IRC 382: Understanding Limitations on Net Operating Loss (NOL) Utilization

Under the Internal Revenue Code 382 (IRC 382), a C corporation is required to have a limit to offset historic losses. Essentially, a loss corporation is a firm that can use tax attributes like, for instance, NOL (Net Operating Loss). In contrast, “A Corporation” is a successful company that wants to acquire 100% of the stock of another company, “B Corporation”.

Basics of IRC 382

To understand the basics of section 382, we have the following details about B Corporation: It is a private company whose IP was funded with preferred financing and it has had net operating losses ever since it started. It is then considered a loss corporation. Once the acquisition is made, under Section 382, it limits the NOLs available to offset the taxable income of the company in the future.

There are two main components of this section – limitation and ownership change. Ownership change occurs when there is a shift in the owners or in the equity structure which is much more than 50%. Stock includes the following: convertible preferred stock, certain convertible debt instruments, common stock, and stock options/warrants.

Limitations of IRC 382

After the acquisition, the new company may deduct its losses in its taxable income following the Section 382 limitation. There is a formula used in calculating the base limitation amount. It is calculated as follows:

Fair Market Value of the Old Loss Corporation Stock x Federal Long Term Tax Exempt Rate= Base Limitation Amount

To get the most of its NOLS, the company would calculate to get the biggest base amount that they can.

However, when calculating the amount, keep in mind that the fair market value depends on potential adjustments as set forth in the said regulations. The Internal Revenue Service publishes monthly the federal long-term tax-exempt rate.

Offsetting Taxable Income

Companies that are operating at losses can get use these to offset taxable income. Although companies may benefit from such, it does not mean that there are no limitations. The limitations are guided by the Internal Revenue Code Section 382. Then again, even the calculation of the base amount has become much more complicated, especially when the Chief Counsel Advice has issued a case that could affect loss corporations.

Learn more by reading a helpful guide on Internal Revenue Code 382 from Cornell Law School.

Read more

Thank you for reading CFI’s explanation of Internal Revenue Code 382. To further advance your financial education, we offer the following free resources:

- Tax-free reorganizationTax-Free ReorganizationTo qualify as a tax-free reorganization, a transaction must meet certain requirements, which vary greatly depending on the form of the transaction.

- Type A reorganizationType A ReorganizationA Type A reorganization is a statutory merger or consolidation, which is classified under Section 368 of the IRC.

- Prepaid leasePrepaid LeaseA prepaid lease (or operating lease) is a contract to acquire the use of tangible assets, which include plant, equipment, and real estate.

- Inside Basis vs Outside BasisInside Basis vs Outside BasisInside Basis vs Outside Basis. The inside basis is the basis in the individual assets in the partnership. The outside basis is the basis of the partnership interest. Section 754 requires each partner to determine their adjusted basis in order to determine the exact tax liability of the partner..

-

Understanding Tax Basis: A Comprehensive Guide for Businesses

All businesses have assets. For very small businesses, those assets may be office equipment. For large companie

-

Understanding Adjusting Journal Entries: A Comprehensive Guide

An adjusting journal entry is usually made at the end of an accounting period to recognize an income or expense in the period that it is incurred. It is a result of accrual accountingAccrual Accountin

Accounting

- Accrued Revenue: Definition, Examples & Accounting Explained

- Ancillary Revenue: Definition, Examples & Maximization

- Understanding Deferred Revenue: A Comprehensive Guide

- Understanding Installment Sales: A Comprehensive Guide

- Internal Controls: Definition, Types & Importance for Financial Reporting

- IRC 382: Understanding Limitations on Net Operating Loss (NOL) Utilization

- Marginal Revenue: Definition, Calculation & Importance

- Understanding Revenue: A Comprehensive Guide for Businesses

- Revenue vs. Income: Understanding the Key Differences

-

LTM Revenue: Definition & Importance in Financial Analysis

LTM Revenue: Definition & Importance in Financial AnalysisLTM stands for “Last Twelve Months” and is similar in meaning to TTM, or “Trailing Twelve Months.” LTM Revenue is a popular term used in the world of finance as a measurement o...

-

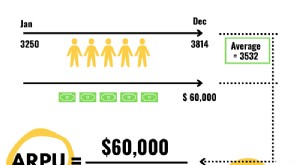

ARPU: Understanding and Calculating Average Revenue Per User

ARPU: Understanding and Calculating Average Revenue Per UserARPU is the amount of money a company earns from each of its users. The more you bill your customers, the more important understanding your average revenue per user becomes. For software businesses...