Objectives of Income Tax Accounting: A Comprehensive Overview

Tax accounting is one of the largest subsets or specializations within the field of accountingAccountingPublic accounting firms consist of accountants whose job is serving business, individuals, governments & nonprofit by preparing financial statements, taxes. In terms of corporate finance, there are several objectives when it comes to accounting for income taxes and optimizing a company’s valuation.

Main Objectives

The three main objectives in accounting for income taxes are:

1. Optimizing After-Tax Profits

First, a company’s income tax accounting should be in line with its operating strategy. That is, to maximize profits a company must understand how it incurs tax liabilities and adjust its strategies accordingly.

2. Funding Considerations

Secondly, income tax accounting can enable a company to maintain financial flexibility. There are different effects of funding the company’s operations with debt and/or equity, and a company’s capital structure can influence its tax liability. Knowing these effects will allow the company to plan accordingly and transitively maintain its financial flexibility by keeping its options open.

3. Timing of Payments

Finally, accounting for taxes enables the company to manage cash flow and minimize cash taxes paid. It is beneficial to postpone payment of taxes into the future, as opposed to paying taxes today. A company will want to take tax deductions sooner rather than later to maximize the time value of their money.

What Should an Analyst Understand about Tax?

Tax is an intricate field to navigate and often confuses even the most skilled financial analysts. This is keeping in mind that there are numerous tax codes and policies in any given jurisdiction, and numerous jurisdictions with different tax policies to exacerbate the effect.

Working knowledge of tax accounting, thus, becomes a great skill to have as a financial analystFP&A AnalystBecome an FP&A Analyst at a corporation. We outline the salary, skills, personality, and training you need for FP&A jobs and a successful finance career. FP&A analysts, managers, and directors are responsible for providing executives with the analysis and information they need. When speaking of just the bare necessities, an analyst should at least have a solid conceptual understanding of the following:

- Exceptions to certain policies

- An understanding of common issues that arise with taxes

- An understanding of the interplay of deferred taxesDeferred Tax Liability/AssetA deferred tax liability or asset is created when there are temporary differences between book tax and actual income tax., current taxes, and effective tax rates

- An understanding of the impact of taxes on cash flow

- How to apply this understanding in financial modeling

Income Tax vs. Accounting Tax

Tax as recorded in a company’s financial statement rarely ever matches the taxes filed in their tax returns. It is because each item (company financials and tax return) has different purposes, users, and accounting treatment. The company’s financials are intended for investors and lenders, and – as such – are made with application and dependability in mind. In contrast, the tax return is intended for the government or corresponding tax body and is made with the purpose of adhering to public tax policy.

The financial statements report a tax expense, but the true tax payable comes from the tax return. The dichotomy in reporting these two items creates differencesPermanent/Temporary Differences in Tax AccountingPermanent differences are created when there's a discrepancy between pre-tax book income and taxable income under tax returns and tax that need to be reconciled and accounted for. These differences are either permanent differences, which never reverse, or temporary differences, which are timing differences that will reverse over time.

Read More

This has been a guide to accounting for income taxes and alignment with corporate strategy. To learn more about taxation, check out the following CFI resources:

- Tax-Free ReorganizationTax-Free ReorganizationTo qualify as a tax-free reorganization, a transaction must meet certain requirements, which vary greatly depending on the form of the transaction.

- Section 368Section 368Section 368(A)(1) outlines a format for US tax treatment of corporate reorganizations, as described in the Internal Revenue Code of 1986.

- Balance SheetBalance SheetThe balance sheet is one of the three fundamental financial statements. The financial statements are key to both financial modeling and accounting.

- Debt ScheduleDebt ScheduleA debt schedule lays out all of the debt a business has in a schedule based on its maturity and interest rate. In financial modeling, interest expense flows

- Income Statement TemplateIncome StatementThe Income Statement is one of a company's core financial statements that shows their profit and loss over a period of time. The profit or

-

Understanding Accounting Policies: A Guide for Businesses

Accounting policies are rules and guidelines that are selected by a company for use in preparing and presenting its financial statements. Accounting policies are important, as they set a framework, wh

-

Understanding Accounting Ratios: A Comprehensive Guide

Accounting ratios cover a wide array of ratios that are used by accountants and act as different indicators that measure profitability, liquidityLiquidityIn financial markets, liquidity refers to how

Accounting

- Essential Factors for Creating a Personal Budget

- Florida Low Income Guidelines & Assistance Programs - 2024

- Understanding Taxes on Pension Benefits: A Comprehensive Guide

- Understanding Accounting Income: A Key Financial Metric

- Understanding Earnings Before Tax (EBT): Definition & Importance

- Understanding Permanent vs. Temporary Tax Differences

- LLC Tax Benefits: Maximize Your Savings & Business Growth

- 5 Key Steps in Tax Planning for Businesses

- Capital Gains Tax vs. Ordinary Income Tax: Key Differences Explained

-

Accounting vs. Tax Depreciation: Key Differences Explained

Accounting vs. Tax Depreciation: Key Differences ExplainedBefore we discuss accounting depreciation vs tax depreciation, let us first talk about depreciation itself. Essentially, depreciation is a method of allocating the cost of a tangible asset over severa...

-

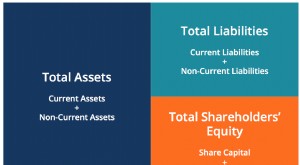

Understanding the Accounting Equation: Assets = Liabilities + Equity

Understanding the Accounting Equation: Assets = Liabilities + EquityThe accounting equation is a basic principle of accounting and a fundamental element of the balance sheetBalance SheetThe balance sheet is one of the three fundamental financial statements. The financ...