are given an opportunity to sit down with the top managers and share their views on certain points of interest. Employee involvement in the process improves their moraleEmployee MoraleEmployee morale is defined as the overall satisfaction, outlook, and feelings of well-being that an employee holds in the workplace. In other, providing them with a greater urge to work harder towards the attainment of the goals that they helped set.

3. Goal congruence

Goal congruence refers to the agreement between the employee’s goals and the overall company goals. In order for the company to create a budget that is achievable, both the management and the staff must set goals that move in the same direction.

For example, if the goal of the company is to double the production capacity in the next year, it should be shared with the employees since they are the people tasked with implementing the proposal. If there is no agreement between the company’s goals and the subordinate managers’ goals, it will be impossible to attain the set targets.

Disadvantages of Participative Budgeting

1. Time-consuming

The most common limitation of a participative budget is that it is time-consuming compared to an imposed budget. Since the budget preparation starts from the department level to the top, too much participation may occur that may derail the process. Involving all employees in each department will mean that the negotiations may take too long before the staff reaches an agreement. If there is no agreement, the management will need to make the final decision, which means that the staff will need to accept an imposed decision.

2. Budgetary slack

The other limitation is budgetary slackBudgetary SlackBudgetary slack is the practice of overestimating the expenses and/or underestimating the projected revenues when preparing a budget statement for the next financial period. It is a cushion created by management or lower-level managers to prepare budget estimates that will not be hard to achieve.. The employees may overestimate the costs and/or underestimate the revenue projections as a way of manipulating the budget to their advantage. It means that the subordinate managers will set targets that they are sure to achieve and even exceed in the next financial year. This mostly happens when the manager’s performance is measured on the basis of the attainment of the budget. By making the budget easy to achieve, the managers will be seen as exceeding their targets.

Additional Resources

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant CFI resources below:

- Bottom-Up BudgetingBottom-up BudgetingBottom-up budgeting is a budgeting method that starts at the department level, moving up to the top level. Each department within the organization is required to compile a list of the things it needs, the projects it plans to carry out in the next financial period, and cost estimates. The estimates of all the departments are then summed up to get the overall company budget.

- Fixed and Variable CostsFixed and Variable CostsCost is something that can be classified in several ways depending on its nature. One of the most popular methods is classification according

- Top-Down BudgetingTop-Down BudgetingTop-down budgeting refers to a budgeting method where senior management prepares a high-level budget for the company. The company’s senior management prepares the budget based on its objectives and then passes it on to department managers for implementation.

- Types of BudgetsTypes of BudgetsThere are four common types of budgeting methods that companies use: (1) incremental, (2) activity-based, (3) value proposition, and (4)

-

Advertising Budget: Definition, Planning & Best Practices

An advertising budget is a company’s allocation of promotional expenditures over a specified time period. It is a measure of a company’s planned expenditure on accomplishing marketing obje

-

Understanding Budget Deficits: Causes, Effects & Solutions

A budget deficit occurs when government expenditures exceed revenues from taxes and other sources. Although the concept of a budget deficit applies to any organization with operating revenues and expe

finance

- Bottom-Up Budgeting: A Comprehensive Guide

- Budgetary Slack: Definition, Benefits & Risks

- Business Budgeting: A Comprehensive Guide to Planning & KPIs

- Imposed Budgeting: Definition, Pros & Cons | [Your Company Name]

- Negotiated Budgeting: A Collaborative Approach to Financial Planning

- Output/Input Budgeting: A Comprehensive Guide

- Top-Down Budgeting: Definition, Advantages & Disadvantages

- Zero-Based Budgeting: A Comprehensive Guide for Businesses

- Incremental Budgeting: Pros, Cons & Why It's Often Problematic

-

Activity-Based Budgeting (ABB): A Comprehensive Guide

Activity-Based Budgeting (ABB): A Comprehensive GuideActivity-based budgeting (ABB) is a budgeting method where activities are thoroughly analyzed to predict costs. ABB does not take historical costs into account when creating a budget. Summa...

-

Budgeting 101: Understanding & Creating a Personal Budget

Budgeting 101: Understanding & Creating a Personal BudgetEveryone says you should have a budget, and that’s certainly good advice. But if you’ve never had a budget, you may not be entirely sure what it is and what it’s designed to accomplish. In this articl...