Net Liquid Assets: Definition, Calculation & Importance

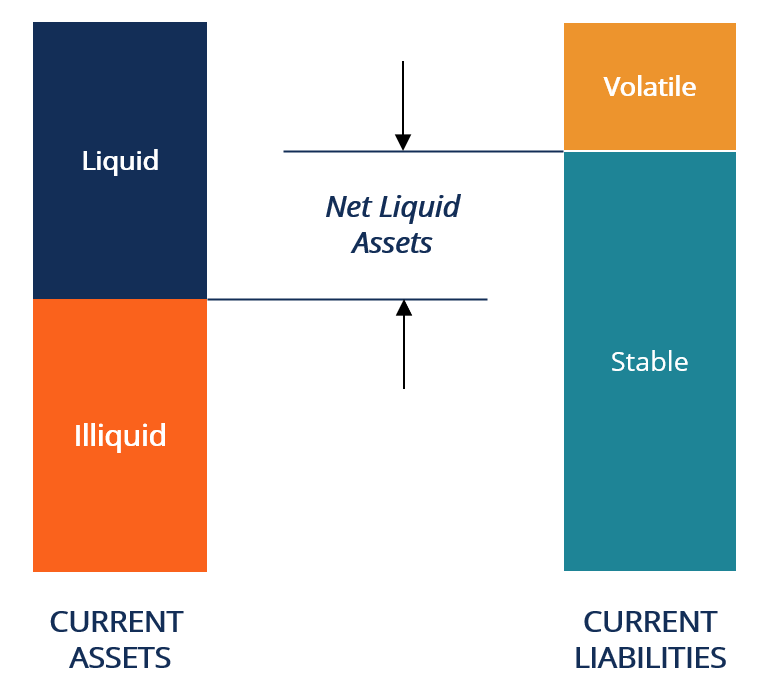

Net liquid assets is a term used to define the immediate liquidity position of a company. It is calculated as the difference between liquid assets and current liabilitiesCurrent LiabilitiesCurrent liabilities are financial obligations of a business entity that are due and payable within a year. A company shows these on the. Examples of liquid assets include cash, money market assets, stocks, accounts receivable, marketable securities, or any assets that can be quickly converted into cash.

Net liquid assets can be used to assess the financial condition of a company. If a company owns positive net liquid assets, it means it is in a comfortable position to make any payments in the near-term or if it can undertake any investment activity without any financing support.

Certain assets do not fall in the definition of liquid assets, even though they are current assets. An example is inventoryInventoryInventory is a current asset account found on the balance sheet, consisting of all raw materials, work-in-progress, and finished goods that a. Although it can be sold to generate cash, it is very probable that the inventory sold immediately would be sold at a discount.

Other current assets, such as prepaid expenses and income tax receivables, cannot be sold for cash, which is why they are not considered liquid assets.

When looking at current liabilities, we can categorize them as volatile or stable. In most calculations of net liquid assets, volatile liabilities are excluded. Volatile liabilities include funds that are unstable and can disappear from a company’s balance sheet overnight. An example of a volatile liability on a bank’s balance sheet is uninsured borrowings.

Summary

- Net liquid assets is a term used to define the immediate liquidity position of a company, and it is calculated as the difference between liquid assets and current liabilities.

- Asset liquidity is very crucial for all types of businesses, and it helps indicate how comfortable a company is if it faces an emergency or unusual situation.

- Certain assets do not fall in the definition of liquid assets, even though they are current assets.

Importance of Liquid Assets

Asset liquidity is very crucial for all types of businesses, and it helps indicate how comfortable a company is if it faces an emergency or unusual situation. Consider a situation where there is an economic crisis, and a company is heavily indebted without any liquid assets. The immediate effect (if the company is not able to raise additional funds) would be that it would declare bankruptcyBankruptcyBankruptcy is the legal status of a human or a non-human entity (a firm or a government agency) that is unable to repay its outstanding debts.

It is also true that the more liquid assets a company owns, the better chances are that it gets a loan and at favorable rates. Most financial institutions ask companies to post assets as collateral, and owning liquid assets shows that in the case of solvency, the bank loan can be repaid.

Liquid assets are also an indicator of whether a company is putting its assets to good use. If a company has excessive idle cash lying around in its bank account, it can be said that it is not making good use of its liquid assets. The cash can be used for investments or paying dividends to shareholders.

However, the biggest dilemma is to maintain the ideal balance between having adequate financial security (in terms of liquid assets) and not having too much idle cash. Most companies and experts suggest having a buffer of at least six months of expenses in liquid assets, which covers operating costsOperating ExpensesOperating expenses, operating expenditures, or "opex," refers to the expenses incurred regarding a business’s operational activities. and also accounts for any emergency funds that may be required during the period.

