Understanding Leases: Types, Classifications, and Key Concepts

Leases are contracts in which the property/asset owner allows another party to use the property/asset in exchange for something, usually money or other assets. The two most common types of leasesLease ClassificationsLease classifications include operating leases and capital leases. A lease is a type of transaction undertaken by a company to have the right to use an asset. In a lease, the company will pay the other party an agreed upon sum of money, not unlike rent, in exchange for the ability to use the asset. in accounting are operating and financing (capital lease) leases. This step-by-step guide covers all the basics of lease accounting.

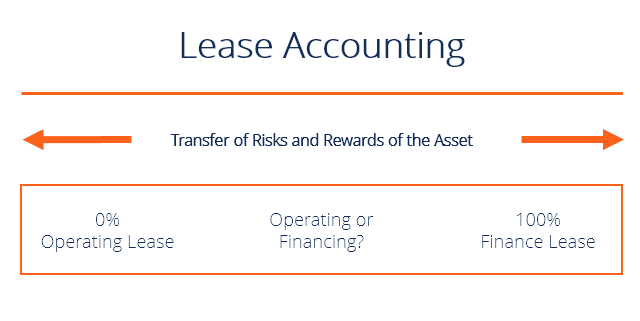

Operating lease vs financing lease (capital lease)

The two most common types of leases are operating leases and financing leases (also called capital leases). In order to differentiate between the two, one must consider how fully the risks and rewards associated with ownership of the asset have been transferred to the lessee from the lessor.

If these risks and rewards have been fully transferred, it is called a financing lease under IFRS StandardsIFRS StandardsIFRS standards are International Financial Reporting Standards (IFRS) that consist of a set of accounting rules that determine how transactions and other accounting events are required to be reported in financial statements. They are designed to maintain credibility and transparency in the financial world. Under ASPE, financing leases are called capital leases. Otherwise, it is an operating lease, which is basically the same as a landlord and renter contract.

Whether the risks and rewards have been fully transferred can be unclear sometimes, thus IFRS outlines several criteria to distinguish between the two leases.

At least one of the following criteria must be met in order to consider the lease a financing lease:

- There is a bargain purchase option – an option given to the lessee to purchase the asset at a price lower than its fair value at a future date (typically the end of the lease term). This option is usually determined at the beginning of the lease.

- The life of the lease is for a significant portion of the useful economic life of the asset (generally, 75% or more).

- The net present value (NPV)Net Present Value (NPV)Net Present Value (NPV) is the value of all future cash flows (positive and negative) over the entire life of an investment discounted to the present. of minimum lease payments is at least 90% of the asset’s fair value.

The advantages of leasing

Leasing provides a number of benefits that can be used to attract customers:

- Payment schedules are more flexible than loan contracts.

- After-tax costs are lower because tax rates are different for the lessor and the lessee.

- Leasing involves 100% financing of the price of the asset.

- For an operating lease, the company will create an expense instead of a liability, allowing the company to obtain financial funding – often referred to as “off-balance-sheet financing”.

Disadvantages of leasing

One major disadvantage of leasing is the agency cost problem. In a lease, the lessor will transfer all rights to the lessee for a specific period of time, creating a moral hazard issue. Because the lessee who controls the asset is not the owner of the asset, the lessee may not exercise the same amount of care as if it were his/her own asset. This separation between the asset’s ownership (lessor) and control of the asset (lessee) is referred to as the agency cost of leasing. This is an important concept in lease accounting.

Lease accounting example and steps

Let’s walk through a lease accounting example. On January 1, 2017, XYZ Company signed an 8-year lease agreement for equipment. Annual payments are $28,500, to be made at the beginning of each year. At the end of the lease, the equipment will revert to the lessor. The equipment has a useful life of 8 years and has no residual value. At the time of the lease agreement, the equipment has a fair value of $166,000. An interest rate of 10.5% and straight-line depreciation are used.

Step 1: Identify the type of lease

- There is no bargain purchase option because the equipment will revert back to the lessor.

- The life of the lease is 8 years and the economic life of the asset is 8 years. This is 100%.

