Understanding Seller's Discretionary Earnings: A Comprehensive Guide

Seller’s discretionary earnings is a cash-flowCash FlowCash Flow (CF) is the increase or decrease in the amount of money a business, institution, or individual has. In finance, the term is used to describe the amount of cash (currency) that is generated or consumed in a given time period. There are many types of CF based measure of business earnings in an owner-operated business. It comprises the profit before taxEarnings Before Tax (EBT)Earnings before tax, or pre-tax income, is the last subtotal found in the income statement before the net income line item. EBT is found and interest of a business before the owner’s benefits, non-cash expensesNon-Cash ExpensesNon cash expenses appear on an income statement because accounting principles require them to be recorded despite not actually being paid for with cash. , extraordinary one-time investments, and other non-related business incomes and expenses. This metric is used to measure the value of an organization in order to provide potential buyers with a better picture of their expected return on investmentReturn on Investment (ROI)Return on Investment (ROI) is a performance measure used to evaluate the returns of an investment or compare efficiency of different investments..

From the seller’s side, calculating the seller’s discretionary earnings allows them to maximize the value of the business before getting into a business sale negotiation with potential buyers. Understanding how to calculate the seller’s discretionary earnings allows the seller to make the right decision when choosing what expenses and incomes to include.

To Learn how to perform Valuation Methods such as DCF, Comps and Precedent Transactions, check out CFI’s Business Valuation Modeling Course.

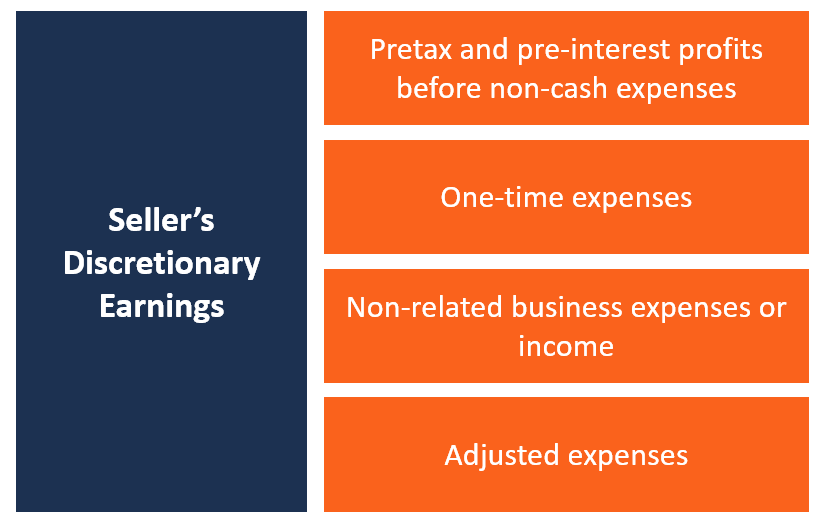

Components of the Seller’s Discretionary Earnings

When preparing a business for sale, there are various incomes and expenses that may or may not have an effect on the company’s valuation. Knowing what to include in the valuation can help both parties in the negotiation process reach a reasonable valuation of the business. Here are some of the items that are included when calculating the seller’s discretionary earnings:

#1 Pretax and pre-interest profits before non-cash expenses

This is the EBITDAEBITDAEBITDA or Earnings Before Interest, Tax, Depreciation, Amortization is a company's profits before any of these net deductions are made. EBITDA focuses on the operating decisions of a business because it looks at the business’ profitability from core operations before the impact of capital structure. Formula, examples (Earnings before Interest, Taxes, Depreciation, and Amortization), which shows how much the company is earning. It gives the investor an overview of the return on investment that they will get once they acquire the business.

#2 One-time expenses

One-time purchases include expenses that are non-recurring and are only paid once. The expenses may include payments for website design services, purchase of a business license, one-time application fees, legal fees, etc.

#3 Non-related business expenses or income

This comprises incomes and expenses that are not related to the business’ core operations. Typical non-related incomes and expenses include costs incurred on a business trip for a personal vacation, consulting income not related to the business activities, fuel and automobile expenses for a business that does not require automobiles, and office rentSG&ASG&A includes all non-production expenses incurred by a company in any given period. It includes expenses such as rent, advertising, marketing recorded as business expenses.

