SEC Form S-1: Your Guide to IPO Registration

SEC Form S-1 is a filing needed to register the securities of companies that wish to go public with the U.S. Securities and Exchange Commission (SEC). It is required under the Securities Act of 1933The 1933 Securities ActThe 1933 Securities Act was the first major federal securities law passed following the stock market crash of 1929. The law is also referred to as the Truth in Securities Act, the Federal Securities Act, or the 1933 Act. It was enacted on May 27, 1933 during the Great Depression. ...the law was aimed at correcting some of the wrongdoings and is also known as the Registration Statement Under the Securities Act of 1933.

SEC Form S-1 is used to register the securities of all registrants except for the securities of foreign governments or political subdivisions.

What Information Does SEC Form S-1 Require?

The SEC Form S-1 requires companies to provide certain basic information regarding their business and finances. It includes:

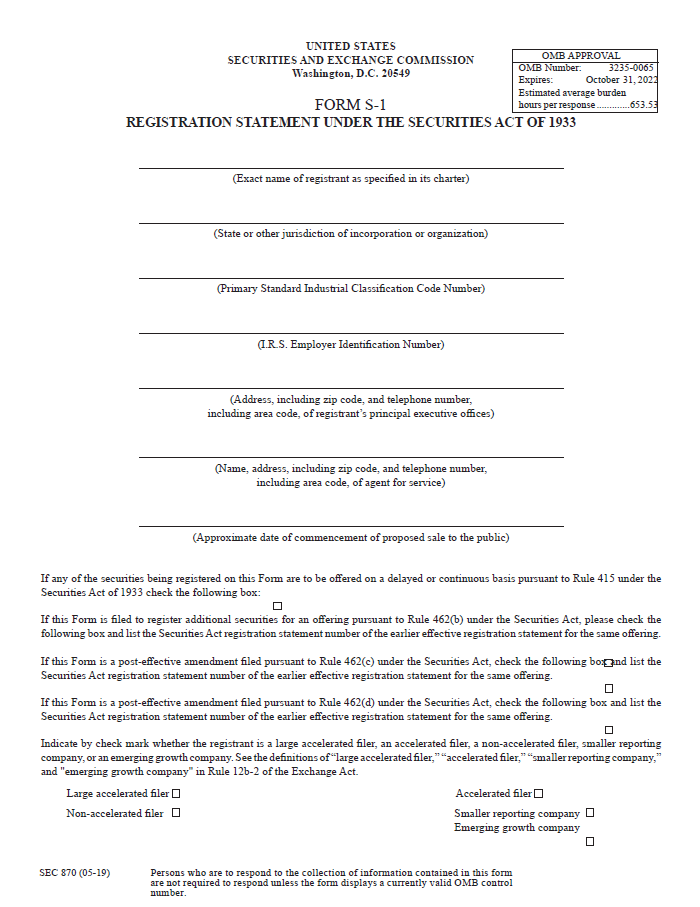

- The registrant’s exact name, as specified in its charter

- The state or jurisdiction in which the company is incorporated or organized

- R.S. Employer Identification Number

- Information regarding the registrant’s principal executive offices, including the address and telephone number

- Approximate date of the beginning of the proposed sale to the public

The SEC Form S-1 also requires registrants to provide an investment prospectusProspectusA prospectus is a legal disclosure document that companies are required to file with the Securities and Exchange Commission (SEC). The document provides information about the company, its management team, recent financial performance, and other related information that investors would like to know. so that investors can make informed decisions about whether to invest in the company. The specific information required in the prospectus consists of various items, including:

- Summary information

- Risk factors

- Ratio of earnings to fixed charges

- Use of proceedsUse of Proceeds StatementThe use of proceeds statement is a short document that summarizes how a company that aims to secure additional capital is going to spend the funds. In other words, the document provides the reader with a snapshot of what aspects of the business the company will spend money on.

