Compound Interest Explained: How It Works & Benefits

Compound interest refers to interest payments that are made on the sum of the original principalPrincipalPrincipal in bonds is their par value. It is the initial investment paid for a security or bond and does not include interest derived. and the previously paid interest. An easier way to think of compound interest is that is it “interest on interest,” where the amount of the interest payment is based on changes in each period, rather than being fixed at the original principal amount.

Compound interest enables investors to earn potentially very high returns over a long time horizon and is essentially a risk-free way to generate gains. It is very different from equity investments, where capital gainsCapital Gains YieldCapital gains yield (CGY) is the price appreciation on an investment or a security expressed as a percentage. Because the calculation of Capital Gain Yield involves the market price of a security over time, it can be used to analyze the fluctuation in the market price of a security. See calculation and example are only realized if the security’s market value increases over time (i.e., buy low, sell high).

Compound interest isn’t entirely risk-free, as the interest payer can default or interest rates can change. However, the mechanism of compound interest is what makes it relatively riskless compared to other investments.

Components of Compound Interest

The following are the four main components of compound interest:

1. Principal

The principal is the amount that is originally deposited in a compounding environment (for example, a high-interest savings account at a bankTop Banks in the USAAccording to the US Federal Deposit Insurance Corporation, there were 6,799 FDIC-insured commercial banks in the USA as of February 2014. ). It is the starting amount upon which the first interest payment is calculated.

2. Interest rate

The interest rateInterest RateAn interest rate refers to the amount charged by a lender to a borrower for any form of debt given, generally expressed as a percentage of the principal. refers to the rate that is paid on the account value. The interest payment will be equal to the interest rate times the account value (which is the sum of the original principal and any previously paid interest).

3. Compounding Frequency

The compounding frequency determines how many times a year the interest is paid. It will influence the interest rate itself as high-frequency compounding will typically only be available with lower rates. Typically, compounding occurs on a monthly, quarterly, or annual basis.

4. Time horizon

Time horizon refers to the amount of time over which the compound interest mechanism can operate. The longer the time horizon, the more interest payments that can be made and the larger the ending account value will be.

Time horizon is the single most important component of compound interest, as it essentially dictates the future profitability of an investment. A compounding environment with low rates and low compounding frequency can still be attractive if the available time horizon is very long.

Practical Example: Compound Interest

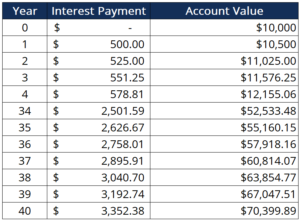

Sam wants to start saving and decides to deposit money into a high-interest savings account. He deposits an initial $10,000, which is to be compounded yearly at a rate of 5% per month. Sam is currently 20 years old and plans to retire at 60, which means that he can avail himself of a 40-year time horizon over which to accumulate interest.

Taking into account the given information, the table below calculates how much Sam’s account value would be at the end of his time horizon:

Here, we see that the account value at the end of the 40-year period is about $70,000. It shows the power of compound interest, as Sam was able to multiply his money seven-fold without actively managing the investment. We see how as interest accumulated on the principal, the interest payment in each succeeding period increased.

The example above also assumes that Sam never deposited additional money into his savings account. Had Sam deposited an additional $10,000 early on in his time horizon, the final account value would have been dramatically higher.

Related Readings

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

- Annual Percentage Rate (APR)Annual Percentage Rate (APR)The Annual Percentage Rate (APR) is the yearly rate of interest that an individual must pay on a loan, or that they receive on a deposit account. Ultimately, APR is a simple percentage term used to express the numerical amount paid by an individual or entity yearly for the privilege of borrowing money.

- Effective Annual Interest Rate CalculatorEffective Annual Interest Rate CalculatorThis effective annual interest rate calculator helps you calculate the EAR given the nominal interest rate and number of compounding periods. The Effective Annual Rate (EAR) is the rate of interest actually earned on an investment or paid on a loan as a result of compounding the interest over a given period of time. It

- Floating Interest RateFloating Interest RateA floating interest rate refers to a variable interest rate that changes over the duration of the debt obligation. It is the opposite of a fixed rate.

- Simple InterestSimple InterestSimple interest formula, definition and example. Simple interest is a calculation of interest that doesn't take into account the effect of compounding. In many cases, interest compounds with each designated period of a loan, but in the case of simple interest, it does not. The calculation of simple interest is equal to the principal amount multiplied by the interest rate, multiplied by the number of periods.

-

Assumable Mortgages: A Comprehensive Guide

An assumable mortgage is a mortgage that can be transferred from the current owner of the property to the buyer, with the terms that were agreed upon originally. In other words, the buyer is able to &

-

Bullet Loan Explained: Structure, Risks & Benefits

A bullet loan is a type of loan in which the principal that is borrowed is paid back at the end of the loan term. In some cases, the interest expenseInterest ExpenseInterest expense arises out of a co

finance

- Compound Interest Explained: How to Grow Your Wealth

- Understanding Add-On Interest: How It Works & Loan Payments

- Compound Interest Formula: Calculate & Understand Growth

- Understanding Interest: Costs & Rewards of Borrowing and Lending

- Understanding Interest Income: A Comprehensive Guide

- Understanding Interest Rates: A Comprehensive Guide

- Simple vs. Compound Interest: Understanding the Difference

- Compound Interest: Understand the Power of Exponential Growth

- Compound Interest Explained: How It Works & Benefits

-

Accrued vs. Regular Interest: Understanding the Difference

Accrued vs. Regular Interest: Understanding the DifferenceWhen investing in stocks and bonds, investors are paid either an accrued interest vs regular interest at an agreed period. The interest payments are not paid immediately, and security issuers will owe...

-

Compound (COMP): Earn & Borrow Crypto - A Comprehensive Guide

Compound (COMP): Earn & Borrow Crypto - A Comprehensive GuideTrading crypto need not be limited to just buying and selling bitcoin. For the past few years, developers have been busy creating sophisticated financial products that let you do far more. Compound is...