Understanding Deferred Revenue: A Comprehensive Guide

Deferred Revenue (also called Unearned Revenue) is generated when a company receives payment for goods and/or services that have not been delivered or completed. In accrual accountingAccrual AccountingIn financial accounting, accruals refer to the recording of revenues that a company has earned but has yet to receive payment for, and the, revenue is only recognized when it is earned. If a customer pays for goods/services in advance, the company does not record any revenue on its income statementIncome StatementThe Income Statement is one of a company's core financial statements that shows their profit and loss over a period of time. The profit or and instead records a liability on its balance sheetBalance SheetThe balance sheet is one of the three fundamental financial statements. The financial statements are key to both financial modeling and accounting..

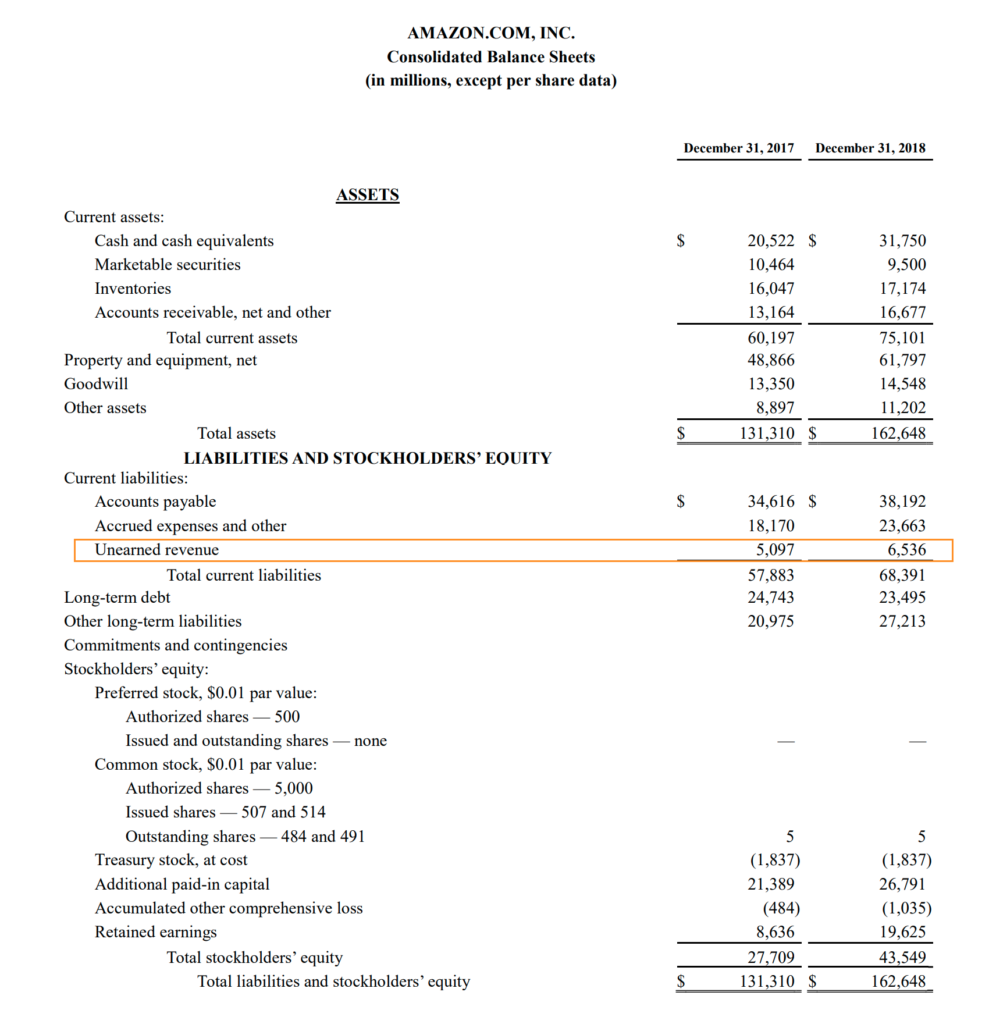

*Amazon’s 2018 Q4 Financial Statements

Example of Deferred Revenue

Let us look at a detailed example of the accounting entries a company makes when deferred revenue is created and then reversed or earned.

