Operating Lease Explained: Benefits & How They Work

An operating lease is an agreement to use and operate an asset without the transfer of ownership. Common assetsTangible AssetsTangible assets are assets with a physical form and that hold value. Examples include property, plant, and equipment. Tangible assets are that are leased include real estate, automobiles, aircraft, or heavy equipment. By renting and not owning, operating leases enable companies to keep from recording an asset on their balance sheets by treating them as operating expenses.

Operating Lease vs. Capital Lease

An operating lease is different from a capital lease and must be treated differently for accounting purposes. Under an operating lease, the lessee enjoys no risk of ownership, but cannot deduct depreciation for tax purposes.

For a lease to qualify as a capital leaseCapital Lease vs Operating LeaseThe difference between a capital lease vs operating lease - A capital lease (or finance lease) is treated like an asset on a company’s, it must meet any of the following criteria as outlined by GAAP:

- The lease term is greater than or equal to 75% of the asset’s estimated useful life

- The present value of the lease payments is greater than or equal to 90% of the fair value of the asset

- Ownership of the asset may be transferred to the lessee at the end of the lease

- The lease contains a bargain purchase option for the lessee to buy the equipment below market value at the end of the lease

Additionally, under IFRS, there are a few more criteria that a lease can meet to qualify as a capital lease:

- The leased assets are specialized to the point that only the lessee can utilize these assets without major changes being made to them

Under a capital lease, the lessee is considered an owner and can claim depreciation and interest expense for tax purposes. The leased asset and lease obligation are shown on the balance sheet.

Capitalizing an Operating Lease

If a lease does not meet any of the above criteria, it is considered an operating lease. Assets acquired under operating leases do not need to be reported on the balance sheet. Likewise, operating leases do not need to be reported as a liability on the balance sheet, as they are not treated as debt. The firm does not record any depreciation for assets acquired under operating leases.

However, if a lease does meet any of the above criteria, it is instead considered a capital lease. A capital lease is treated differently from an operating lease. Instead of being treated as an operating expense, a capital lease is considered a financing expense. Therefore, we need to adjust the lease expense, depreciation expense, and interest expense numbers to account for this shift.

This will have an effect on operating income, which will always increase when these expenses are recategorized. However, it will not have any net effect on net income, as the change in numbers will balance out.

There are two methods to capitalize operating leases: the full adjustment method and the approximation method.

1. Full Adjustment Method

Step 1: Collect input data

Find the operating lease expenses, operating income, reported debt, cost of debt, and reported interest expenses.

Cost of debt can be found using the firm’s bond rating. If there is no existing bond rating, a “synthetic” bond rating can be calculated using the firm’s interest coverage ratio. Using the interest coverage ratio, compare it to this table created by New York University, Stern Business School professor Aswath Damodaran.

The remaining input data can be found in the company’s financial statements or the notes to the financial statements.

Step 2: Calculate the Present Value of Operating Lease Commitments

By capitalizing an operating lease, a financial analyst is essentially treating the lease as debt. Both the lease and the asset acquired under the lease will appear on the balance sheet. The firm must adjust depreciation expenses to account for the asset and interest expenses to account for the debt.

To do this, you must find the debt value of the operating leases. Find the present value of future operating lease expenses by discounting each year’s expense by the cost of debtCost of DebtThe cost of debt is the return that a company provides to its debtholders and creditors. Cost of debt is used in WACC calculations for valuation analysis.. The annuity method can be used if lease expenses are provided and remain constant over a timeframe of multiple years (e.g. years 6-10).

