Understanding the Chart of Accounts: A Comprehensive Guide

The chart of accounts is a tool that lists all the financial accounts included in the financial statementsThree Financial StatementsThe three financial statements are the income statement, the balance sheet, and the statement of cash flows. These three core statements are of a company. It provides a way to categorize all of the financial transactions that a company conducted during a specific accounting period.

Companies often use the chart of accounts to organize their records by providing a complete list of all the accounts in the general ledger of the business. The chart makes it easy to prepare information for evaluating the financial performance of the company at any given time.

The chart of accounts provides the name of each account listed, a brief description, and identification codes that are specific to each account. The balance sheet accounts are listed first, followed by the accounts in the income statement.

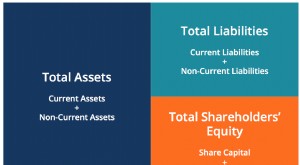

The balance sheet accounts comprise assets, liabilities, and shareholders equityStockholders EquityStockholders Equity (also known as Shareholders Equity) is an account on a company's balance sheet that consists of share capital plus, and the accounts are broken down further into various subcategories. The accounts in the income statement comprise revenues and expenses, and these accounts are also broken down further into sub-categories.

Setting Up the Chart of Accounts

When setting up a chart of accounts, typically, the accounts that are listed will depend on the nature of the business. For example, a taxi business will include certain accounts that are specific to the taxi business, in addition to the general accounts that are common to all businesses. For example, the taxi business will include a fuel expense account that is not common to all businesses, but it will leave out an inventory account since the taxi business is a service business that does not hold stock.

Typically, when listing accounts in the chart of accounts, you should use a numbering system for easy identification. Numbering also makes it easy to record a transaction. Small businesses commonly use three-digit numbers, while large businesses use four-digit numbers to allow room for additional numbers as the business grows.

Groups of numbers are assigned to each of the five main categories, while blank numbers are left at the end to allow for additional accounts to be added in the future. Also, the numbering should be consistent to make it easier for management to roll up information of the company from one period to the next.

Example: A large business numbering system

- Assets: 1000-1999

- Liabilities: 2000-2999

- Shareholder’s equity: 3000-3999

- Revenue: 4000-4999

- Expenses: 5000-5999

Categories on the Chart of Accounts

Each of the accounts in the chart of accounts corresponds to the two main financial statements, i.e., the balance sheet and income statement.

Balance sheet accounts

Such accounts are required when creating a balance sheet for the business. Balance sheet accounts comprise the following:

1. Asset accounts

The asset account provides a list of all the categories of assets that the business owns. The account may include intangible assetsIntangible AssetsAccording to the IFRS, intangible assets are identifiable, non-monetary assets without physical substance. Like all assets, intangible assets (such as trademarks, patents, and software), current assets (such as cash on hand, accounts receivable, and

Each asset account can be numbered in a sequence such as 1000, 1020, 1040, 1060, etc. The numbering follows the traditional format of the balance sheet by starting with the current assets, followed by the fixed assets.

2. Liability accounts

Liability accounts provide a list of categories for all the debts that the business owes its creditors. Typically, liability accounts will include the word “payable” in their name and may include accounts payableAccounts PayableAccounts payable is a liability incurred when an organization receives goods or services from its suppliers on credit. Accounts payables are, invoices payable, salaries payable, interest payable, etc.

Liability accounts also follow the traditional balance sheet format by starting with the current liabilities, followed by long-term liabilities. The number system for each liability account can start from 2000 and use a sequence that is easy to follow and compare in different accounting periods.

3. Owner’s equity accounts

Equity represents the value that is left in the business after deducting all the liabilities from the assets. Owner’s equityOwner’s EquityOwner's Equity is defined as the proportion of the total value of a company’s assets that can be claimed by the owners (sole proprietorship or partnership) and by the shareholders (if it is a corporation). It is calculated by deducting all liabilities from the total value of an asset (Equity = Assets – Liabilities). measures how valuable the company is to the shareholders of the company.

