Understanding Highest-In, First-Out (HIFO) Inventory Valuation

Highest-In First-Out (HIFO) is a type of stock distribution and valuation method. The HIFO method follows the concept that stock or inventory with the greatest purchasing costs is first to be sold, used, or removed from the stock or inventory count. The use of HIFO is not recognized by GAAP (Generally Accepted Accounting Principles)GAAPGAAP, Generally Accepted Accounting Principles, is a recognized set of rules and procedures that govern corporate accounting and financial and is hardly used in accounting.

Following the HIFO method, at the end of an accounting period, the inventory will be recorded at the lowest possible value, and costs of goods sold (COGS)Cost of Goods Sold (COGS)Cost of Goods Sold (COGS) measures the “direct cost” incurred in the production of any goods or services. It includes material cost, direct will be the highest possible value.

Highest-in First-out is typically used by corporations looking to minimize their taxable earnings for a particular accounting period. HIFO allows for the costliest inventory to be sold first, regardless of when it was purchased, thereby driving up the value of the cost of goods sold, and lowering taxable earnings.

Also, HIFO will record high inventory turnover because the closing or ending inventory is valued at its lowest amount.

Summary

- Highest In First Out (HIFO) follows the concept that stock or inventory with the greatest purchasing costs is first to be sold, used, or removed from the stock or inventory count.

- The use of HIFO is not recognized by GAAP (Generally Accepted Accounting Principles) and therefore is rarely used in accounting.

- Apart from HIFO, there are seven (7) other methods of inventory valuation. They include first-in-first-out (FIFO), last-in-first-out (LIFO), base stock method, inflated price method, standard price method, market or replacement price method, and the average cost method.

Understanding Stock and Inventory Valuation

Inventory valuation is the costing methodology used to determine the value of unsold stock at the end of a period. Apart from HIFO, there are seven other methods of inventory valuation. They include:

- First-in First-out (FIFO) First-In First-Out (FIFO)The First-In First-Out (FIFO) method of inventory valuation accounting is based on the practice of having the sale or usage of goods followmethod

- Last-in First-out (LIFO) method

- Base stock method

- Inflated price method

- Standard price method

- Market or replacement price method

- Average cost method

An Overview of FIFO and LIFO

First-In First-Out (FIFO)

FIFO is a stock or inventory valuation and control method used to determine cash flows concerning the computation of COGS. The FIFO method follows the assumption that the oldest stock items in a company’s inventory are sold first. That means that the inventory purchased first before other additional purchases occurred is sold first.

The costs spent on the oldest inventory used in the FIFO computation (i.e., COGS). An example of the FIFO method for determining COGS is explained below:

Company XYZ sold 1,000 units of a product. There were 750 units originally purchased by Company XYZ at $15.00 and 250 units purchased at $25.00. The company cannot assign the original purchase cost of $15.00 to each unit sold. The cost can only be assigned to the 750 units sold. The remaining inventory of 250 units must be allocated at a higher purchase price – i.e., $25.00.

It is important to know that the items must’ve been sold to form part of the COGS computation, as it cannot be applied to unsold inventory. The FIFO method is widely used and preferred over LIFO.

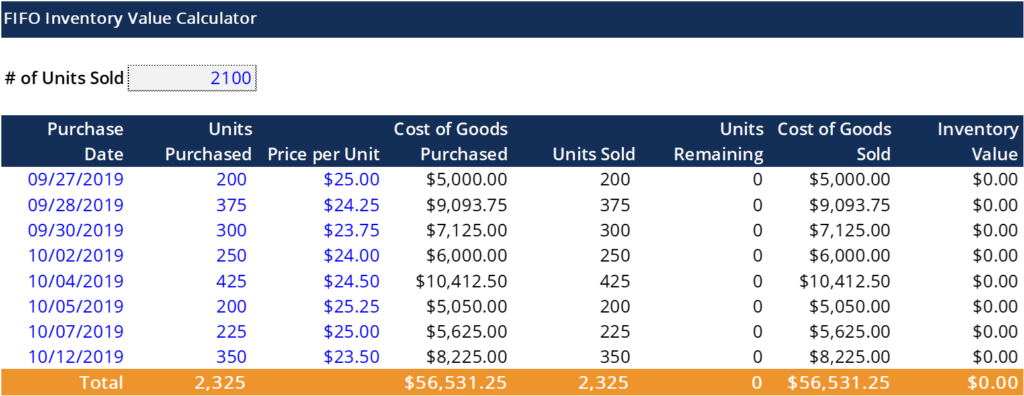

Below is an example of a FIFO Excel computation:

Last-In First-Out (LIFO)

Referencing an article by the CFI, LIFO is “an inventory valuation method based on the assumption that assets produced or acquired last are the first to be expensed. In other words, under the Last-in First-out method, the latest purchased or produced goods are removed and expensed first. Therefore, the old inventory costs remain on the balance sheet while the newest inventory costs are expensed first.”

