Understanding the Expanded Accounting Equation: A Comprehensive Guide

The expanded accounting equation breaks down shareholder’s equity (otherwise known as owners’ equity) into more depth than the fundamental accounting equation. It allows analysts and accountants to see the components of shareholder’s equityStockholders EquityStockholders Equity (also known as Shareholders Equity) is an account on a company's balance sheet that consists of share capital plus and how it impacts the company. It breaks down net income and the transactions related to the owners (dividends, etc.).

Fundamental Accounting Equation

The more simplified version of the accounting equation is called the “fundamental accounting equation” or the “balance sheet equation.” It is equal to:

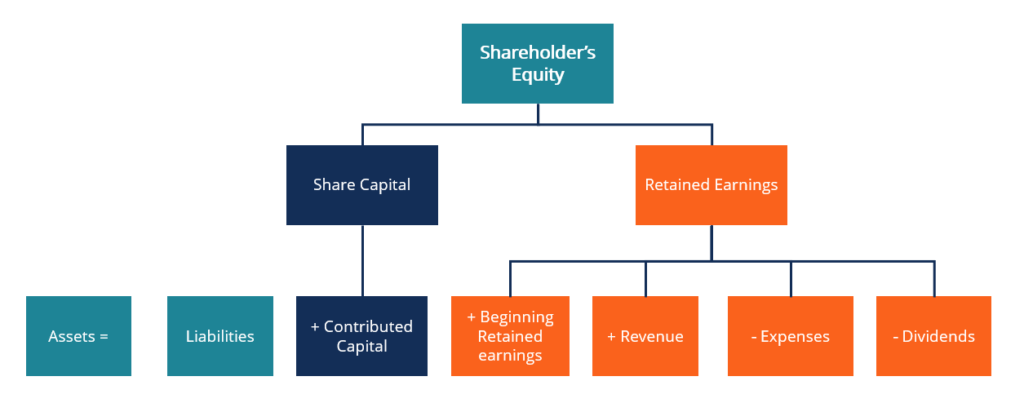

Assets = Liabilities + Shareholder’s Equity

The fundamental accounting equation is debatably the foundation of all accounting, specifically the double-entry accounting system and the balance sheet. Double-entry accounting is the concept that every transaction will affect both sides of the accounting equation equally, and the equation will stay balanced at all times. Double-entry accounting is used for journal entries of any kind.

- Assets are resources a company has that hold a future benefit. Assets are found by combining all current assetsCurrent AssetsCurrent assets are all assets that a company expects to convert to cash within one year. They are commonly used to measure the liquidity of a with all non-current assets. Common examples of assets include cash, accounts receivable, machinery, land, and prepaid expenses.

- Liabilities are obligations of a company to pay money owed to a lender as a result of a previous transaction. The liability total can be found by adding all current liabilities with all long-term debts and other obligations. Common examples of liabilities include accounts payable, taxes owed, and bank loans.

- Shareholder’s equity is the company owners’ residual claims on assets after deducting all liabilities deducted. The expanded accounting equation will further break them down.

Understanding the Expanded Accounting Equation

The expanded accounting equation is broken down to be:

Assets = Liabilities + Share Capital + Retained Earnings

Assets = Liabilities + CC + BRE + R + E + D

Where:

- CC = Contributed Capital

- BRE = Beginning Retained Earnings

- R = Revenue

- E = (–) Expenses

- D = (–) Dividends

N.B.: Expenses and dividends will be negative numbers if applicable.

- Contributed capital comes from the capital provided by the original stockholders.

- Beginning retained earnings is the carryover retained earnings that were not distributed to stockholders during the previous period.

- Revenue comes from the sales and operations of the business.

- Expenses are the costs associated with running the operation.

- Dividends are the earnings that are distributed to stockholders of the company.

The expanded accounting equation can allow analysts to better look into the company’s break-down of shareholder’s equity. The revenues and expenses show the change in net income from period to period. Stockholder transactions can be seen through contributed capital and dividends. Although these numbers are basic, they are still useful for executives and analysts to get a general understanding of their business.

Rearranged Expanded Accounting Equation

The expanded accounting equation can be rearranged to suit better the needs of the individual using it. We can rearrange the equation to be:

Assets – Liabilities = Shareholder’s Equity

Assets – Liabilities = Share Capital + Retained Earnings

Assets – Liabilities = CC + BRE + R + E + D

Rearrangement in such a way can be useful when looking at bankruptcyBankruptcyBankruptcy is the legal status of a human or a non-human entity (a firm or a government agency) that is unable to repay its outstanding debts. The equation layout can help shareholders to see more easily how they will be compensated.