- Using a financial calculator, calculate for the PV of the minimum lease payments:

- N = 8

- I/YR = 10.5

- FV = 0

- PMT = 28,500

- PV = 164,995

- Therefore, 164,995/166,000 = 99%

Conclusion: This is a financing/capital lease because at least one of the finance lease criteria is met and during the lease, the risks and rewards of the asset have been fully transferred. We have determined the proper lease accounting.

Step 2: Lease amortization schedule

OpeningInterestPrincipalClosingYear BalanceExpensePaymentPaymentBalance1 $136,495 $14,332 $28,500 $14,168 $122,3272 122,327 12,844 28,500 15,656 106,6713 106,671 11,201 28,500 17,299 89,3724 89,372 9,384 28,500 19,116 70,2565 70,256 7,377 28,500 21,123 49,1336 49,132.90 5,158.95 28,500 23,341.05 25,791.867 $25,792 $2,708 $28,500 $25,792 $0

Step 3: Journal entries

January 1, 2017

DR Equipment 164,995

CR Cash 28,500

CR Lease Liability 136,495

The equipment account is debited by the present value of the minimum lease payments and the lease liability account is the difference between the value of the equipment and cash paid at the beginning of the year.

December 31, 2017

DR Depreciation Expense 20,624

CR Accumulated Depreciation 20,624

Depreciation expense must be recorded for the equipment that is leased.

DR Interest Expense 14,332

CR Interest Payable 14,332

January 1, 2018

DR Interest Payable 14,332

DR Lease Liability 14,168

CR Cash 28,500

Additional resources

This has been a guide to lease accounting and understanding operating leases, capital leases, and the debits and credits to account for them. You can read more about lease accounting on the IFRS website http://www.ifrs.org/ias-17-leases/

To keep learning and developing your financial knowledge, we recommend these additional CFI resources:

- Prepaid leasePrepaid LeaseA prepaid lease (or operating lease) is a contract to acquire the use of tangible assets, which include plant, equipment, and real estate.

- Lease classificationsLease ClassificationsLease classifications include operating leases and capital leases. A lease is a type of transaction undertaken by a company to have the right to use an asset. In a lease, the company will pay the other party an agreed upon sum of money, not unlike rent, in exchange for the ability to use the asset.

- Pension accountingPension AccountingPension accounting guide and example, Steps include, record company contribution, record pension expense, and adjust pension liability to

- Goodwill impairment accountingGoodwill Impairment AccountingGoodwill is acquired and recorded on the books when an entity purchases another entity for more than the fair market value of its assets.

-

Securities Explained: Types, Categories & Trading in the US

A security is a financial instrument, typically any financial asset that can be traded. The nature of what can and can’t be called a security generally depends on the jurisdiction in which the a

-

Asset Swap Explained: Definition, OTC Trading & Key Concepts

An asset swap is a derivative contract between two parties that swap fixed and floating assets. The transactions are done over-the-counterOver-the-Counter (OTC)Over-the-counter (OTC) is the trading of

Accounting

- Asset Disposal: Definition, Types & Financial Statement Impact

- Depreciated Cost Explained: Calculation & Importance

- Historical Cost Accounting: Definition & Importance

- Impaired Assets: Definition, Recognition, and Accounting Standards

- Understanding Lease Classifications: Operating vs. Capital Leases

- Lessor vs. Lessee: Understanding Lease Agreements

- Operating Lease Explained: Benefits & How They Work

- Understanding Operating Leases: Definition & Benefits

- Synthetix: A Decentralized Platform for Synthetic Asset Trading

-

Forward Contracts: Definition, How They Work & Examples

Forward Contracts: Definition, How They Work & ExamplesA forward contract, often shortened to just forward, is a contract agreement to buy or sell an assetAsset ClassAn asset class is a group of similar investment vehicles. They are typically traded in th...

-

Non-Performing Assets (NPAs): Definition & Implications

Non-Performing Assets (NPAs): Definition & ImplicationsA non-performing asset (NPA) is a classification used by financial institutions for loans and advances on which the principal is past due and on which no interest paymentsInterest PayableInterest Paya...