Understanding Subsequent Events in Financial Reporting

Subsequent events are events that occur after a company’s year-end period but before the release of the financial statementsThree Financial StatementsThe three financial statements are the income statement, the balance sheet, and the statement of cash flows. These three core statements are. In other words, subsequent events are events that happen between the cut-off date and the date in which the company issues its financial statements. Depending on the situation, subsequent events may require disclosureIFRS StandardsIFRS standards are International Financial Reporting Standards (IFRS) that consist of a set of accounting rules that determine how transactions and other accounting events are required to be reported in financial statements. They are designed to maintain credibility and transparency in the financial world in a company’s financial statements.

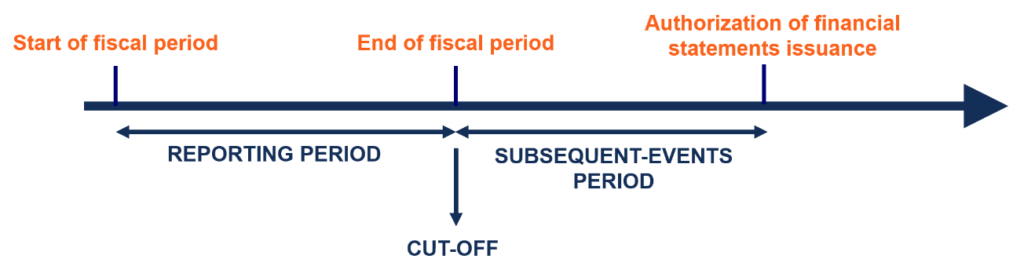

Understanding Reporting Period, Cut-off, and Subsequent Events

The typical reporting periodFiscal Year (FY)A fiscal year (FY) is a 12-month or 52-week period of time used by governments and businesses for accounting purposes to formulate annual for a company is 12 months. However, a reporting period does not need to match the calendar year from January 1 to December 31. Typically, companies will choose a year-end corresponding to a period of low activity. For example, retailers usually follow a year-end at the end of January when inventory is low (post-holiday season).

The cut-off date refers to the end of the reporting period and the start of the new reporting period. It is important in accrual accounting because cash cycles may not be complete. Therefore, it is necessary to understand which events will be during the current reporting period and which events will be recorded in the next reporting period. Transactions and events are recognized up to the cut-off date.

Between the period of the cut-off date and the authorization of financial statements issuance is the subsequent events period. Depending on the type of subsequent event, it may or may not require an adjustment to the financial statements. Transactions and events that change the measurement of transactions before the cut-off date are recognized.

Example

After the cut-off period (after the company’s year-end) and before the issuance of financial statements, Company A’s major client unexpectedly goes bankrupt. It is determined that the company will only get 10% of its outstanding accounts receivableAccounts ReceivableAccounts Receivable (AR) represents the credit sales of a business, which have not yet been collected from its customers. Companies allow from the major client. The event will require an adjustment to the financial statements of Company A.

Types of Subsequent Events

There are two types of subsequent events:

1. Adjusting events

An event that provides additional information about pre-existing conditions that existed on the balance sheet date.

2. Non-adjusting events

A subsequent event that provides new information about a condition that did not exist on the balance sheet date.

Accounting for Subsequent Events

For subsequent events that provide additional information about pre-existing conditions that existed on the balance sheet date, the financial statements are adjusted to reflect this additional information.

For example:

- If the company faced a lawsuit before the balance sheet date and the lawsuit is settled during the subsequent-events period, the company would adjust the contingent loss amount to match the actual settlement loss.

- Assume that, due to new technology, there is a significant reduction in the market price of Company A’s inventory. This will require an adjustment to the financial statements, with inventory valued at the lower of cost or market value.

For subsequent events that are new events and thus do not provide additional information about pre-existing conditions that existed on the balance sheet, these events are not recognized in the financial statements. However, a subsequent event footnote disclosure should be made so that investors know the event occurred.

For example:

- A labor strike that could potentially threaten the company into bankruptcy should be disclosed in the financial statements.

- A fire in the company’s warehouse that destroys inventory and assets is not recognized (but disclosure is required) because the conditions did not exist prior to the balance sheet date.

Related Readings

CFI offers the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

- Financial Accounting TheoryFinancial Accounting TheoryFinancial Accounting Theory explains the why behind accounting - the reasons why transactions are reported in certain ways. This guide will

- Projecting Income Statement Line ItemsProjecting Income Statement Line ItemsWe discuss the different methods of projecting income statement line items. Projecting income statement line items begins with sales revenue, then cost

- Projecting Balance Sheet ItemsProjecting Balance Sheet Line ItemsProjecting balance sheet line items involves analyzing working capital, PP&E, debt share capital and net income. This guide breaks down how to calculate

- Analysis of Financial Statements Analysis of Financial StatementsHow to perform Analysis of Financial Statements. This guide will teach you to perform financial statement analysis of the income statement,

-

Understanding Financial Audits: A Comprehensive Guide

An audit refers to an examination of the financial statements of a company. Audits are conducted to provide investors and other stakeholders with confidence that a company’s financial reports ar

-

Understanding Finance: A Comprehensive Overview

In financeFinance OverviewFinance is defined as the providing of funding and management of money for individuals, businesses, and governments. The financial system includes the circulation of money, m

Accounting

- Understanding Financial Barriers: How Costs Impact Your Lifestyle

- Financial Covenants: Definition, Types & Importance

- Robo-Advisors: A Comprehensive Guide to Automated Investment Management

- Understanding Audit Assertions: A Comprehensive Guide

- Understanding Cash Equivalents: Definition & Examples

- Understanding Financial Assets: Definitions & Types

- Understanding Financial Statements: A Comprehensive Guide

- Understanding Intersegment Sales: Definition & Reporting

- Understanding Financial Services: A Comprehensive Guide

-

Accounting Explained: Understanding Financial Records & Reporting

Accounting Explained: Understanding Financial Records & ReportingAccounting is a term that describes the process of consolidating financial information to make it clear and understandable for all stakeholders and shareholdersShareholderA shareholder can be a person...

-

Why Do You Save Money? Understanding Your Savings Goals

Last week, I wrote about a conversation with my investment adviser. In the article, I mentioned that my current income roughly covers my current spending except that Ive been spending an average ...