Simple vs. Compound Interest: Understanding the Difference

In this article, we will discuss simple interest vs compound interest and illustrate the major differences that can arise between them. Interest payments can be thought of as the price of borrowing funds in the market. They are paid by the borrower to the lender with the payment made at the end of the loan period. Interest payments are usually calculated as a proportion of the principal that the borrower borrowed from the lender.

Summary:

- Interest payments can be thought of as the price of borrowing funds in the market. Interest is paid by the borrower to the lender.

- Simple interest calculates the total interest payment using a fixed principal amount. The interest that is accrued over time is not added to the principal amount.

- Compound interest calculates the total interest payment using a variable principal amount. The interest that is accrued over time is added to the principal amount.

What is Simple Interest?

Simple interest calculates the total interest payment using a fixed principal amountPrincipal PaymentA principal payment is a payment toward the original amount of a loan that is owed. In other words, a principal payment is a payment made on a loan that reduces the remaining loan amount due, rather than applying to the payment of interest charged on the loan.. The interest that is accrued over time is not added to the principal amount. Consider the following example:

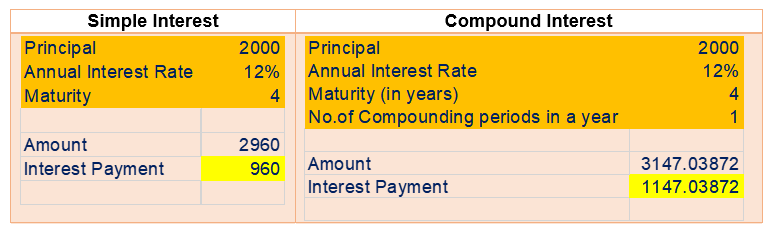

An investor invests $2,000 in a 4-year term deposit paying simple interest of 12%.

Total Interest Earned = Principal * Interest Rate * Time

= $2,000 * 12% * 4 = $960

Average Annual Interest Earned = Total Interest Earned / Time

= $960 / 4 = $240

Total Amount Repaid = Principal + Total Interest

= $2,000 + $960 = $2,960

What is Compound Interest?

Compound interest calculates the total interest payment using a variable principal amount. The interest that is accrued over time is added to the principal amount. For example, the interest for the first year is calculated as a proportion of the initial principal. The interest amount is then added to the initial principal, and the interest for the second year is calculated as a proportion of the revised principal. Consider the following example:

An investor invests $2,000 in a 4-year term deposit paying an annual interest of 12% with interest compounded annually.

Where:

- N is the number of times in a year the interest is compounded or added to the initial principal.

Total Interest Earned = $2,000 * [(1 + 12%)4 – 1] = $1,147.04

Average Annual Interest Earned = Total Interest Earned / Time

= $1,147.04 / 4 = $286.76

Simple Interest vs. Compound Interest

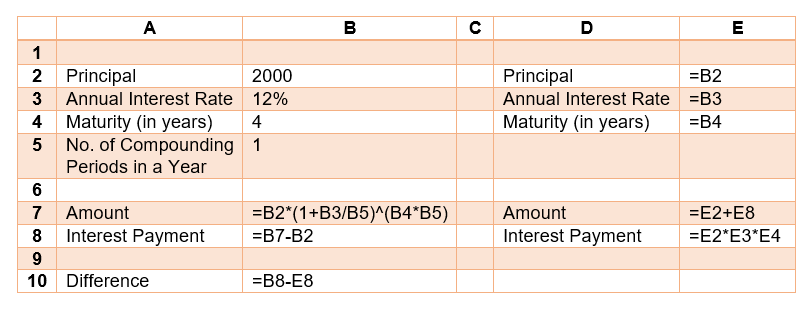

The following Excel spreadsheetExcel for BeginnersThis Excel for beginners guide teaches you everything you need to know about Excel spreadsheets and formulas to perform financial analysis. Watch the Video and learn everything a beginner needs to know from what is Excel, to why do we use, and what are the most important keyboard shortcuts, functions, and formulas can be used to illustrate the large differences between simple interest and compound interest payments:

Continuous Compounding

In the example above, interest was compounded on an annual basis. However, we could’ve just as easily compounded on a semi-yearly or a quarter-yearly basis. In fact, we could’ve also compounded the interest every day.

Continuous compounding recalculates the principal on a continuous basis. Continuously compounded interestContinuously Compounded InterestContinuously compounded interest is interest that is computed on the initial principal, as well as all interest other interest earned. The idea is that the principal will receive interest at all points in time, rather than in a discrete way at certain points in time. can be found using the following formula:

Where:

- e is Euler’s number ≈ 2.7183

Continuing with the example above, if $2,000 is lent out for 4 years at an annual interest rate of 12% and the interest is compounded continuously, the total interest earned is $1,232.15. The result can be verified by setting the number of compounding periods in the Excel spreadsheet to a very large number (such as 100,000).

More Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Annual Percentage Rate (APR)Annual Percentage Rate (APR)The Annual Percentage Rate (APR) is the yearly rate of interest that an individual must pay on a loan, or that they receive on a deposit account. Ultimately, APR is a simple percentage term used to express the numerical amount paid by an individual or entity yearly for the privilege of borrowing money.

- Continuously Compounded InterestContinuously Compounded InterestContinuously compounded interest is interest that is computed on the initial principal, as well as all interest other interest earned. The idea is that the principal will receive interest at all points in time, rather than in a discrete way at certain points in time.

- Effective Annual Interest RateEffective Annual Interest RateThe Effective Annual Interest Rate (EAR) is the interest rate that is adjusted for compounding over a given period. Simply put, the effective

- Interest PayableInterest PayableInterest Payable is a liability account shown on a company’s balance sheet that represents the amount of interest expense that has accrued

-

Principal Curtailment: Definition, Benefits & Tax Implications

A principal curtailment is a mortgage payment sent in by a homeowner before it's due in order to reduce the principal balance on the mortgage. Individual mortgage contracts also come with their ow

-

Accrued vs. Regular Interest: Understanding the Difference

When investing in stocks and bonds, investors are paid either an accrued interest vs regular interest at an agreed period. The interest payments are not paid immediately, and security issuers will owe

finance

- Compound Interest Explained: How to Grow Your Wealth

- Understanding Add-On Interest: How It Works & Loan Payments

- Compound Interest Explained: How It Works & Benefits

- Compound Interest Formula: Calculate & Understand Growth

- Understanding Continuously Compounded Interest & Key Financial Ratios

- Simple Interest Explained: Calculation, Benefits & Examples

- Compound Interest: Understand the Power of Exponential Growth

- Compound Interest Explained: How It Works & Benefits

- Simple vs. Compound Interest: Understand the Difference & Impact

-

Simple vs. Compound Interest: Understanding the Difference & Benefits

Simple vs. Compound Interest: Understanding the Difference & BenefitsCompounded interest yields higher amounts than simple interest. Interest on savings accounts and other types of accounts is calculated using either simple or compounding interest. Simple inte...

-

Notional Principal Amount: Definition & Explained

Notional Principal Amount: Definition & ExplainedThe notional principal amount refers to the predetermined dollar amount in an interest rate swapInterest Rate SwapAn interest rate swap is a derivative contract through which two counterparties agree ...