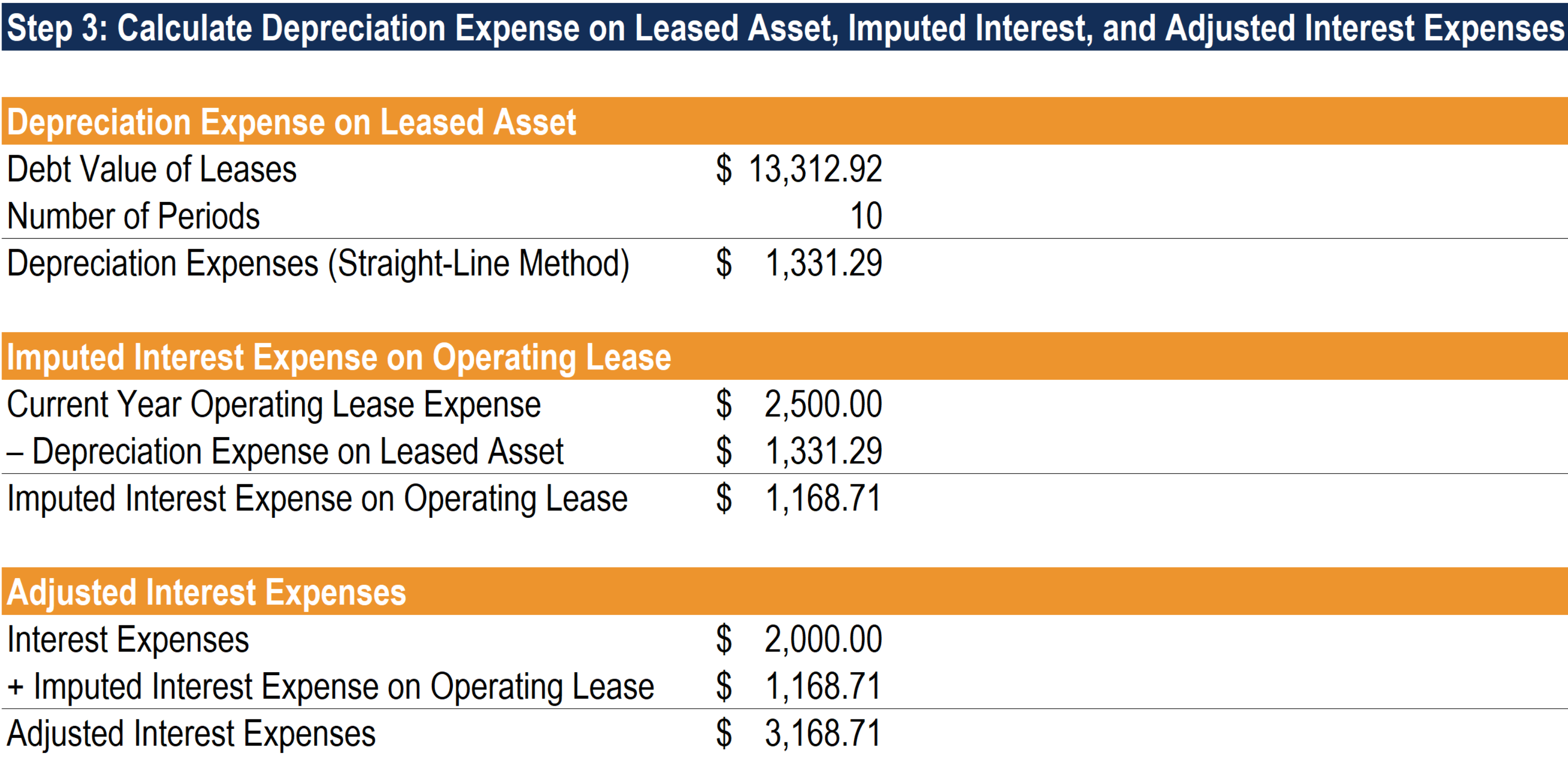

Step 3: Calculate Depreciation Expenses, Imputed Interest, and Adjusted Interest Expenses

We need to calculate depreciation and adjust interest expenses. To calculate depreciation, we use the debt value of leases and employ the straight-line method of depreciationStraight Line DepreciationStraight line depreciation is the most commonly used and easiest method for allocating depreciation of an asset. With the straight line.