Example of Net Liquid Assets Calculation

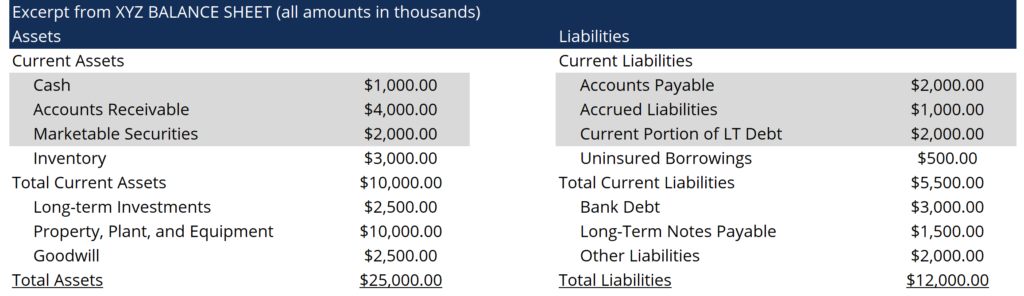

The following is a numerical example of the calculation of net liquid assets. Figure 2 is an excerpt from the balance sheet of Company XYZ, which shows the various types of assets and liabilities of the company. The components of the balance sheet that are used to calculate net liquid assets are highlighted in grey.

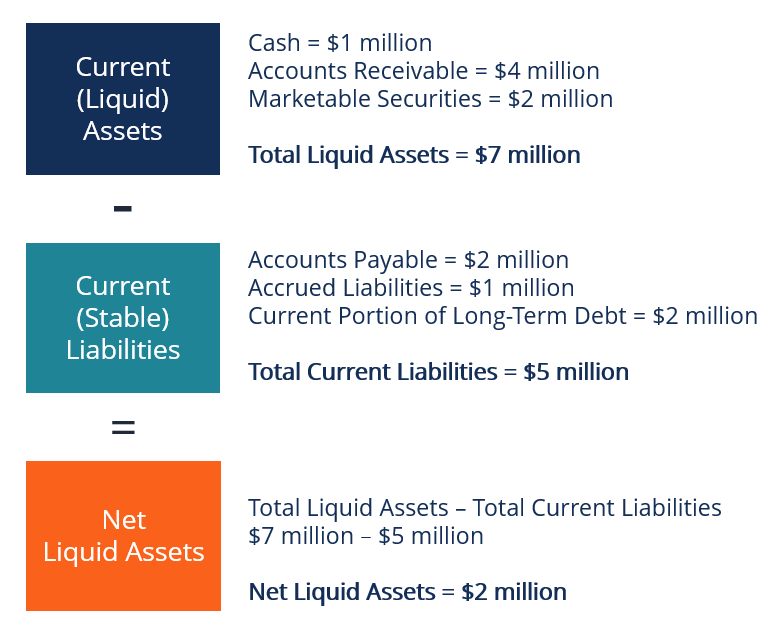

Figure 3 shows the actual calculation of net liquid assets for Company XYZ. Based on the figures, the company shows a net liquid position of +2 million, indicating that it is in a fairly comfortable position to meet its short-term obligations.

More Resources

CFI offers the Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful:

- Cash EquivalentsCash EquivalentsCash and cash equivalents are the most liquid of all assets on the balance sheet. Cash equivalents include money market securities, banker's acceptances

- Economic DepressionEconomic DepressionAn economic depression is an occurrence wherein an economy is in a state of financial turmoil, often the result of a period of negative activity based on the country’s Gross Domestic Product (GDP) rate. It is a lot worse than a recession, with GDP falling significantly, and usually lasts for many years.

- Inventory ValuationInventory ValuationInventory valuation refers to the practice of accounting for the value of a business' inventory. Business inventories refer to all the

- Dividend vs. Share RepurchaseDividend vs Share Buyback/RepurchaseShareholders invest in publicly traded companies for capital appreciation and income. There are two main ways in which a company returns profits to its shareholders – Cash Dividends and Share Buybacks. The reasons behind the strategic decision on dividend vs share buyback differ from company to company

-

Liquid Assets: Definition, Examples & Importance

A liquid asset is cash on hand or an asset other than cash that can be quickly converted into cash at a reasonable price. In other words, a liquid asset can be quickly sold on the market without a sig

-

Non-Operating Assets: Definition, Examples & Financial Impact

Non-operating assets are assets that are not required in the normal operations of a business but that can generate income nonetheless. The assets are recorded in the balance sheetBalance SheetThe bala

finance

- Fixed Assets: Definition, Examples & Importance for Businesses

- Monetary Assets: Definition, Examples & Key Characteristics

- Understanding Net Foreign Assets (NFA): A Comprehensive Guide

- Understanding Non-Monetary Assets: Definition & Examples

- Understanding Unrestricted Net Assets for Nonprofits

- Net Tangible Assets (NTA): Definition, Calculation & Importance

- Liquid Assets: Definition, Examples & Importance

- Understanding Liquid Assets: A Comprehensive Guide

- Liquid Assets: Definition, Importance & Examples | [Your Brand Name]

-

Understanding Intangible Assets: Definition & Importance

Understanding Intangible Assets: Definition & ImportanceAccording to the IFRS, intangible assets are identifiable, non-monetary assets without physical substance. Like all assets, intangible assets are expected to generate economic returns for the company ...

-

Understanding Net Sales: Definition & Importance

Understanding Net Sales: Definition & ImportanceNet sales are the total revenue generated by a company, excluding any sales returns, allowances, and discounts. It is a very important figure and is used by analysts when making decisions about the bu...