Understanding Non-Recurring Items in Financial Statements

In accounting, a non-recurring item is an infrequent or abnormal gain or loss that is reported in the company’s financial statementsThree Financial StatementsThe three financial statements are the income statement, the balance sheet, and the statement of cash flows. These three core statements are. Unlike other items reported by a company, non-recurring items do not arise from the normal company’s operations. The items are generally caused by unusual and infrequent events that are not likely to happen again in the future.

Non-Recurring Items in Financial Analysis

Understanding the nature of a non-recurring item and its impact on a company’s profitability is crucial in financial valuation. Generally, analysts adjust their profitability analysis for non-recurring items. Since the items arise from extraordinary events and/or occur only once, it is not likely that they will affect the company’s future long-term profitability.

However, analysts should still carefully assess the guidance on non-recurring items provided by the company’s managementCorporate StructureCorporate structure refers to the organization of different departments or business units within a company. Depending on a company’s goals and the industry. It may turn out to be that the non-recurring items can reoccur in the future, impacting the company’s profitability.

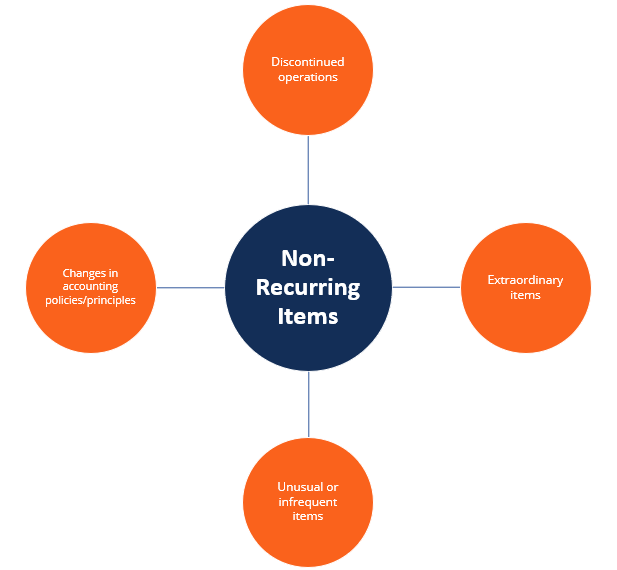

Types of Non-Recurring Items

Generally, we can derive four main types of non-recurring items:

- Discontinued operations: Relates to the disposal of a company’s segment or division distinct from the continuous company’s operations that generate recurring net incomeNet IncomeNet Income is a key line item, not only in the income statement, but in all three core financial statements. While it is arrived at through.

- Extraordinary items: Non-recurring items that are both unusual and infrequent in their nature. The best examples of extraordinary items are losses arising from natural disasters.

- Unusual or infrequent items: Non-recurring items that are either unusual or infrequent in their nature. They include various items such as gains/losses on a sale of a subsidiary, restructuring costs, and asset impairments.

- Changes in accounting policies: This refers to the company’s decision to voluntarily change its accounting policies or make changes in accounting principles that may change the values of certain recurring items reported by a company. The impact of the changes is recorded as a gain or loss.

Accounting Reporting of Non-Recurring Items

Non-recurring items are reported by a company on the income statement. Depending on the type of item, it may be reported as before-tax or after-tax. Generally, unusual or infrequent items are reported before tax.

In addition, the nature of such items is usually discussed in detail in the management discussion and analysis (MD&A) section of the company’s financial reports. In addition, detailed information about the items can be found in the footnotes to the financial statements.

More Resources

CFI is the official provider of the Financial Modeling and Valuation Analyst (FMVA)Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today!®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

- How the 3 Financial Statements are LinkedHow the 3 Financial Statements are LinkedHow are the 3 financial statements linked together? We explain how to link the 3 financial statements together for financial modeling and

- Projecting Income Statement Line ItemsProjecting Income Statement Line ItemsWe discuss the different methods of projecting income statement line items. Projecting income statement line items begins with sales revenue, then cost

- Projecting Balance Sheet ItemsProjecting Balance Sheet Line ItemsProjecting balance sheet line items involves analyzing working capital, PP&E, debt share capital and net income. This guide breaks down how to calculate

- Revenue Recognition PrincipleRevenue Recognition PrincipleThe revenue recognition principle dictates the process and timing by which revenue is recorded and recognized as an item in a company's

-

Understanding Financial Systems: Institutions & Key Players

A financial system is a network of financial institutions – such as insurance companies, stock exchanges, and investment banksList of Top Investment BanksList of the top 100 investment banks in

-

Understanding Guarantees: Protecting Lenders and Borrowers

A guarantee is a legal promise made by a third party (guarantor) to cover a borrower’s debt or other types of liability in case of the borrower’s defaultDebt DefaultA debt default happens

Accounting

- Understanding Financial Hardship: Causes, Impacts & Relief

- Understanding Auditors: Roles, Responsibilities & Audit Processes

- EBITDARM Explained: A Comprehensive Guide to Financial Analysis

- Eurocurrency Explained: What It Is & How It Works

- Factset: Financial Data & Analytics Solutions for Investment Professionals

- Accounting Explained: Understanding Financial Records & Reporting

- Understanding Financial Audits: A Comprehensive Guide

- Understanding Finance: A Comprehensive Overview

- Understanding Special Items: Definition and Significance

-

Understanding Financial Performance: A Comprehensive Overview

Understanding Financial Performance: A Comprehensive OverviewFinancial performance is a complete evaluation of a company’s overall standing in categories such as assets, liabilities, equity, expenses, revenue, and overall profitability. It is measured thr...

-

Comprehensive Financial Planning: Your Path to Financial Security

Comprehensive Financial Planning: Your Path to Financial SecurityA financial plan is a document that covers an individual’s current financial situation, short-term and long-term economic goals, and an in-depth strategy to achieve the goals. A finan...