Understanding Audited Financial Statements: A Comprehensive Guide

Public companies are obligated by law to ensure that their financial statementsThree Financial StatementsThe three financial statements are the income statement, the balance sheet, and the statement of cash flows. These three core statements are are audited by a registered CPA. The purpose of the independent audit is to provide assurance that the management has presented financial statements that are free from material error.

Additionally, hiring an independent and qualified CPA provides reassurance to banks, suppliers, and potential investors that the business is financially sound and creditworthy. Audited financial statements are needed to provide information to decision-makers.

During a financial audit, a CPA confirms that the financial statements do not contain material errors. In case there are substantial errors, the CPA recommends corrective measures that comply with the Generally Accepted Accounting Principles (GAAP)GAAPGAAP, Generally Accepted Accounting Principles, is a recognized set of rules and procedures that govern corporate accounting and financial and International Financial Reporting Standards (IFRS).

The following are the main types of audited financial statements:

1. Income Statement

An income statementIncome Statement TemplateFree Income Statement template to download. Create your own statement of profit and loss with annual and monthly templates in the Excel file shows the performance of the company during a fiscal year. The statement reports the revenueSales RevenueSales revenue is the income received by a company from its sales of goods or the provision of services. In accounting, the terms "sales" and earned and expenses incurred during the period. On the last line, the report reveals the net profitNet Profit MarginNet Profit Margin (also known as "Profit Margin" or "Net Profit Margin Ratio") is a financial ratio used to calculate the percentage of profit a company produces from its total revenue. It measures the amount of net profit a company obtains per dollar of revenue gained. or loss for the period. (This fact is actually the origin of the term, “bottom line”, as the bottom line on an income statement shows a company’s profit/loss for the year.)

The earnings per share (EPS) figure may be included when the financial statements are issued by a publicly-traded company.

The auditor verifies the accuracy of transactions by cross-checking the cash book and individual books of accounts.

2. Balance Sheet

The balance sheetBalance SheetThe balance sheet is one of the three fundamental financial statements. The financial statements are key to both financial modeling and accounting. reports the financial position of the company at the end of the fiscal year (or at any other point in time a balance sheet is prepared; for example, companies are usually required to submit a balance sheet when applying for a loan). It reveals the value of assets, liabilities, and equity of a company.

The items in the assets and liabilities columns are presented in order of liquidity, with the most liquid items reported first. The auditor may verify the existence of assets and liabilities, and the accuracy of the figures presented.

3. Cash Flow Statement

The cash flow statementCash Flow StatementA cash flow Statement contains information on how much cash a company generated and used during a given period. may also be included in the audited financial statements. The cash flow statement reveals the cash inflows and outflows during the fiscal year. It provides an insight into the company’s ability to meet its short-term obligations and continue operating in the foreseeable future. The auditor may verify the entries in the cash flow statement against the bank statement and also check the accuracy of the footnotes.

Audit Opinion Letter

An auditor issues an audit opinion letter after completing the audit process, and it is included with the audited financial statements. In this letter, the auditor reveals the financial statements reviewed and the audit method used. If there were no material errors in the financial statements, then the auditor will give an audit opinion that the financial statements represent a true and fair view of the company’s performance and position.

Learn more about audit standards from AICPA.

Contents of Audit Opinion Letter

Below is an example of an audition opinion letter, to be used for education purposes only.

Dear Board of Directors

XYZ Company

We, the auditors, have audited the income statement, balance sheet, and cash flow statement of XYZ Company as of December 31, 2018.

We completed our audit according to the auditing standards set out by Generally Accepted Accounting Principles (GAAP) in the United States. Based on this audit, we have obtained reasonable assurance that the above noted financial statements are free of material misstatement.

As part of our audit, we examined and tested evidence supporting the figures contained in the financial statements. We also assessed the accounting principles and estimates used by the company in preparing their financial statements. This audit formed the basis of our opinion, stated below.

In our opinion, the financial statements of XYZ Company are represented in accordance with Generally Accepted Accounting Principles (GAAP) in the United States.

[Signature]

Auditor’s name

Additional Resources

We hope this has been a helpful guide on audited financial statements. CFI is the official global provider of the Financial Modeling and Valuation Analyst (FMVA)Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today!®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! designation.

If you want to learn more, CFI has all the resources you need to advance your career:

- IFRS vs. US GAAPIFRS vs. US GAAPThe IFRS vs US GAAP refers to two accounting standards and principles adhered to by countries in the world in relation to financial reporting

- SEC MD&AWhat is MD&A?The Management Discussions and Analysis (MD&A) is a section of the annual report or SEC filing 10-K that provides an overview of how the company performed in the prior period, its current financial condition, and management's future projections.

- SEC 10-K10-KForm 10-K is a detailed annual report that is required to be submitted to the U.S. Securities and Exchange Commission (SEC). The filing provides a comprehensive summary of a company’s performance for the year. It is more detailed than the annual report that is sent to shareholders

- Types of SEC FilingsTypes of SEC FilingsThe US SEC makes it mandatory for publicly traded companies to submit different types of SEC filings, forms include 10-K, 10-Q, S-1, S-4, see examples. If you are a serious investor or finance professional, knowing and being able to interpret the various types of SEC filings will help you in making informed investment decisions.

-

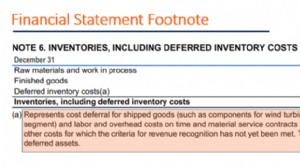

Understanding Financial Statement Footnotes: A Comprehensive Guide

Financial statement footnotes are used as additional information to individuals reading a financial statement. Otherwise known as explanatory notes or notes to the financial statements, the footnotes

-

Understanding Review Engagements: Limited Assurance on Financial Statements

A review engagement is also known as a limited assurance or negative engagement. Auditors conduct a review engagement after an accountant’s completed an audit of a company’s financial stat

Accounting

- Understanding Joint Financial Statements: A Comprehensive Guide

- Understanding Financial Statement Analysis: Income Statement, Balance Sheet & Cash Flow

- Understanding Financial Statements: A Comprehensive Guide

- Personal Financial Statements: A Guide for Individuals

- Financial Statement Manipulation: Definition & Examples

- Understanding Financial Statement Notes: A Comprehensive Guide

- Understanding Financial Statements: A Comprehensive Guide

- Understanding the Interrelationship of Financial Statements

- Understanding Financial Statements: A Beginner's Guide

-

Understanding Annual Reports: Key Components & Financial Insights

Understanding Annual Reports: Key Components & Financial InsightsYou can find most annual reports on the company website. The annual report is a financial document published by most private and public companies to summarize the major transactions of the ye...

-

![Compilation Engagement: Definition & Benefits | [Your Company Name]](https://www.etffin.com/article/uploadfiles/202110/2021100815133559_S.jpeg) Compilation Engagement: Definition & Benefits | [Your Company Name]

Compilation Engagement: Definition & Benefits | [Your Company Name]A compilation engagement is a service provided by an outside accountant to assist the management in the presentation of financial data in the form of financial statements. The accountant should posses...