- Determination of offering price

- Plan of distribution

- Description of securities to be registered

- Interests of named experts and counsel

- Description of business, property, legal proceedings, and selected financial data

- Directors and executive officers

- Quantitative and qualitative disclosures about market risk

- Material changes in the company’s affairs since the end of the latest fiscal year

- The registrant’s latest annual report

The SEC Form S-1 specifies certain information not required in the investment prospectus. They include:

- Indemnification of directors and officers

- Recent sales of unregistered securities

- Other expenses of issuance and distribution

How is SEC Form S-1 Completed?

Although SEC Form S-1 is only eight pages long, it requires information from a wide range of sources using many rules and regulations. Independent accountants need to certify the financial statements required by the filing. Significant time and effort are required to fill out the form, with the OMB Office estimating an average time burden of over 970 hours.

Once completed, S-1 forms may be filed with the SEC’s EDGAR filing systemUS - EDGAREDGAR is a database where U.S. public companies file regulatory documents such as annual reports, quarterly reports, 10-K, 10-Q, prospectus every business day from 10:00 a.m. to 5:00 p.m. A live feed of recent SEC Form S-1 filings is public and can be found online.

Registration Fee

The registration fee required to submit SEC Form S-1 varies by company and depends on factors including:

- The number of securities to be registered

- The proposed maximum offering price per unit

- The proposed maximum aggregate offering price

Registration of Additional Securities

If a company that has already filed the SEC Form S-1 wants to register additional securities at a later date, it is not obligated to file another form of the same type. Instead, the registrant may file a separate registration statement which consists only of:

- The facing page

- A statement that the contents of the earlier registration statement are incorporated by reference

- Required opinions and consents

- The signature page

- Any price-related information the earlier registration statement omitted

Additional Information

To file amendments to a previously filed SEC Form S-1, companies are required to complete the related SEC Form S-1/A.

A more simplified form, SEC Form S-3, may be used only by companies required to file under the Securities Exchange Act of 1934. To be eligible to use the form, certain requirements must be met by both the offering and the issuer.

More Resources

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program, designed to transform anyone into a world-class financial analyst.

In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful:

- DisclosureDisclosureDisclosure, in financial terms, basically refers to the action of making all relevant information about a business available to the public in

- Market RiskMarket RiskMarket risk, also known as systematic risk, refers to the uncertainty associated with any investment decision. Price volatility often arises due to

- Shareholder RegisterShareholder RegisterA shareholder register is a list of all active and former owners of a company's shares. The register includes details of shareholders such as

- Types of SEC FilingsTypes of SEC FilingsThe US SEC makes it mandatory for publicly traded companies to submit different types of SEC filings, forms include 10-K, 10-Q, S-1, S-4, see examples. If you are a serious investor or finance professional, knowing and being able to interpret the various types of SEC filings will help you in making informed investment decisions.

-

Selling Away: Understanding Conflicts of Interest in Investing

Selling away is an inappropriate practice by an investment professional – such as a financial adviser or stockbroker – who sells or solicits a client to purchase securities not approved by

-

1933 Securities Act: Protecting Investors & Market Integrity

The 1933 Securities Act was the first major federal securities law passed following the stock market crash of 1929. The law is also referred to as the Truth in Securities Act, the Federal Securities A

invest

- Understanding Depositories: Secure Storage for Financial Securities

- Accredited Investors: Definition & Requirements | SEC

- Disgorgement Explained: Legal Remedy for Illegal Profits

- Understanding Distressed Securities: Risks & Opportunities

- Non-Marginable Securities: Definition & Investing Implications

- Understanding Non-Marketable Securities: Definition & Examples

- Understanding Security Quality: A Guide to Investment Risk

- Understanding SEC Yield: A Guide for Bond Investors

- SEC Explained: Your Guide to the U.S. Securities Regulator

-

Understanding Non-Covered Securities: Definition & SEC Role

Understanding Non-Covered Securities: Definition & SEC RoleThe term non-covered security refers to a legal definition of securities, the details of which may not necessarily be disclosed to the Internal Revenue Service (IRS). The competent authority that make...

-

Restricted Stock Lists: Understanding Employee Trading Restrictions

Restricted Stock Lists: Understanding Employee Trading RestrictionsA Restricted List is a list of securities that a bank’s employees are prohibited from buying or selling, either themselves or via any other person or third party. When are stocks placed on ...