Short and long-term debts, which fall under liabilities, will always be paid first. The remainder of the liquidated assets will be used to pay off parts of shareholder’s equity until no funds are remaining.

The expanded accounting equation can be rearranged in many ways to suit its use better. With that being said, no matter how the formula is laid out, it must always be balanced.

Examples

Journal Entry

As was previously stated, double-entry accounting supports the expanded accounting equation. Double-entry accounting is a fundamental concept that backs most modern-day accounting and bookkeeping tasks.

It specifies that all financial transactions will include a corresponding and opposite entry in two or more accounts, balancing the journal entry and the accounting equation. Transactions are recorded with one (or more) accounts being debited and one (or more) accounts being credited. Below are some examples of journal entries:

*Notice how in all cases, the equation stays balanced.

Explanation: New computers that cost $2,500 are purchased. $1,000 is paid upfront in cash and the rest is paid on account.

Dr. Computer (Asset) $2,500

Cr. Cash (Asset) $1,000

Cr. A/P (Liability) $1,500

2,500 – 1,000 = +1,500 + CC + BRE + R + E + D

Explanation: $1,000 is paid out of retained earnings to stockholders as dividends.

Dr. Retained Earnings $1,000

Cr. Dividends $1,000

Assets = Liabilities + CC + 1,000 + R + E + (–)1,000

Explanation: A supplies expense of $600 is paid on account

Dr. Supplies Expense $600

Cr. Accounts Payable $600

Assets = 6,000 + CC + BRE + R + E + (–)600 + D

Balance Sheet

The expanded accounting equation goes hand in hand with the balance sheet; hence, it is why the fundamental accounting equation is also called the balance sheet equation. Any changes to the expanded accounting equation will result in the same change within the balance sheet.

Additional Resources

CFI offers the Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below:

- Financial Accounting TheoryFinancial Accounting TheoryFinancial Accounting Theory explains the why behind accounting - the reasons why transactions are reported in certain ways. This guide will

- Projecting Balance Sheet Line ItemsProjecting Balance Sheet Line ItemsProjecting balance sheet line items involves analyzing working capital, PP&E, debt share capital and net income. This guide breaks down how to calculate

- Journal Entries GuideJournal Entries GuideJournal Entries are the building blocks of accounting, from reporting to auditing journal entries (which consist of Debits and Credits)

- Projecting Income Statement Line ItemsProjecting Income Statement Line ItemsWe discuss the different methods of projecting income statement line items. Projecting income statement line items begins with sales revenue, then cost

-

![Rule of 72: Calculate Investment Doubling Time | [Your Brand Name]](https://www.etffin.com/article/uploadfiles/202110/2021100815281678_S.png)

Rule of 72: Calculate Investment Doubling Time | [Your Brand Name]

In finance, the Rule of 72 is a formula that estimates the amount of time it takes for an investment to double in value, earning a fixed annual rate of returnRate of ReturnThe Rate of Return (ROR) is

-

Accounting Conservatism: Definition, Examples & Importance

Accounting conservatism refers to financial reporting guidelines that require accountants to exercise a high degree of verification and utilize solutions that show the least aggressive numbers when fa

Accounting

- Accounting Explained: Understanding Financial Records & Reporting

- Understanding the Accounting Cycle: A Comprehensive Guide

- Understanding the Accounting Equation: Assets = Liabilities + Equity

- Understanding Accounting Income: A Key Financial Metric

- Understanding Accounting Methods: Cash vs. Accrual

- Accrual Accounting Principle: Definition & Explanation

- FASB: Understanding Financial Accounting Standards & GAAP

- Understanding the GAAP Hierarchy: A Comprehensive Guide

- Understanding the Philosophy of Accounting: Principles & Concepts

-

Dow 30 Explained: Understanding the Dow Jones Industrial Average

Dow 30 Explained: Understanding the Dow Jones Industrial AverageThe Dow 30, or Dow Jones Industrial Average, is a stock index that tracks the performance of the 30 biggest companies listed on the stock indices in the United States. Despite being used by analysts t...

-

Mastering the Accounting Equation for Small Business Bookkeeping

Mastering the Accounting Equation for Small Business BookkeepingThe accounting equation is the basis of double-en...