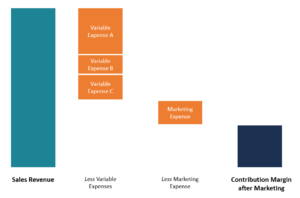

Understanding Contribution Margin After Marketing (CMAM): Definition & Calculation

Contribution margin after marketing (CMAM) refers to the amount of money generated for each unit sold after deducting the variable costsVariable CostsVariable costs are expenses that vary in proportion to the volume of goods or services that a business produces. In other words, they are costs that vary and marketing expenses incurred by a company. Contribution margin after marketing is similar to contribution margin, but the company must account for the marketing costs incurred when promoting the product to potential buyers with information about the company’s products. CMAM tells you if the net sales are enough to cover the total variable costs and how much of the net sales is left to cover fixed expenses.

The variable cost component is comprised of expenses that fluctuate with changes in production levels. Examples of variable costs include raw materials, direct labor, inventoryInventoryInventory is a current asset account found on the balance sheet, consisting of all raw materials, work-in-progress, and finished goods that a, sales commission, and shipping costsFreight ExpenseFreight expense refers to the price that is charged by a carrier for sending out cargo from the source location to the destination location. The expense is paid by the person who wants the goods transported from one location to another. The amount of freight expense charged depends on the mode of transportation. Fixed costs, on the other hand, are costs that remain fixed even when there are changes in the production levels. Examples of fixed costs include rent, equipment lease, management salaries, and advertising.

Marketing Expense in Contribution Margin: Is it Fixed or Variable?

Marketing expense is categorized as a fixed cost since companies allocate money that they plan to spend over a particular period and will aim to spend the monthly or annual marketing budget. At the same time, there are some elements of marketing expense can be considered variable. For example, sales commissionCommissionCommission refers to the compensation paid to an employee after completing a task, which is, often, selling a certain number of products or services is directly correlated to the volume of sales during a specific period.

Depending on the industry, the fixed market expense may see seasonal variations where a company may allocate more funds to the marketing department to take advantage of a revenue surge or increased demand for specific products.

How to Calculate Contribution Margin After Marketing

The formula for calculating the contribution margin after marketing is as follows:

CMAM = Sales Revenue – Variable Costs – Marketing Expense

The contribution margin can also be calculated per unit in order to understand how much one unit of a product contributes to the overall company’s profits. The contribution margin per unit is calculated as follows:

CMAM per Unit = Sales Revenue per Unit – Variable Expenses per Unit – Marketing Expense per Unit

The difference between the sales revenue and the variable cost (and marketing expense) is the CMAM, and whatever is left is the combination of fixed costs and profit. To get the net profit/loss, we use the following formula:

Net Operating Profit = CMAM – Fixed Costs

When a company or department is profitable, it will post a profit after deducting variable costs, marketing expenses, and fixed costs. If the resulting value is negative, it means that the company made a loss and did not have enough money to cover its expenses.

Contribution Margin After Marketing Example

ABC Limited manufactures energy-saving bulbs. The variable costs of manufacturing one bulb include $1.70 worth of raw materials, $1.50 direct labor cost, $0.50 electricity, and $0.30 shipping costs. The company also incurs $3,000 in equipment lease, $4,500 in factory rent, $20,000 in management salaries, and $7,000 in marketing expenses. The selling price per unit is $7.50, and the company sold 20,000 bulbs in the previous year.

To get the contribution margin after marketing, we use the following formula:

Contribution Margin After Marketing = Sales Revenue – Variable Costs – Marketing Expense

Where:

Sales revenue = $7.50 x 20,000 = $150,000

Variable Costs = ($1.70 + $1.50 + $0.50 + $0.30) x 20,000

= $4 x 20,000 = $80,000

The contribution margin after marketing is obtained as follows:

= $150,000 – $80,000 – $7,000 = $63,000

To get the net operating profit or loss, we deduct fixed costs from the contribution margin after marketing, as shown below:

= $63,000 – ($3,000 + $4,500 + $20,000)

= $63,000 – $27,500 = $35,500

This means that ABC Limited posted a net operating profit of $35,500 in the previous financial year.

How CMAM is Used

The contribution margin after marketing is a useful metric for decision making in a company. The following are the main uses of the CMAM metric:

Management

The management of a company uses CMAM as a decision-making tool when deciding what product to continue producing and what product to discontinue. For example, using the previous example, assume that the bulb-manufacturing machine produces three different types of bulbs, and the company’s management must make a decision on two types of bulbs to continue manufacturing and one type of bulbs to discontinue.

The company can use the contribution margin per unit of each type of bulb to gauge which types of bulbs offer the possibility of earning the highest profits. The management may decide to continue producing the top two products and discontinue the third less profitable type of bulb. They can also use the outcome obtained to make decisions on how to allocate resources to the two remaining types of bulbs.

Investors

Investors may use the CMAM of the high-performing products of different potential companies to decide which companies to invest in. If one company produces a top product that consistently maintains a high CMAM compared to other competitor’s products, investors may use that information to guide their investment decisions.

Companies with products that provide a low or negative CMAM point to a non-viable product that should be discontinued or improved in order to compete favorably with other competitor’s products.

Additional Resources

CFI offers the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below:

- 5 P’s of Marketing5 P's of MarketingThe 5 P's of Marketing – Product, Price, Promotion, Place, and People – are key marketing elements used to position a business strategically. The 5 P's of

- Analysis of Financial StatementsAnalysis of Financial StatementsHow to perform Analysis of Financial Statements. This guide will teach you to perform financial statement analysis of the income statement,

- Fixed and Variable CostsFixed and Variable CostsCost is something that can be classified in several ways depending on its nature. One of the most popular methods is classification according

- Operating Profit MarginOperating Profit MarginOperating Profit Margin is a profitability or performance ratio that reflects the percentage of profit a company produces from its operations, prior to subtracting taxes and interest charges. It is calculated by dividing the operating profit by total revenue and expressing as a percentage.

-

EBITDA Margin: Definition, Calculation & Importance

EBITDA margin is a profitability ratio that measures how much in earnings a company is generating before interest, taxes, depreciation, and amortization, as a percentage of revenue. EBITDA Margin = EB

-

Margin of Safety: Definition, Calculation & Importance

The margin of safety is the difference between the amount of expected profitability and the break-even point. The margin of safety formula is equal to current sales minus the breakeven point, divided

Accounting

- Absorption Costing: A Comprehensive Guide for Businesses

- Capitalized Costs Explained: Definition & Examples

- Understanding Contribution Margin: A Key Profit Metric

- Cost Allocation: Definition, Methods & Importance

- Cost Drivers: Understanding What Impacts Your Business Expenses

- Direct Costs Explained: Definition, Examples & vs. Indirect Costs

- Understanding Implicit Costs: A Comprehensive Guide

- Understanding Markup: Definition, Calculation & Importance

- Profit Margin Explained: Types & How to Calculate

-

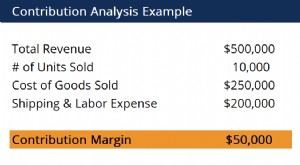

Contribution Analysis: Understanding Profitability & Cost Management

Contribution Analysis: Understanding Profitability & Cost ManagementContribution analysis is used in estimating how direct and variable costs of a product affect the net income of a company. It addresses the issue of identifying simple or overhead costs related to sev...

-

Contribution Margin: Definition, Calculation & Importance

Contribution Margin: Definition, Calculation & ImportanceWhat Is the Contribution Margin? The contribution margin can be stated on a gross or per-unit basis. It represents the incremental money generated for each product/unit sold after deducting the...