Understanding Variable Overhead Efficiency Variance: A Comprehensive Guide

Variable overhead efficiency variance is a measure of the difference between the actual costs to manufacture a product and the costs that the business entity budgeted for it. Thus, it can arise from a difference in productive efficiency.

The productivity efficiency variance is the difference between the actual number of labor hoursLabor Force KPIsHow can we monitor the labor force? Governments and economists usually refer to three main key performance indicators (KPIs) to assess the strength of a nation's labor force required to manufacture a certain number of a product and the budgeted or standard number of hours. The difference can be significant and needs to be monitored and managed.

Variable overhead efficiency variance is one of the factors that impact the total variable overhead variance. The other important factor is the variable overhead spending varianceVariable Overhead Spending VarianceVariable overhead spending variance is essentially that cost associated with running a business that varies with fluctuations in operational activity..

Variable Overhead Efficiency Variance – Formula

Variable overhead efficiency variance is essentially an accounting measure that is calculated by multiplying the difference between the actual and budgeted hours worked with the standard variable overhead rate per hour. The formula for calculating the variable overhead efficiency variance is:

When a favorable variance is achieved, it implies that the actual hours worked during the given period were less than the budgeted hours. It results in applying the standard overhead rate across fewer hours, which means that the total expensesExpensesAn expense is a type of expenditure that flows through the income statement and is deducted from revenue to arrive at net income. Due to the being incurred are reduced by a factor of the decrease in hours worked. It does not necessarily mean that, in actual terms, the company incurred a lower overhead. It simply implies that an improvement was seen in the total allocation base used to apply overhead.

Risk of Error

The variable overhead efficiency variance uses inputs provided by different departments within the organizationTypes of OrganizationsThis article on the different types of organizations explores the various categories that organizational structures can fall into. Organizational structures. The production expense information is submitted by the production department of the enterprise. The estimated labor hours to meet output requirements are estimated by the staff responsible for industrial engineering and production scheduling.

Projections are based on two things: the historical and estimated employee efficiency, or labor productivity, and the capacity levels of the equipment, with depreciation being accounted for.

There is an inherent risk of arriving at a variance that does not represent an entity’s actual performance due to a margin of error. The error can directly result from an incorrect estimation or record of the standard number of labor hours. Therefore, the validity of the underlying standard, or lack thereof, must be accounted for in investigating the variable overhead efficiency variance.

Example

Assume that the cost accounting staff of Company X has calculated that the company’s production staff works 10,000 hours per month. The company also incurs a cost of $100,000 per month as its variable overhead costs. The information given is largely based on historical and projected labor patterns.

A few months later, Company X decided to install a new materials handling system. It is supposed to have a significant impact on production efficiency. The overall efficiency improves, and the total hours worked during the month drops to 9,000 from the previous 10,000. In this case, the variable overhead efficiency variance is as follows:

Given information:

Standard Hours = 10,000

Hours Worked = 9,000

Calculation:

Standard Overhead Rate per Hour = Cost Incurred / Standard Hours

= $100,000 / 10,000

= $10

Therefore, the company established a variable overhead rate of $10 per hour.

$10 Standard Overhead Rate / Hour x (9,000 Hours Worked – 10,000 Standard Hours)

= $10,000 (Variable Overhead Efficiency Variance)

Related Readings

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

- Variance Analysis TemplateVariance Analysis TemplateThis variance analysis template guides you through the process of variance analysis using the column method. Variance analysis can be summarized as an analysis of the difference between planned and actual numbers. The sum of all variances gives information on the over-applied or under-applied values for the company’s r

- Philosophy of AccountingPhilosophy of AccountingThe philosophy of accounting encompasses the general rules, concepts, and ideas surrounding the preparation and auditing of the accounts and

- Variance FormulaVariance FormulaThe variance formula is used to calculate the difference between a forecast and the actual result.

- Budgeting and Forecasting Course

-

Understanding Variable Price Limits in Futures Contracts

Variable price limits allow futures contracts to move beyond their fixed price limits in a single day. Due to the high volatility of the commoditiesCommoditiesCommodities are another class of assets j

-

Understanding Variable Interest Entities (VIEs): Definition & Examples

A variable interest entity (VIE) may be any type of legal business structure. It can be, for instance, a trust, a partnership, a corporation, or joint ventureJoint Venture (JV)A joint venture (JV) is

Accounting

- Budget Variance Explained: Causes, Types & Analysis

- Portfolio Variance: Understanding Risk and Diversification

- Allocative Efficiency: Understanding Optimal Resource Allocation

- Revenue Variance Analysis: Understanding Sales Performance & Forecasting

- Variable Costing Explained: A Clear Guide for Businesses

- Understanding Variable Costs: Definition & Examples

- Understanding Variable Overhead Costs: A Comprehensive Guide

- Variable Overhead Spending Variance: Definition & Analysis

- Variance Analysis: Understanding & Improving Performance

-

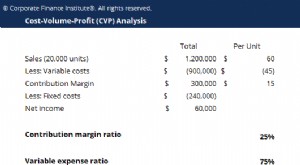

CVP Analysis: Understand Break-Even & Profitability

CVP Analysis: Understand Break-Even & ProfitabilityCost-Volume-Profit Analysis (CVP analysis), also commonly referred to as Break-Even Analysis, is a way for companies to determine how changes in costs (both variable and fixedFixed and Variable CostsC...

-

Variance Swaps: Understanding Volatility Derivatives

Variance Swaps: Understanding Volatility DerivativesVariance swap refers to an over-the-counter financial derivative that allows the holder to speculate on the future volatility of a given underlying asset. Holders use variance swaps to hedge their exp...