Treasury Stock: Definition, Purpose & Implications

Treasury stock, or reacquired stock, is the previously issued, outstanding shares of stock which a company repurchased or bought back from shareholders. The reacquired shares are then held by the company for its own disposition. They can either remain in the company’s possession to be sold in the future, or the business can retire the shares and they will be permanently out of market circulation.

Treasury stock is one of the various types of equity accountsEquity AccountsEquity accounts consist of common stock, preferred stock, share capital, treasury stock, contributed surplus, additional paid-in capital, reported on the balance sheet statement under the stockholders’ equity section as a contra-equity account.

Understanding Where Treasury Stocks Come From

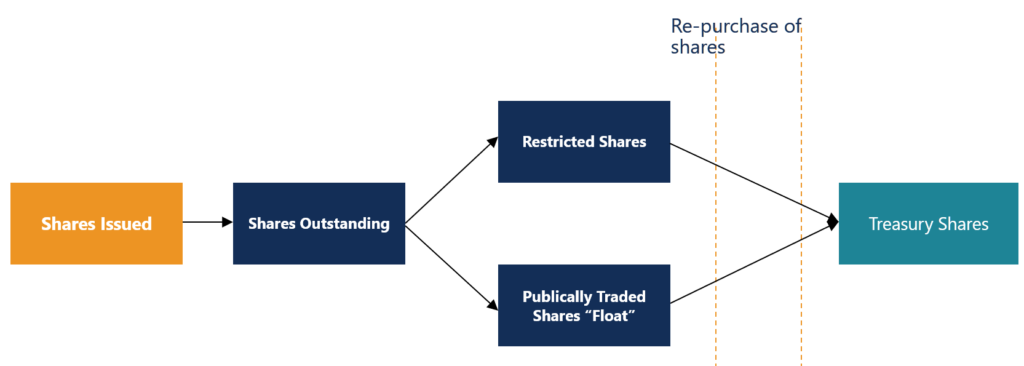

Every company is authorized to issue a certain number of shares. This is referred to as “shares outstanding,” or the total shares that exist for a company. Of those outstanding shares, some shares are restricted (meaning they cannot be traded unless certain conditions are met) while most shares are publicly traded (known as the “float”).

Treasury stocks are shares that were originally part of “shares outstanding” but that have been repurchased by the company.

Rationale Behind Share Repurchases

There are several reasons why companies reacquire issued and outstanding shares from the investors.

1. For reselling

Treasury stock is often a form of reserved stock set aside to raise funds or pay for future investments. Companies may use treasury stock to pay for an investment or acquisition of competing businesses. These shares can also be reissued to existing shareholders to reduce dilution from incentive compensation plans Stock OptionA stock option is a contract between two parties which gives the buyer the right to buy or sell underlying stocks at a predetermined price and within a specified time period. A seller of the stock option is called an option writer, where the seller is paid a premium from the contract purchased by the stock option buyer.for employees.

2. For controlling interest

The repurchase action lowers the number of outstanding shares, therefore, increasing the value of the remaining shareholders’ interest in the company. The reacquisition of stock can also prevent hostile takeovers when the company’s management does not want the acquisition deal to push through.

3. Undervaluation

When the market is not performing well, the company’s stock may be undervalued – buying back the shares will usually boost the share price and benefit the remaining shareholders.

4. Retiring of shares

When treasury stocks are retired, they can no longer be sold and are taken out of the market circulation. In turn, the share count is permanently reduced, which causes the remaining shares present in circulation to represent a larger percentage of shareholder ownership, including dividends and profits.

5. For improving financial ratiosEarnings Per Share Formula (EPS)EPS is a financial ratio, which divides net earnings available to common shareholders by the average outstanding shares over a certain period of time. The EPS formula indicates a company’s ability to produce net profits for common shareholders.

If there is a sound motive for the buyback of stocks, the improvement of financial ratios may just be an after-effect of such good management decisions. This results in an increase in the return on assets (ROA)Return on Assets & ROA FormulaROA Formula. Return on Assets (ROA) is a type of return on investment (ROI) metric that measures the profitability of a business in relation to its total assets. ratio and return on equity (ROE)Return on Equity (ROE)Return on Equity (ROE) is a measure of a company’s profitability that takes a company’s annual return (net income) divided by the value of its total shareholders' equity (i.e. 12%). ROE combines the income statement and the balance sheet as the net income or profit is compared to the shareholders’ equity. ratio. This then illustrates positive company market performance.

