Understanding the Accounting Reporting Cycle: A Comprehensive Guide

The reporting cycle involves the running, managing, updating, and reporting of a company’s accounts. The cycle usually runs concurrently with the planning and budgeting cycles. It ensures that the company is ready to begin the following period. A company’s planning/budgeting cycles and reporting cycle are usually independent of each other but can involve the same people in their preparation.

The planning cycle involves future estimations in spending and income cashflows while the reporting cycle gives the current standings of the company, with regards to assetsTypes of AssetsCommon types of assets include current, non-current, physical, intangible, operating, and non-operating. Correctly identifying and, revenue, and expenses, after a specified period of business time. Therefore, the planning cycle looks forward in terms of time, while the reporting cycle looks backward on business activity and the most recent standings.

Summary

- The reporting cycle is an entire sequence of a reporting period that guides the preparation of financial statements.

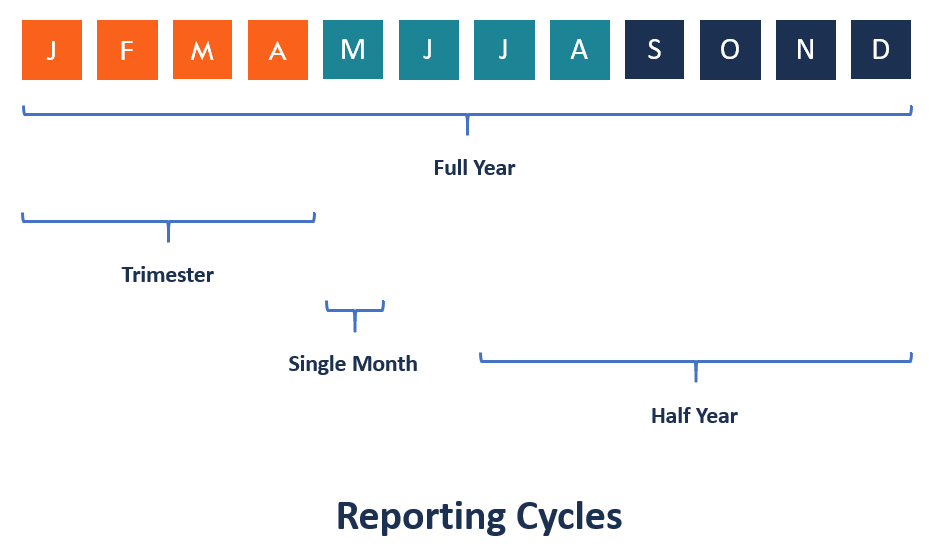

- The reporting cycle period can be a year, fiscal quarter, or a specified period.

- The cycle begins with the initial transaction entries in the journal and ends with the published financial statements of the company and the closing of all the temporary accounts.

Reporting Cycle Regulations

Reporting of business performance, especially for public companiesPublic CompaniesPublic companies are entities that trade their stocks on the public exchange market. Investors can become shareholders in a public company by purchasing shares of the company's stock. The company is considered public since any interested investor can purchase shares of the company in the public exchange to become equity owners., is mandatory all over the world. The reporting cycle should, at most, be for a year or less. Such a regulation helps in transparency in the running of public companies. Investors own publicly held companies through the purchase of shares, and gain insight into their operations through the reading of the companies financial reports.. The financial reports, therefore, enable the investors to follow the company’s performance with ease.

Financial statements that companies are obliged to report on include the income statement, cash flow statement, statement of retained earnings, and statement of financial position. They are the basic statements that allow the public to understand the financial performance of the company during a given period.

Benefits of the Reporting Cycle

The reporting cycle of any company is important in providing vital information to its shareholders, directors, employees, competitors, and financial analysts. The financial statements published during the reporting cycle provide an overview of the performance of the company.

For example, the income statementIncome StatementThe Income Statement is one of a company's core financial statements that shows their profit and loss over a period of time. The profit or details the sales revenue for a specific period, expenses incurred by the company, interest incomes earned, and the net profit for the period. The statement of financial position, also known as the balance sheet, gives the net value of assets owned by the company at the end of a financial period.