To adjust interest expenses, we begin with a simplifying assumption: operating lease expense is equal to the sum of imputed interest expense and depreciation. With this assumption, we can use our newly calculated depreciation value to find imputed interest expense on an operating lease. Take the difference between the current year operating lease expense and our calculated depreciation value to find the imputed interest on the lease.

Finally, add the imputed interest expense on an operating lease to interest expenses to find adjusted interest.

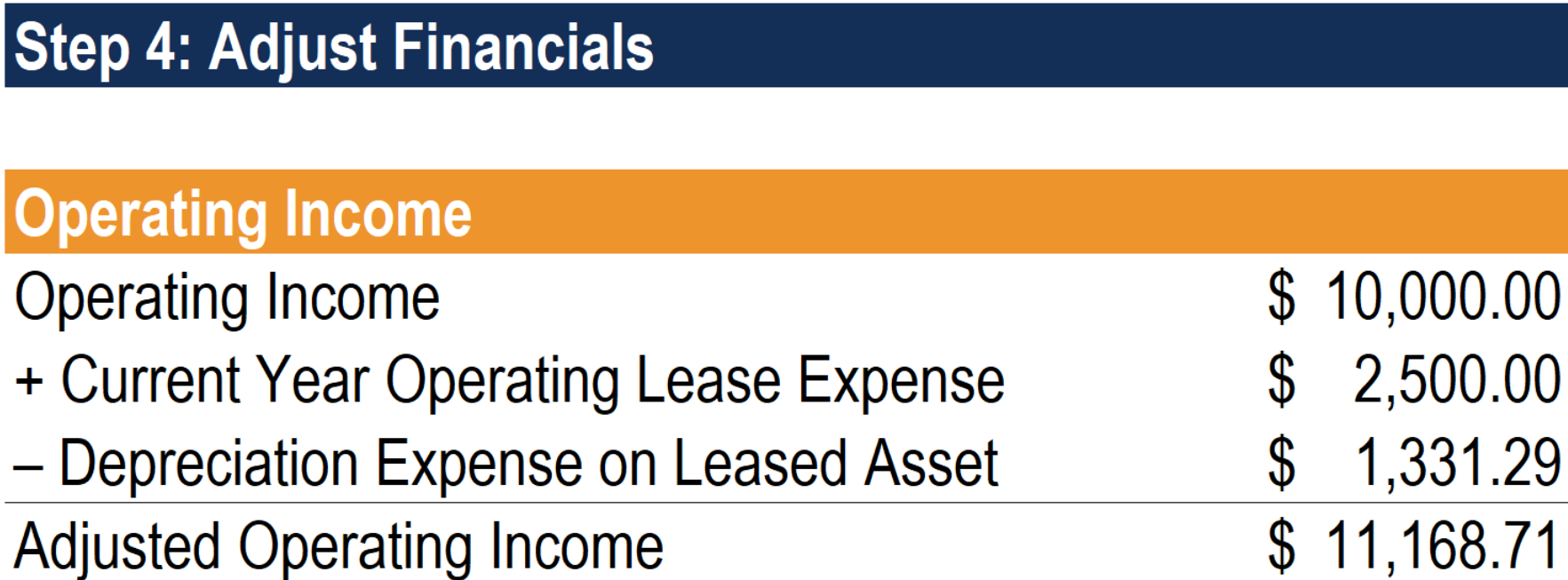

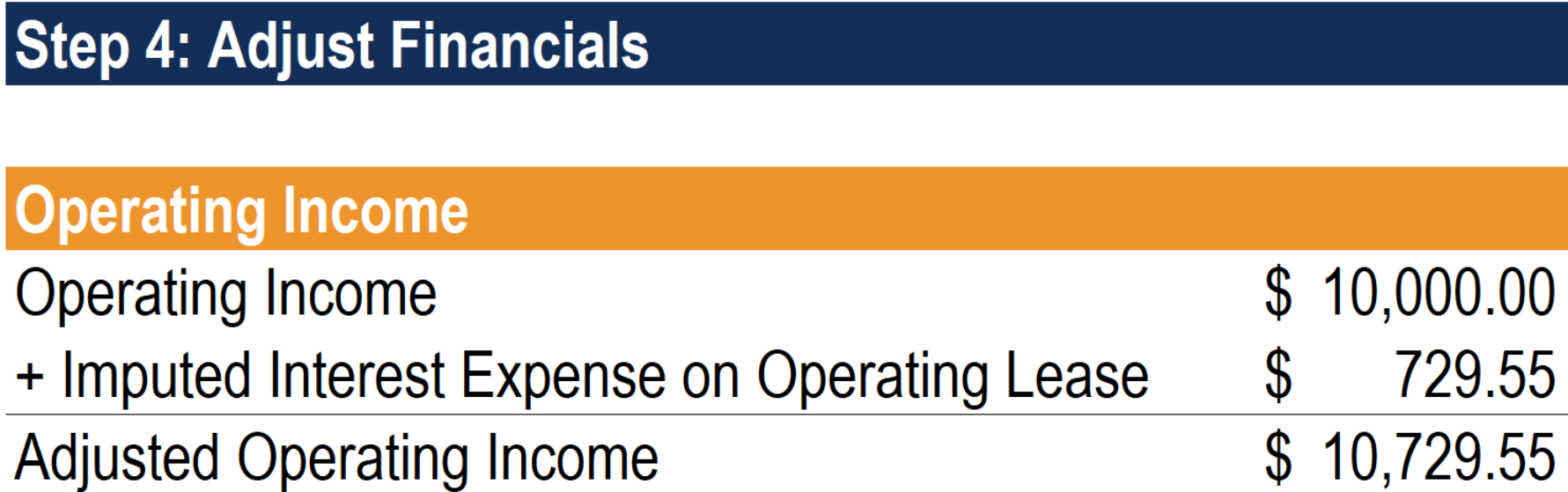

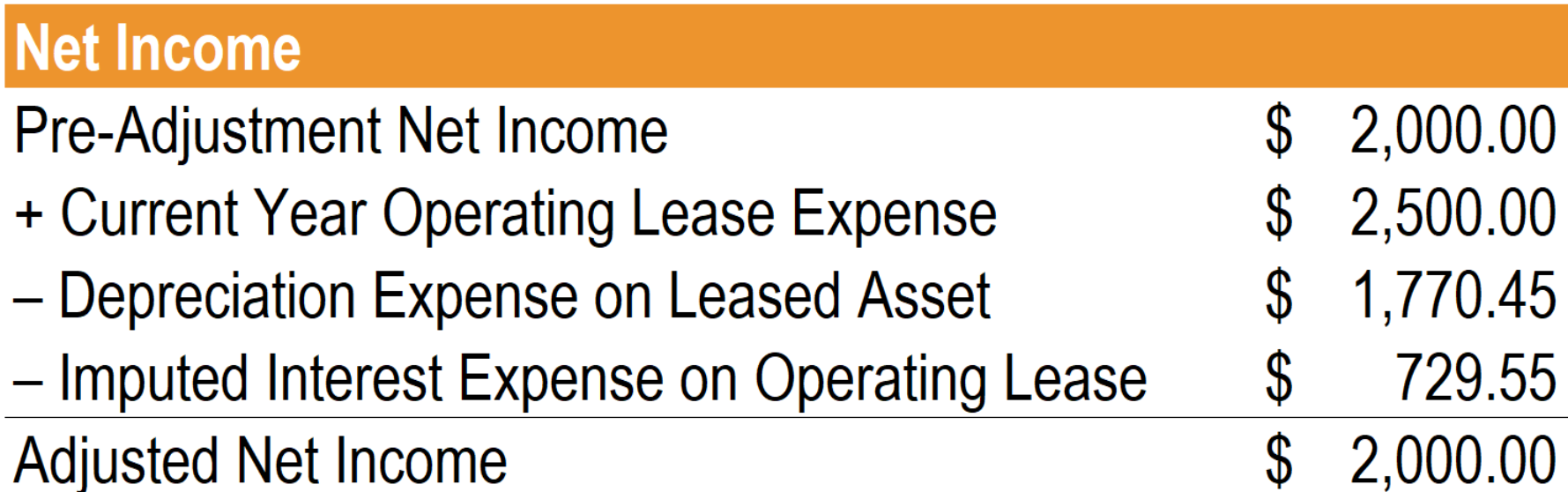

Step 4: Adjust Financials

First, we need to adjust operating income. Begin with the reported operating income (EBIT). Then, add the current year’s operating lease expense and subtract the depreciation on the leased asset to arrive at adjusted operating income.

