Understanding the Accounting Equation: Assets = Liabilities + Equity

The accounting equation is a basic principle of accounting and a fundamental element of the balance sheetBalance SheetThe balance sheet is one of the three fundamental financial statements. The financial statements are key to both financial modeling and accounting.. The equation is as follows:

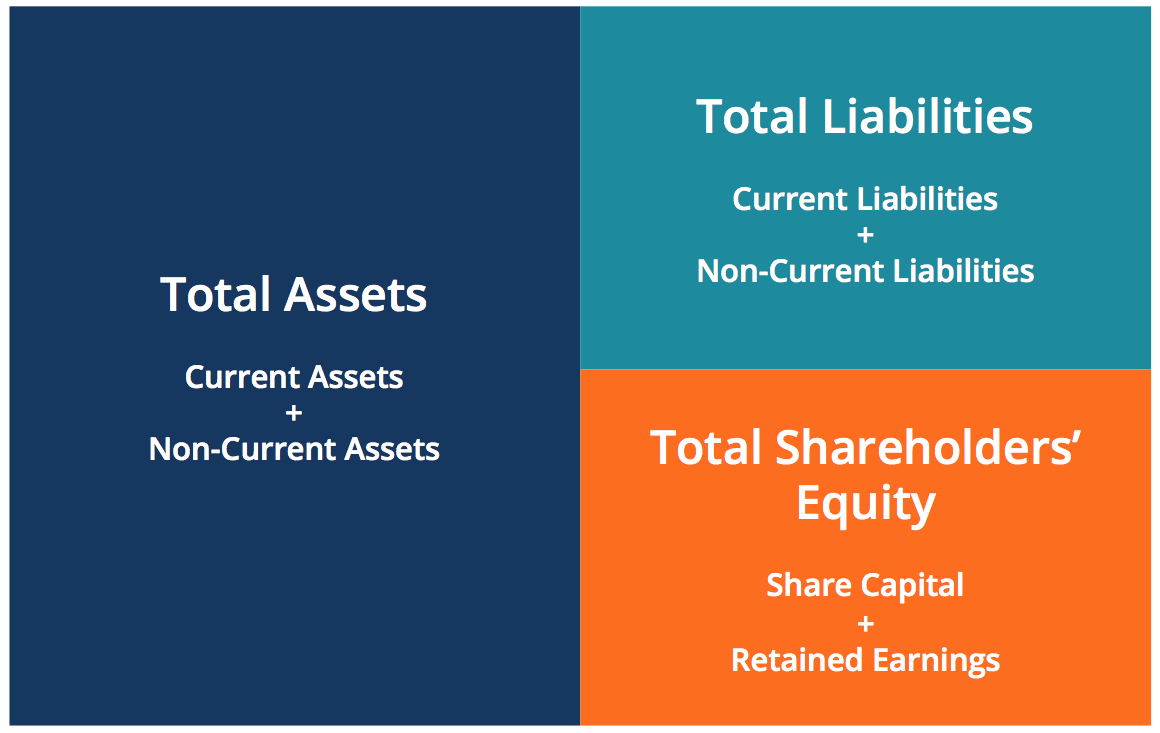

Assets = Liabilities + Shareholder’s Equity

This equation sets the foundation of double-entry accounting and highlights the structure of the balance sheet. Double-entry accounting is a system where every transaction affects both sides of the accounting equation. For every change to an asset account, there must be an equal change to a related liability or shareholder’s equity account. It is important to keep the accounting equation in mind when performing journal entries.Journal Entries GuideJournal Entries are the building blocks of accounting, from reporting to auditing journal entries (which consist of Debits and Credits)

The balance sheet is broken down into three major sections and their various underlying items: Assets, Liabilities, and Shareholder’s Equity.

Learn to read a balance sheet and other financial statements with CFI’s reading financial statements course!

Below are some examples of items that fall under each section:

- Assets: Cash,Current AssetsCurrent assets are all assets that a company expects to convert to cash within one year. They are commonly used to measure the liquidity of a Accounts ReceivableAccounts ReceivableAccounts Receivable (AR) represents the credit sales of a business, which have not yet been collected from its customers. Companies allow, InventoryInventoryInventory is a current asset account found on the balance sheet, consisting of all raw materials, work-in-progress, and finished goods that a, EquipmentPP&E (Property, Plant and Equipment)PP&E (Property, Plant, and Equipment) is one of the core non-current assets found on the balance sheet. PP&E is impacted by Capex,

- Liabilities: Accounts PayableAccounts PayableAccounts payable is a liability incurred when an organization receives goods or services from its suppliers on credit. Accounts payables are, Short-term borrowingsCurrent LiabilitiesCurrent liabilities are financial obligations of a business entity that are due and payable within a year. A company shows these on the, Long-term DebtLong Term DebtLong Term Debt (LTD) is any amount of outstanding debt a company holds that has a maturity of 12 months or longer. It is classified as a non-current liability on the company’s balance sheet. The time to maturity for LTD can range anywhere from 12 months to 30+ years and the types of debt can include bonds, mortgages

- Shareholder’s Equity: Share CapitalShare CapitalShare capital (shareholders' capital, equity capital, contributed capital, or paid-in capital) is the amount invested by a company’s, Retained EarningsRetained EarningsThe Retained Earnings formula represents all accumulated net income netted by all dividends paid to shareholders. Retained Earnings are part

The accounting equation shows the relationship between these items.

