Understanding the Accounting Cycle: A Comprehensive Guide

The accounting cycle is the holistic process of recording and processing all financial transactions of a company, from when the transaction occurs, to its representation on the financial statementsThree Financial StatementsThe three financial statements are the income statement, the balance sheet, and the statement of cash flows. These three core statements are, to closing the accounts. One of the main duties of a bookkeeperJobsBrowse job descriptions: requirements and skills for job postings in investment banking, equity research, treasury, FP&A, corporate finance, accounting and other areas of finance. These job descriptions have been compiled by taking the most common lists of skills, requirement, education, experience and other is to keep track of the full accounting cycle from start to finish. The cycle repeats itself every fiscal year as long as a company remains in business.

The accounting cycle incorporates all the accounts, journal entries, T accountsT Accounts GuideIf you want a career in accounting, T Accounts may be your new best friend. The T Account is a visual representation of individual accounts, debits, and credits, adjusting entries over a full cycle.

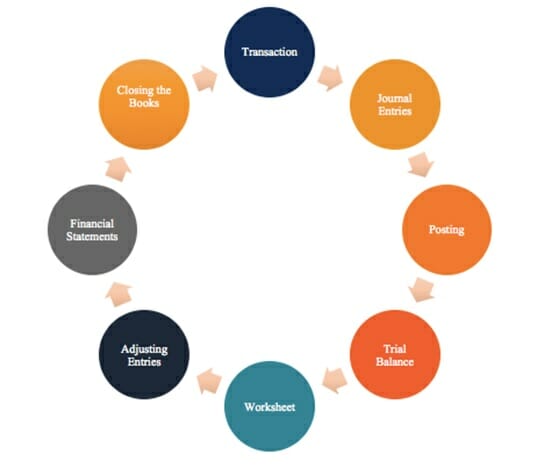

Steps in the Accounting Cycle

#1 Transactions

Transactions: Financial transactions start the process. If there were no financial transactions, there would be nothing to keep track of. Transactions may include a debt payoff, any purchases or acquisition of assets, sales revenue, or any expenses incurred.

#2 Journal Entries

Journal EntriesJournal Entries GuideJournal Entries are the building blocks of accounting, from reporting to auditing journal entries (which consist of Debits and Credits): With the transactions set in place, the next step is to record these entries in the company’s journal in chronological order. In debiting one or more accounts and crediting one or more accounts, the debits and credits must always balance.

#3 Posting to the General Ledger (GL)

Posting to the GL: The journal entries are then posted to the general ledger where a summary of all transactions to individual accounts can be seen.

#4 Trial Balance

Trial Balance: At the end of the accounting period (which may be quarterly, monthly, or yearly, depending on the company), a total balance is calculated for the accounts.

#5 Worksheet

Worksheet: When the debits and credits on the trial balance don’t match, the bookkeeper must look for errors and make corrective adjustments that are tracked on a worksheet.

#6 Adjusting Entries

Adjusting EntriesAdjusting EntriesThis guide to adjusting entries covers deferred revenue, deferred expenses, accrued expenses, accrued revenues and other adjusting journal: At the end of the company’s accounting period, adjusting entries must be posted to accounts for accruals and deferrals.

#7 Financial Statements

Financial StatementsThree Financial StatementsThe three financial statements are the income statement, the balance sheet, and the statement of cash flows. These three core statements are: The balance sheet, income statement, and cash flow statement can be prepared using the correct balances.

#8 Closing

Closing: The revenue and expense accounts are closed and zeroed out for the next accounting cycle. This is because revenue and expense accounts are income statement accounts, which show performance for a specific period. Balance sheet accounts are not closed because they show the company’s financial position at a certain point in time.

General Ledger

The general ledger serves as the eyes and ears of bookkeepers and accountants and shows all financial transactions within a business. Essentially, it is a huge compilation of all transactions recorded on a specific document or in accounting software.

For example, if you want to see the changes in cash levels over the course of the business and all their relevant transactions, you would look at the general ledger, which shows all the debits and credits of cash.

Accounting Cycle Fundamentals

To fully understand the accounting cycle, it’s important to have a solid understanding of the basic accounting principles. You need to know about revenue recognitionRevenue RecognitionRevenue recognition is an accounting principle that outlines the specific conditions under which revenue is recognized. In theory, there is a (when a company can record sales revenue), the matching principleMatching PrincipleThe matching principle is an accounting concept that dictates that companies report expenses at the same time as the revenues they are related (matching expenses to revenues), and the accrual principleAccrual AccountingIn financial accounting, accruals refer to the recording of revenues that a company has earned but has yet to receive payment for, and the.

The fundamental concepts above will enable you to construct an income statement, balance sheet, and cash flow statement, which are the most important steps in the accounting cycle. To learn more, check out CFI’s free Accounting Fundamentals Course.

Additional Resources

Thanks for checking out CFI’s guide and overview of the accounting cycle. CFI is the official global provider of the Financial Modeling and Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification, designed to transform anyone into a world-class financial analyst. To learn more, see the additional CFI resources below:

- Financial Accounting TheoryFinancial Accounting TheoryFinancial Accounting Theory explains the why behind accounting - the reasons why transactions are reported in certain ways. This guide will

- Analysis of Financial StatementsAnalysis of Financial StatementsHow to perform Analysis of Financial Statements. This guide will teach you to perform financial statement analysis of the income statement,

- Revenue Recognition PrincipleRevenue Recognition PrincipleThe revenue recognition principle dictates the process and timing by which revenue is recorded and recognized as an item in a company's

- Accounting CareersAccountingPublic accounting firms consist of accountants whose job is serving business, individuals, governments & nonprofit by preparing financial statements, taxes

-

Allowance for Doubtful Accounts: Definition & Purpose

The allowance for doubtful accounts is a contra-asset account that is associated with accounts receivableAccounts ReceivableAccounts Receivable (AR) represents the credit sales of a business, which ha

-

Cash Conversion Cycle (CCC): Definition & Analysis

The Cash Conversion Cycle (CCC) is a metric that shows the amount of time it takes a company to convert its investments in inventoryInventoryInventory is a current asset account found on the balance s

Accounting

- Accounts Payable vs. Accounts Receivable: A Clear Explanation

- Understanding the Accounting Equation: Assets = Liabilities + Equity

- Accrual Accounting Principle: Definition & Explanation

- Understanding the Chart of Accounts: A Comprehensive Guide

- Understanding the Expanded Accounting Equation: A Comprehensive Guide

- Understanding the GAAP Hierarchy: A Comprehensive Guide

- Understanding the Philosophy of Accounting: Principles & Concepts

- Understanding the Accounting Reporting Cycle: A Comprehensive Guide

- Understanding the Accounting Cycle: A Comprehensive Guide

-

Understanding Accounting Methods: Cash vs. Accrual

Understanding Accounting Methods: Cash vs. AccrualAn accounting method refers to a set of rules that a company adheres to when keeping its financial records and reporting financial transactions. The transactions are recorded in a manner that accurate...

-

Understanding the Acquisition and Payment Cycle: A Comprehensive Guide

Understanding the Acquisition and Payment Cycle: A Comprehensive GuideThe Acquisition and Payment Cycle (also referred to as the PPP Cycle for Purchases, Payables, and Payments) consists mainly of two classes of transactions. The first class is the acquisition class. Th...