Some of the components of the owner’s equity accounts include common stock, preferred stock, and retained earnings. The numbering system of the owner’s equity account for a large company can continue from the liability accounts and start from 3000 to 3999.

Income statement accounts

The main components of the income statement accounts include the revenue accounts and expense accounts.

1. Revenue accounts

Revenue accounts capture and record the incomes that the business earns from selling its products and services. It only includes revenues related to the core functions of the business and excludes revenues that are unrelated to the main activities of the business.

Some of the sub-categories that may be included under the revenue account include sales discounts account, sales returns account, interest income account, etc. Numbering for each revenue account can start from 4000.

2. Expense accounts

The expense account is the last category in the chart of accounts. It includes a list of all the accounts used to capture the money spent in generating revenues for the business. The expenses can be tied back to specific products or revenue-generating activities of the business.

A simple way to organize the expense accounts is to create an account for each expense listed on IRS Tax Form Schedule CSchedule CThe Schedule C tax form is used to report profit or loss from a business. It is a form that sole proprietors (single owners of businesses) and adding other accounts that are specific to the nature of the business. Each of the expense accounts can be assigned numbers starting from 5000.

Summary

Setting up a chart of accounts can provide a helpful tool that enables a company’s management to easily record transactions, prepare financial statements, and review revenues and expenses in detail.

Additional Resources

Thank you for reading CFI’s explanation of a chart of accounts. CFI offers the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

- Financial Accounting TheoryFinancial Accounting TheoryFinancial Accounting Theory explains the why behind accounting - the reasons why transactions are reported in certain ways. This guide will

- How the 3 Financial Statements are LinkedHow the 3 Financial Statements are LinkedHow are the 3 financial statements linked together? We explain how to link the 3 financial statements together for financial modeling and

- Projecting Balance Sheet Line ItemsProjecting Balance Sheet Line ItemsProjecting balance sheet line items involves analyzing working capital, PP&E, debt share capital and net income. This guide breaks down how to calculate

- Projecting Income Statement Line ItemsProjecting Income Statement Line ItemsWe discuss the different methods of projecting income statement line items. Projecting income statement line items begins with sales revenue, then cost

-

Understanding the Accounting Equation: Assets = Liabilities + Equity

The accounting equation is a basic principle of accounting and a fundamental element of the balance sheetBalance SheetThe balance sheet is one of the three fundamental financial statements. The financ

-

Understanding Average Inventory: Definition & Calculation

The average inventory is the mean value (that can be different from the median value) of an inventory during a determined period of time. The average inventory is thus a mathematical calculation. It e

Accounting

- Accounts Payable vs. Accounts Receivable: A Clear Explanation

- Accounts Payable (AP): Definition, Function & Importance

- Business Visibility: Forecasting Performance & Driving Success

- Heikin-Ashi: A Comprehensive Guide to Trend Analysis

- Understanding the Accounting Cycle: A Comprehensive Guide

- Accounts Payable Turnover Ratio: Definition & Interpretation

- Accounts Receivable Turnover Ratio: Definition & Calculation

- Understanding Accounts Receivable Quality: A Key Indicator of Financial Health

- Chart of Accounts for Small Businesses: A Comprehensive Guide

-

Dow 30 Explained: Understanding the Dow Jones Industrial Average

Dow 30 Explained: Understanding the Dow Jones Industrial AverageThe Dow 30, or Dow Jones Industrial Average, is a stock index that tracks the performance of the 30 biggest companies listed on the stock indices in the United States. Despite being used by analysts t...

-

![Rule of 72: Calculate Investment Doubling Time | [Your Brand Name]](https://www.etffin.com/article/uploadfiles/202110/2021100815281678_S.png) Rule of 72: Calculate Investment Doubling Time | [Your Brand Name]

Rule of 72: Calculate Investment Doubling Time | [Your Brand Name]In finance, the Rule of 72 is a formula that estimates the amount of time it takes for an investment to double in value, earning a fixed annual rate of returnRate of ReturnThe Rate of Return (ROR) is ...