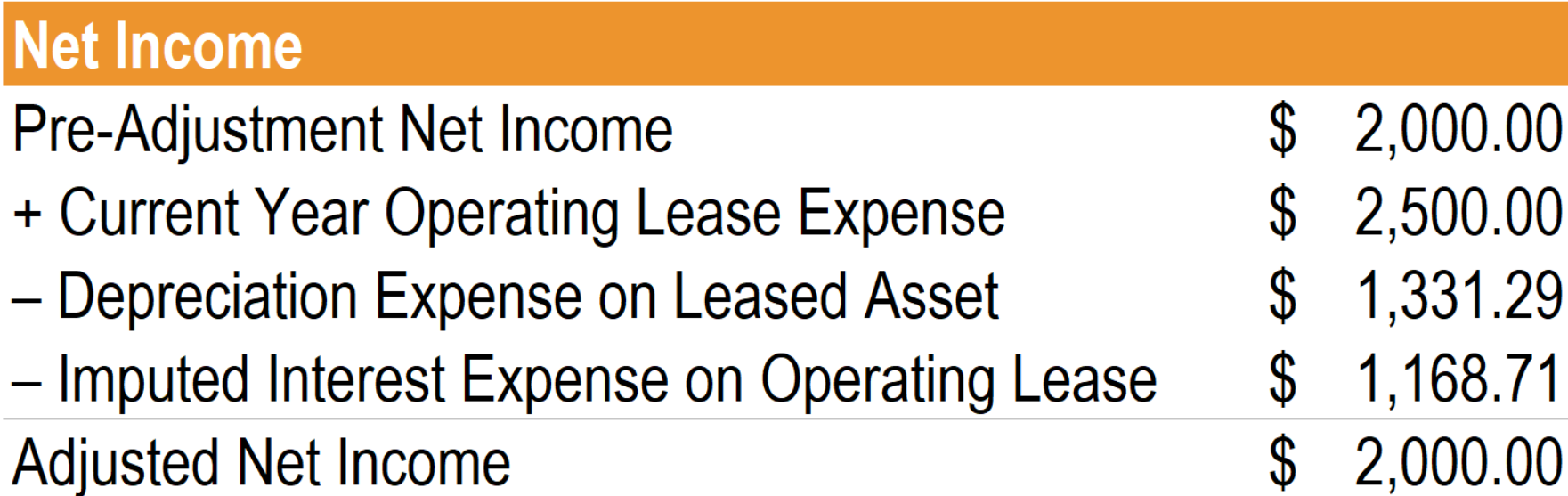

Even though operating income has changed, there should not be a change in net income due to our simplifying assumption. Below are the calculations illustrating this:

Finally, to adjust debt, take the reported value of debt (book value of debt) and add the debt value of the leases.

2. Approximation Method

Step 1: Collect input data

Like the full adjustment method, we will need to collect the same input data.

Step 2: Calculate the Present Value of Operating Lease Commitments

The second step for the approximation method is identical to the second step in the full adjustment method as well. We need to calculate the present value of operating lease commitments to arrive at the debt value of the lease.