#4 Adjusted expenses

When selling a business, one must account for some of the expenses that are complementary to that business. For example, when a company is selling its branded t-shirts website, the new owner will need to factor in the expenses for warehouse rent and order fulfillment since they are crucial to the success of the business. Such expenses must be included when preparing the earnings statement for the business.

Areas of Disagreements between Buyers and Sellers

When calculating the seller’s discretionary earnings, there is a likelihood that the seller and the buyer will disagree on some of the incomes, expenses, and replacement costs that should be included in the calculations. The common areas of disagreements include:

#1 One-time expenses

Some of the expenses included under one-time expenses may be disputed by the potential buyer on the basis of whether they are one-time expenses or they will recur in the future. For example, license fees that are included as one-time expenses may need to be paid again in the future.

The same applies to web design fees since the new buyer will need to redesign the website after a few years to update it to the latest technologies. The buyer and the seller will need to agree on the appropriate items to be recorded as one-time expenses.

#2 Replacement owner’s benefits

Another item where the buyer and the seller may disagree is the replacement owner’s benefit. A business may have more than one owner, and this means that the value of the seller’s discretionary earnings may be overstated or understated. If a business has more than one owner earning an income from the business, only one owner’s benefit can be added back to the earnings for valuation purposes.

The other owner’s benefits should be adjusted to represent current market rates that are equal to what the new owner will pay a full-time employee to perform that function. The point of disagreement may be where the owner’s benefit represents reasonable value for the amount of work performed.

Similarities between Seller’s Discretionary Earnings and EBITDA

Both Seller’s Discretionary Earnings and Earnings before Interest, Taxes, Depreciation, and Amortization (EBITDA) attempt to calculate standardized earnings by excluding certain items that are variable from one business to another. For example, both metrics exclude interest expense on debt since each company has different debt levels. Including the expense may bring big variances in reported earnings.

Seller’s discretionary earnings are used when valuing smaller companies, while the EBITDA metric is more commonly used when valuing large companies.

Related Readings

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to transform anyone into a world-class financial analyst. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

- Interest ExpenseInterest ExpenseInterest expense arises out of a company that finances through debt or capital leases. Interest is found in the income statement, but can also

- Profitability RatiosProfitability RatiosProfitability ratios are financial metrics used by analysts and investors to measure and evaluate the ability of a company to generate income (profit) relative to revenue, balance sheet assets, operating costs, and shareholders' equity during a specific period of time. They show how well a company utilizes its assets to produce profit

- Projecting Income Statement Line ItemsProjecting Income Statement Line ItemsWe discuss the different methods of projecting income statement line items. Projecting income statement line items begins with sales revenue, then cost

- Statement of Cash FlowsStatement of Cash FlowsThe Statement of Cash Flows (also referred to as the cash flow statement) is one of the three key financial statements that report the cash

-

Understanding Earnings Announcements: A Comprehensive Guide

An earnings announcement is the public statement a company offers to reveal its profitability for a certain period of time. Most often, an earnings announcement details profit for a quarter or a year.

-

Understanding Earnings Calls: A Comprehensive Guide

An earnings call is a conference call (typically held in the form of a teleconference or a webcast) during which the management of a public companyPrivate vs Public CompanyThe main difference between

finance

- Understanding Operating Expenses (OpEx): A Comprehensive Guide

- Understanding Appraisals: A Comprehensive Guide

- Business Banking: Services, Accounts & Loans Explained

- Understanding Discretionary Expenses: Definition & Examples

- Understanding Discretionary Income: Definition & Examples

- Earnings Management: Definition, Techniques & Impact

- Understanding Earnings Volatility: Risk & Stock Price Prediction

- Understanding Business Erosion: Causes, Risks & Prevention

- Understanding Tax Deductions: What Businesses Need to Know

-

Drawing Account Explained: Understanding Owner Withdrawals

Drawing Account Explained: Understanding Owner WithdrawalsA drawing account is a financial account that essentially records owners’ drawings, i.e., the assets, mainly including money, that are withdrawn from a business by its owner(s) for their persona...

-

Understanding Earnings: A Guide to Financial Profitability

Understanding Earnings: A Guide to Financial ProfitabilityEarnings refer to the income that an individual or organization gains during a certain period. They can be found on a company’s income statement and are used to measure the profitability of that...