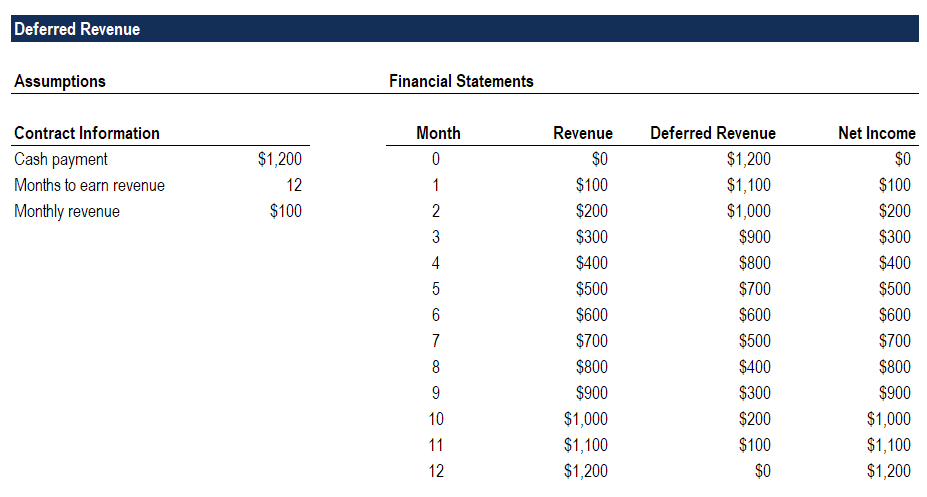

On August 1, Cloud Storage Co received a $1,200 payment for a one-year contract from a new client. Since the services are to be delivered equally over a year, the company must take the revenue in monthly amounts of $100.

On August 1, the company would record a revenue of $0 on the income statement. On the balance sheet, cash would increase by $1,200, and a liability called deferred revenue of $1,200 would be created.

On August 31, the company would record revenue of $100 on the income statement. On the balance sheet, cash would be unaffected, and the deferred revenue liability would be reduced by $100.

The pattern of recognizing $100 in revenue would repeat each month until the end of 12 months, when total revenue recognized over the period is $1,200, retained earnings are $1,200, and cash is $1,200. At that point, the deferred revenue from the transaction is now $0.

Download CFI’s Deferred Revenue template to analyze the numbers on your own.

Why Companies Record Deferred Revenue

The simple answer is that they are required to, due to the accounting principles of revenue recognition. In accrual accounting, they are considered liabilities, or a reverse prepaid expense, as the company owes either the cash paid or the goods/services ordered.

The timing of customers’ payments can be volatile and unpredictable, so it makes sense to ignore the timing of the cash payment and recognize revenue when it is earned.

Cash from Operating Activities

We’ve seen what happens to the income statement and balance sheet. Now, let’s look at the impact on the cash flow statement.

Referring to the example above, on August 1, when the company’s net income is $0, it would see an increase in current liabilities of $1,200, which would result in cash from operating activities of $1,200.

In all subsequent months, cash from operations would be $0 as each $100 increment in net income would be offset by a corresponding $100 decrease in current liabilities (the deferred revenue account).

Additional Resources

CFI offers the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

- Revenue Recognition PrincipleRevenue Recognition PrincipleThe revenue recognition principle dictates the process and timing by which revenue is recorded and recognized as an item in a company's

- Cash Flow StatementCash Flow StatementA cash flow Statement contains information on how much cash a company generated and used during a given period.

- Projecting Balance Sheet ItemsProjecting Balance Sheet Line ItemsProjecting balance sheet line items involves analyzing working capital, PP&E, debt share capital and net income. This guide breaks down how to calculate

- Analysis of Financial StatementsAnalysis of Financial StatementsHow to perform Analysis of Financial Statements. This guide will teach you to perform financial statement analysis of the income statement,

-

Financial Literacy: Understanding Key Concepts & Skills

Financial literacy is the cognitive understanding of financial components and skills such as budgeting, investing, borrowing, taxation, and personal financial management. The absence of such skil

-

Financial Mathematics: Applications & Quantitative Finance Explained

Financial mathematics describes the application of mathematics and mathematical modeling to solve financial problems. it is sometimes referred to as quantitative financeQuantitative FinanceQuantitativ

Accounting

- Understanding Financial Hardship: Causes, Impacts & Relief

- Accounting Explained: Understanding Financial Records & Reporting

- Ancillary Revenue: Definition, Examples & Maximization

- Understanding Financial Audits: A Comprehensive Guide

- Understanding Finance: A Comprehensive Overview

- Marginal Revenue: Definition, Calculation & Importance

- Understanding Revenue: A Comprehensive Guide for Businesses

- Revenue vs. Income: Understanding the Key Differences

- Unearned Revenue: Definition, Examples & Accounting Explained

-

Understanding Your Financial Health: A Comprehensive Guide

Understanding Your Financial Health: A Comprehensive GuideFinancial health is a basic measure of the soundness of an individual’s finances – essentially, it’s about what kind of financial shape you’re in overall. You may also view it ...

-

Financial Inclusion: Definition, Benefits & Impact

Financial Inclusion: Definition, Benefits & ImpactFinancial inclusion refers to the provision of equally available and affordable access to financial services for everyone, regardless of their level of income. It applies to providing services to both...