What are the Limitations of Treasury Stock?

- No voting rights

- Not entitled to receive dividends

- Not included in the calculation of outstanding shares

- Do not exercise preemptive rights as a shareholder

- Not entitled to receive net assets in case the company liquidates

- In some countries, the number of treasury stocks held by companies is regulated – total treasury stock cannot exceed the maximum proportion of capitalization specified by law.

How do Companies Perform a Buyback of Stocks?

A stock buyback, or share repurchase, is one of the techniques used by management to reduce the number of outstanding shares circulating in the market. It benefits the company’s owners and investors because the relative ownership of the remaining shareholders increases. There are three methods by which a company may carry out the repurchase:

1. Tender offer

The company offers to repurchase a number of shares from the shareholders at a specified price it is willing to pay, which is most likely at a premium or above market price. The company will also disclose the duration for which this offer is valid, and shareholders are welcome to tender their shares to the company should they be willing to sell at the specified price.

2. Open market or direct repurchase

Direct buying of shares in the open market. When a company announces the repurchase of stocks, it often causes the share price to increase, which is perceived by the market as a positive outcome. The company then simply proceeds to purchase shares as other investors would on the market.

3. Dutch auction

In a Dutch auctionDutch AuctionA Dutch auction is a price discovery process where the auctioneer starts with the highest asking price and lowers it until it reaches an optimum price level, the company specifies a range, and the number of shares it wishes to repurchase. Shareholders are invited to offer their shares for sale at their personally desired price, within or below this range. The company will then purchase their desired number of shares for the lowest cost possible, by purchasing from shareholders who have offered at the lower end of the range.

Learn More

To keep advancing your career, the additional CFI resources below will be useful:

- LBOLeveraged Buyout (LBO)A leveraged buyout (LBO) is a transaction where a business is acquired using debt as the main source of consideration.

- Earnings-per-Share RatioEarnings Per Share Formula (EPS)EPS is a financial ratio, which divides net earnings available to common shareholders by the average outstanding shares over a certain period of time. The EPS formula indicates a company’s ability to produce net profits for common shareholders.

- Fixed Asset TurnoverFixed Asset TurnoverFixed Asset Turnover (FAT) is an efficiency ratio that indicates how well or efficiently the business uses fixed assets to generate sales. This ratio divides net sales into net fixed assets, over an annual period. The net fixed assets include the amount of property, plant, and equipment less accumulated depreciation

- Inventory Write-DownInventory Write DownAn inventory write down is an accounting process used to record the reduction of an inventory’s value, and is required when the inventory's

-

Understanding Overweight Stocks: A Comprehensive Guide

An overweight stockCommon StockCommon stock is a type of security that represents ownership of equity in a company. There are other terms – such as common share, ordinary share, or voting share

-

Stock Indexes Explained: A Beginner's Guide to Market Benchmarks

A stock index, also called a share index or stock market index, consists of constituent stocks used to provide an indication of an economy, market, or sector. A stock index is commonly used by investo

finance

- Treasury Stock: Definition, Purpose & Impact on Share Count

- Authorized Stock: Understanding Share Issuance Limits

- Founders Stock: Definition, Vesting, and Key Differences

- Restricted Stock: Definition, Types & How It Works

- Floating Stock Explained: Understanding Publicly Traded Shares

- Stock-Based Compensation (SBC): A Comprehensive Guide

- Treasury Stock Method: Calculating Diluted Earnings Per Share

- Understanding Ordinary Shares: A Beginner's Guide to Common Stock

- Understanding Stock Dilution: Causes, Effects & How to Protect Yourself

-

Understanding Downtrends: Definition, Identification & Reversal

Understanding Downtrends: Definition, Identification & ReversalA downtrend describes the movement of a stock towards a lower price from its previous state. It will exist as long as there is a continuation of lower highs and lower lows in the stock chart. The down...

-

Understanding Non-Assessable Stock: Limited Liability Explained

Understanding Non-Assessable Stock: Limited Liability ExplainedNon-assessable stock is a class of stock ownership where the stock owner is limited in their liability to the amount paid for the stock. It means that in the instance of bankruptcyBankruptcyBankruptcy...