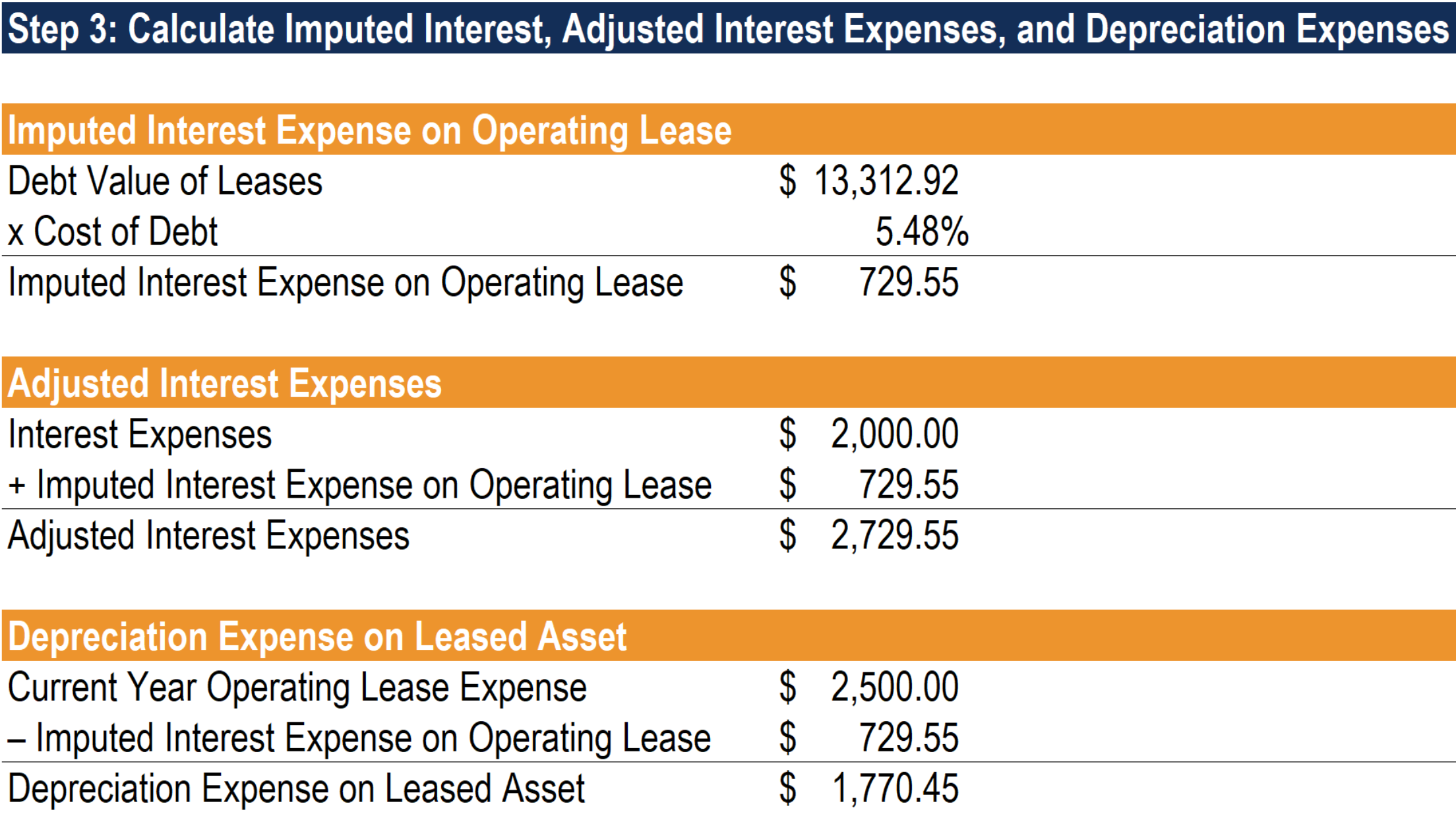

Step 3: Calculate Imputed Interest, Adjusted Interest Expenses, and Depreciation Expenses

Unlike the full adjustment method, the approximation method begins with calculating imputed interest. This is simpler because there is no need to worry about depreciation methods and guidelines. To calculate the imputed interest on the operating lease, multiply the debt value of the lease by the cost of debt.