Rearranging the Accounting Equation

The accounting equation can also be rearranged into the following form:

Shareholder’s Equity = Assets – Liabilities

In this form, it is easier to highlight the relationship between shareholder’s equity and debt (liabilities). As you can see, shareholder’s equity is the remainder after liabilities have been subtracted from assets. This is because creditors – parties that lend money – have the first claim to a company’s assets.

For example, if a company becomes bankruptBankruptcyBankruptcy is the legal status of a human or a non-human entity (a firm or a government agency) that is unable to repay its outstanding debts, its assets are sold and these funds are used to settle debts first. Only after debts are settled are shareholders entitled to any of the company’s assets to attempt to recover their investments.

Regardless of how the accounting equation is represented, it is important to remember that the equation must always balance.

Examples of the Accounting Equation

For every transaction, both sides of this equation must have an equal net effect. Below are some examples of transactions and how they affect the accounting equation.

CFI’s accounting fundamentals course will help you better understand these examples!

1. Purchasing a Machine with Cash

Company XYZ wishes to purchase a $500 machine using only cash. This transaction would result in a debit to Equipment (+$500) and a credit to Cash (-$500). The net effect on the accounting equation would be as follows:

This transaction affects only the assets of the equation; therefore there is no corresponding effect in liabilities or shareholder’s equity on the right side of the equation.

2. Purchasing a Machine with Cash and Credit

Company XYZ wishes to purchase a $500 machine but it only has $250 of cash in its holdings. The company is allowed to purchase this machine with an initial payment of $250 but it owes the manufacturer the remaining amount. It would result in a debit to Equipment (+$500), a credit to Accounts Payable (+$250), and a credit to Cash (-$250). The net effect on the accounting equation would be as follows:

This transaction affects both sides of the accounting equation; both the left and right sides of the equation increase by +$250.

Additional Resources

Corporate Finance Institute has other resources that will help you expand your knowledge and keep your bookkeeping in check. Take a look at the links below:

- Accounting Fundamentals

- Reading Financial Statements

- General LedgerGeneral LedgerIn accounting, a General Ledger (GL) is a record of all past transactions of a company, organized by accounts. General Ledger (GL) accounts

- T AccountT Accounts GuideIf you want a career in accounting, T Accounts may be your new best friend. The T Account is a visual representation of individual accounts

-

Accounting Conservatism: Definition, Examples & Importance

Accounting conservatism refers to financial reporting guidelines that require accountants to exercise a high degree of verification and utilize solutions that show the least aggressive numbers when fa

-

Nifty 50: History, Significance & Key Stocks - A Comprehensive Guide

The Nifty 50 refers to the fifty most popular large-cap stocks that traded at high valuations in the 1960s and 1970s. They included household names such as Xerox (XRX), IBM, Polaroid and Coca-Cola (

Accounting

- Accounting Explained: Understanding Financial Records & Reporting

- Understanding the Accounting Cycle: A Comprehensive Guide

- Understanding Accounting Income: A Key Financial Metric

- Understanding Accounting Methods: Cash vs. Accrual

- Accrual Accounting Principle: Definition & Explanation

- Understanding the Expanded Accounting Equation: A Comprehensive Guide

- Understanding the GAAP Hierarchy: A Comprehensive Guide

- Hedge Accounting Explained: A Comprehensive Guide

- Understanding the Philosophy of Accounting: Principles & Concepts

-

Dow 30 Explained: Understanding the Dow Jones Industrial Average

Dow 30 Explained: Understanding the Dow Jones Industrial AverageThe Dow 30, or Dow Jones Industrial Average, is a stock index that tracks the performance of the 30 biggest companies listed on the stock indices in the United States. Despite being used by analysts t...

-

![Rule of 72: Calculate Investment Doubling Time | [Your Brand Name]](https://www.etffin.com/article/uploadfiles/202110/2021100815281678_S.png) Rule of 72: Calculate Investment Doubling Time | [Your Brand Name]

Rule of 72: Calculate Investment Doubling Time | [Your Brand Name]In finance, the Rule of 72 is a formula that estimates the amount of time it takes for an investment to double in value, earning a fixed annual rate of returnRate of ReturnThe Rate of Return (ROR) is ...