Although the IFRS (International Financial Reporting Standards)IFRS StandardsIFRS standards are International Financial Reporting Standards (IFRS) that consist of a set of accounting rules that determine how transactions and other accounting events are required to be reported in financial statements. They are designed to maintain credibility and transparency in the financial world only permits the use of the FIFO method, the Generally Accepted Accounting Principles allow for the use of both FIFO and LIFO methods (respectively). Hence, companies that fall under the GAAP reporting standards can choose between the two methods.

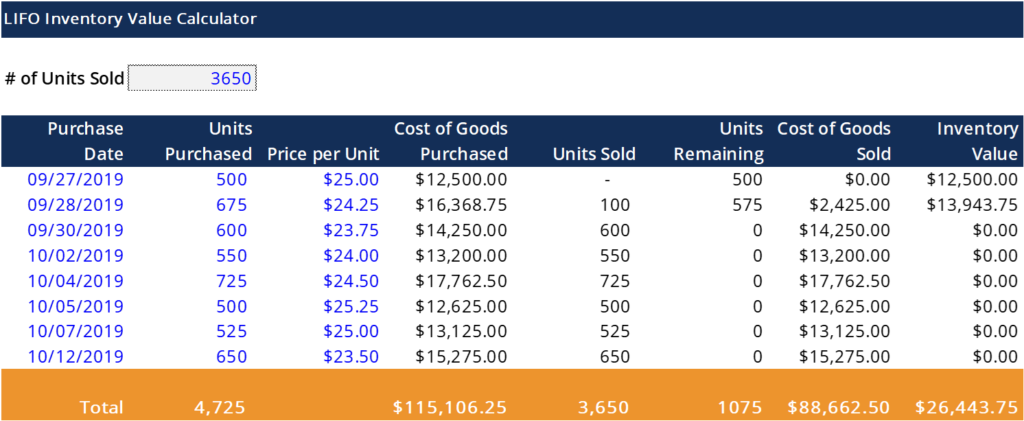

Below is an example of a LIFO Excel computation:

Learn More

CFI offers the Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below:

- Accounting CycleAccounting CycleThe accounting cycle is the holistic process of recording and processing all financial transactions of a company, from when the transaction

- IFRS vs. US GAAPIFRS vs. US GAAPThe IFRS vs US GAAP refers to two accounting standards and principles adhered to by countries in the world in relation to financial reporting

- LIFO vs. FIFOLIFO vs. FIFOAmid the ongoing LIFO vs. FIFO debate in accounting, deciding which method to use is not always easy. LIFO and FIFO are the two most common techniques used in valuing the cost of goods sold and inventory.

- Projecting Balance Sheet Line ItemsProjecting Balance Sheet Line ItemsProjecting balance sheet line items involves analyzing working capital, PP&E, debt share capital and net income. This guide breaks down how to calculate

-

Understanding Bad Debt Expense: Accounting & Methods

Bad debt expense is the way businesses account for a receivable account that will not be paid. Bad debt arises when a customer either cannot pay because of financial difficulties or chooses not to pay

-

Cost Recovery Method: Understanding Revenue Recognition

The cost recovery method of revenue recognitionRevenue RecognitionRevenue recognition is an accounting principle that outlines the specific conditions under which revenue is recognized. In theory, the

Accounting

- Understanding Accounting Methods: Cash vs. Accrual

- Inventory Auditing: A Comprehensive Guide for Businesses

- Understanding Average Inventory: Definition & Calculation

- FIFO Method Explained: Understanding First-In, First-Out Inventory Valuation

- Understanding Inventory: Definition & Importance in Financial Statements

- Inventory Shrinkage: Causes, Impact & Reconciliation

- LIFO Inventory Method: Understanding Last-In, First-Out

- Understanding the Next-In, First-Out (NIFO) Inventory Method

- Specific Identification Method: A Comprehensive Guide for Inventory Valuation

-

Understanding Inventory Age: A Key Metric for Business Efficiency

Understanding Inventory Age: A Key Metric for Business EfficiencyThe average age of inventory represents the average number of days that pass before a company sells its inventory balance. It is an important working capital efficiency metric that is also referred to...

-

Understanding Highest-In, First-Out (HIFO) Inventory Valuation

Understanding Highest-In, First-Out (HIFO) Inventory ValuationHighest-In First-Out (HIFO) is a type of stock distribution and valuation method. The HIFO method follows the concept that stock or inventory with the greatest purchasing costs is first to be sold, us...