We can use this imputed interest value to adjust the interest expense. We do this by adding the imputed interest to interest expense.

Finally, using our simplifying assumption from earlier, take the difference between the current year’s operating lease expense and the imputed interest to find depreciation expenses.

Step 4: Adjust Financials

Adjusting financials with the approximation method is slightly different from the full adjustment method. Begin by adjusting operating income. Take the reported operating income (EBIT) for the year and add the calculated imputed interest on an operating lease to obtain the adjusted operating income.

Like with the full adjustment method, though operating income has changed, net income should not. Below are the calculations to illustrate this effect:

Finally, adjusting debt is the same as the full adjustment method. Add the debt value of the leases to the reported debt value.

Impact on Valuation

There are two effects on free cash flow to the firm (FCFF) when we treat operating lease expenses as financing expenses by capitalizing them:

- FCFF will increase because the imputed interest expense on the capitalized operating leases is added back to the operating income (EBIT).

- FCFF will decrease if the present value of leases increases (and vice versa) due to the net change in capital expenditures. This occurs because we must treat operating leases like capital expenditures if we capitalize them.

Furthermore, the weighted average cost of capital (WACC) will decrease as the debt ratio increases, which has a positive impact on the value of the firm. It is important to note that the increase in firm value derives solely from the value of debt, and not the value of equity. If the debt ratio stays stable, and the leases are fairly valued, treating operating leases as debt should have a neutral effect on the value of equity.

Other Resources

We hope you’ve enjoyed reading this CFI guide to leases. To learn more, see the following free CFI resources.

- Lease ClassificationsLease ClassificationsLease classifications include operating leases and capital leases. A lease is a type of transaction undertaken by a company to have the right to use an asset. In a lease, the company will pay the other party an agreed upon sum of money, not unlike rent, in exchange for the ability to use the asset.

- Lease AccountingLease AccountingLease accounting guide. Leases are contracts in which the property/asset owner allows another party to use the property/asset in exchange for money or other assets. The two most common types of leases in accounting are operating and financing (capital leases). Advantages, disadvantages, and examples

- Prepaid LeasePrepaid LeaseA prepaid lease (or operating lease) is a contract to acquire the use of tangible assets, which include plant, equipment, and real estate.

- Projecting Balance Sheet ItemsProjecting Balance Sheet Line ItemsProjecting balance sheet line items involves analyzing working capital, PP&E, debt share capital and net income. This guide breaks down how to calculate

-

Understanding Net Operating Loss (NOL) Deductions | IRS.gov

A net operating loss (NOL) for income tax purposes is when a company’s allowable deductions exceed the taxable income in a tax period. When a company’s deductibles are greater than its act

-

Operating Cash Flow Formula: Calculation & Explanation

The Operating Cash Flow Formula is used to calculate how much cash a company generated (or consumed) from its operating activities in a period, and is displayed on the Cash Flow StatementCash Flow Sta

Accounting

- Understanding Operating Risk: A Key Component of Business Risk

- Capital Lease vs. Operating Lease: Key Differences Explained

- Understanding Leases: Types, Classifications, and Key Concepts

- Net Lease Explained: Understanding Landlord & Tenant Responsibilities

- Understanding Operating Cash Flow (OCF): A Comprehensive Guide

- Understanding the Operating Cycle: Definition & Importance

- Understanding Operating Expenses (OPEX): A Comprehensive Guide

- Operating Income (EBIT): Definition & Calculation

- Understanding Operating Leases: Definition & Benefits

-

Understanding Residential Leases: A Comprehensive Guide

Understanding Residential Leases: A Comprehensive GuideWhen you lease a home, you sign a rental agreement to live there. An executed lease is a legal document that includes your information, the property owner's information, rental terms and signature...

-

Operating Return on Assets (OROA): Definition & Calculation

Operating Return on Assets (OROA): Definition & CalculationOperating return on assets (OROA), an efficiency or profitability ratioProfitability RatiosProfitability ratios are financial metrics used by analysts and investors to measure and evaluate the ability...