Variable Costing Explained: A Clear Guide for Businesses

Variable costing is a concept used in managerial and cost accounting in which the fixed manufacturing overhead is excluded from the product-cost of production. The method contrasts with absorption costingAbsorption CostingAbsorption costing is a costing system that is used in valuing inventory. It not only includes the cost of materials and labor, but also both, in which the fixed manufacturing overhead is allocated to products produced. In accounting frameworks such as GAAP and IFRSIFRS StandardsIFRS standards are International Financial Reporting Standards (IFRS) that consist of a set of accounting rules that determine how transactions and other accounting events are required to be reported in financial statements. They are designed to maintain credibility and transparency in the financial world, variable costing cannot be used in financial reporting.

Variable Costing in Financial Reporting

Although accounting frameworks such as GAAP and IFRS prohibit the use of variable costing in financial reporting, this costing method is commonly used by managers to:

- Conduct break-even analysisBreak Even AnalysisBreak Even Analysis in economics, financial modeling, and cost accounting refers to the point in which total cost and total revenue are equal. to determine the number of units needed to be sold to begin earning a profit

- Determine the contribution marginContribution MarginContribution margin is a business’ sales revenue less its variable costs. The resulting contribution margin can be used to cover its fixed on a product, which helps to understand the relationship between cost, volume, and profit

- Facilitate decision-making by excluding fixed manufacturing overhead costs, which can create problems due to how fixed costs are allocated to each product

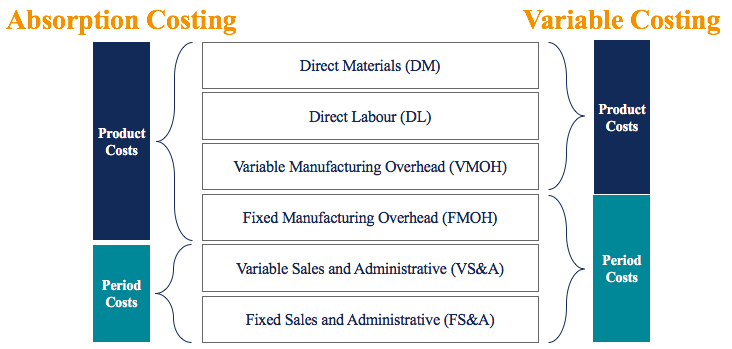

Variable Costing vs. Absorption Costing

Under variable costing, the following costs go into the product:

- Direct material (DM)

- Direct labor (DL)

- Variable manufacturing overhead (VMOH)

Under absorption costing, the following costs go into the product:

- Direct material (DM)

- Direct labor (DL)

- Variable manufacturing overhead (VMOH)

- Fixed manufacturing overhead (FMOH)

For your reference, the diagram provided below provides an overview of which costs go into variable costing vs. absorption costing methods:

Note that product costs are costs that go into the product while period costs are costs that are expensed in the period incurred.

Example of Variable Costing

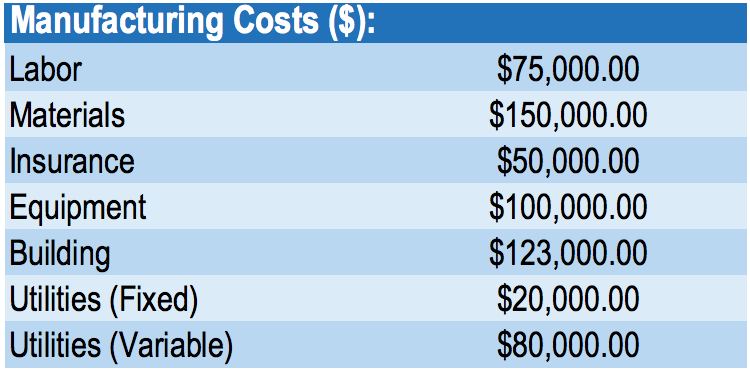

IFC is a manufacturer of phone cases. Below are excerpts from the company’s income statement for its latest year-end (2018):

IFC does not report an opening inventory. During 2018, the company manufactured 1,000,000 phone cases and reported total manufacturing costs of $598,000 (around $0.60 per phone case).