The net value of all assets factors in their depreciation and their current value in the market. The statement of retained earnings indicates how the company’s directors allocated the net profits for the period to the retained earnings account and the dividend account for distribution to stockholders.

An Account in the Reporting Cycle

The account is the basic building block of a reporting cycle, and it takes a record of each transaction performed by the company. A transaction, on the other hand, is an activity undertaken by the business to serve a client. Transactions cause a change in the financial earnings, either as an income for the company or an expense where it spends money.

Accounts fall in categories, such as revenue, liability, equity, assets, and expenses. An account must be unique from other accounts in the company. Therefore, every account comes with a distinct account number and name. The account’s balance is always either a debit or credit balance.

A Transaction in the Reporting Cycle

A transaction can be either financial or non-financial. Transactions can be recorded either as accrual or cash transactions. The number and state of transactions seldom depend on the size of the company and the traffic of activities therein. Examples of transactions include expenses, paying dividends, assets acquisition, writing off bad debt, a sale, revenues earned, etc.

Transactions are entered into the journal chronologically. The order of occurrence of transactions dictates their order. It allows for easy follow-up in case one requires a better explanation of the contents of the financial report.

Closing the Reporting Cycle

The reporting cycle is closed by preparing and publishing financial statements. The reported statements should be cross-checked for errors through auditing to make final adjustments before they are released to the public. The financial statements are discussed with the directors before publishing. The final report should undergo an auditor’s scrutiny before being released to the public.

An auditor should read in between the lines to highlight any inconsistencies and outright errors in the report. The auditor checks whether the report conforms to the laid out accounting principles and whether it portrays a true financial state of the firm. If the auditor is satisfied with the report and gives an unqualified opinion, the report is released to investors, shareholders, and the general public through the mainstream media or the company’s own channels of communication.

Related Readings

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today!®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to transform anyone into a world-class financial analyst.

In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful:

- Earnings GuidanceEarnings GuidanceAn earnings guidance is the information provided by the management of a publicly traded company regarding its expected future results, including estimates

- Projecting Balance Sheet Line ItemsProjecting Balance Sheet Line ItemsProjecting balance sheet line items involves analyzing working capital, PP&E, debt share capital and net income. This guide breaks down how to calculate

- Three Financial StatementsThree Financial StatementsThe three financial statements are the income statement, the balance sheet, and the statement of cash flows. These three core statements are

- Types of Due DiligenceTypes of Due DiligenceOne of the most important and lengthy processes in an M&A deal is Due Diligence. The process of due diligence is something which the buyer conducts to confirm the accuracy of the seller's claims. A potential M&A deal involves several types of due diligence.

-

Understanding the Acquisition and Payment Cycle: A Comprehensive Guide

The Acquisition and Payment Cycle (also referred to as the PPP Cycle for Purchases, Payables, and Payments) consists mainly of two classes of transactions. The first class is the acquisition class. Th

-

McKinsey 7S Model: Understanding Organizational Effectiveness

The McKinsey 7S Model refers to a tool that analyzes a company’s “organizational design.” The goal of the model is to depict how effectiveness can be achieved in an organization thro

Accounting

- Acid-Test Ratio: Understanding Your Company's Short-Term Liquidity

- Understanding the Earnings Multiplier (P/E Ratio): A Comprehensive Guide

- Understanding the IPO Process: A Comprehensive Guide

- Modigliani-Miller Theorem: Understanding Capital Structure & Firm Value

- Skin in the Game: Understanding Risk & Accountability

- Clientele Effect: How Investor Preferences Impact Stock Prices

- Understanding the Accounting Cycle: A Comprehensive Guide

- Cash Conversion Cycle (CCC): Definition & Analysis

- Understanding the Matching Principle in Accounting

-

Cost Method Explained: Accounting & Investment Strategies

Cost Method Explained: Accounting & Investment StrategiesThe cost method of accounting is used for recording certain investmentsInvestment MethodsThis guide and overview of investment methods outlines they main ways investors try to make money and manage ri...

-

5C Analysis: A Comprehensive Framework for Business Strategy

5C Analysis is a marketing framework to analyze the environment in which a company operates. It can provide insight into the key drivers of success, as well as the risk exposureSystemic RiskSystemic r...