The manufacturer recently received a special order for 1,000,000 phone cases at a total price of $400,000. Despite having ample capacity, the manager is reluctant to accept this special order because it is below the cost of $598,000 to manufacture the initial 1,000,000 phone cases as outlined in the company’s income statement. Being the company’s cost accountant, the manager wants you to determine whether the company should accept this order.

First, it is important to know that $598,000 in manufacturing costs to produce 1,000,000 phone cases includes fixed costs such as insurance, equipment, building, and utilities. Therefore, we should use variable costing when determining whether to accept this special order.

Variable costing:

- Direct material of $150,000

- Direct labor of $75,000

- Variable manufacturing overhead of $80,000

Total = $305,000 / 1,000,000 units produced = $0.305 variable cost per case

Cost to produce special order of 1,000,000 phone cases = $0.305 x 1,000,000 = $305,000. Therefore, there is a contribution margin of $400,000 – $305,000 = $95,000.

Based on our variable costing method, the special order should be accepted. The special order will add $95,000 of profits to the company.

It is crucial to understand why the manager was reluctant to accept the order. The manager included fixed costs in the cost calculation, which is incorrect in decision-making. Given ample capacity, the company will not incur additional fixed costs to produce the special order of 1,000,000. As you can see, variable costing plays an important role in decision-making!

Why Variable Costing is not Permitted in External Reporting

In accordance with the accounting standards for external financial reporting, the cost of inventory must include all costs used to prepare the inventory for its intended use. It follows the underlying guidelines in accounting – the matching principle. Absorption costing better upholds the matching principle, which requires expenses to be reported in the same period as the revenue generated by the expenses.

Variable costing poorly upholds the matching principle, as related expenses are not recognized in the same period as related revenue. In our example above, under variable costing, we would expense all fixed manufacturing overhead in the period occurred.

However, if the company fails to sell all the inventory manufactured in that year, there would be poor matching between revenues and expenses on the income statement. Therefore, variable costing is not permitted for external reporting. It is commonly used in managerial accounting and for internal decision-making purposes.

Related Readings

CFI offers the Financial Modeling & Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

- Activity-based CostingActivity-Based CostingActivity-based costing is a more specific way of allocating overhead costs based on “activities” that actually contribute to overhead costs. An activity is

- Cost DriverCost DriverA cost driver is the direct cause of a cost, and its effect is on the total cost incurred. For example, if you are to determine the amount of electricity consumed in a particular period, the number of units consumed determines the total bill for electricity. In such a scenario, the units of electricity consumed

- Fixed and Variable CostsFixed and Variable CostsCost is something that can be classified in several ways depending on its nature. One of the most popular methods is classification according

- Target CostingTarget CostingTarget costing is not just a method of costing, but rather a management technique wherein prices are determined by market conditions, taking

-

Understanding Step Costs: A Guide for Business Growth

Step costs, also called stair-step costs, are costs that do not change in direct proportion to increasing levels of activity. In other words, step costs are constant at a certain activity level but in

-

Variable Cost Ratio: Definition, Calculation & Importance

The variable cost ratio is a cost accounting tool used to express a company’s variable production costs as a percentage of its net sales. The ratio is calculated by dividing the variable costs b

Accounting

- Absorption Costing: A Comprehensive Guide for Businesses

- Accounting Profit Explained: Calculation & Importance

- Backflush Costing: Definition, Benefits & Implementation

- Understanding Depreciation Expense: A Comprehensive Guide

- Understanding Asset Disposition: Definition & Tax Implications

- Flat Tax Explained: How It Works & Its Implications

- Gross Income Explained: Definition, Sources & Examples

- Target Costing: A Comprehensive Guide to Value-Based Pricing

- Variable Costing Explained: A Clear Guide for Businesses

-

Activity-Based Costing (ABC): A Comprehensive Guide

Activity-Based Costing (ABC): A Comprehensive GuideActivity-based costing is a more specific way of allocating overhead costs based on “activities” that actually contribute to overhead costs. In job-order costingJob Order Costing GuideJob ...

-

Job Order Costing: A Comprehensive Guide for Businesses

Job Order Costing: A Comprehensive Guide for BusinessesIn managerial accounting, there are two general types of costing systems to assign costs to products or services that the company provides: “job order costing” and “process costing&r...