Incremental Budgeting: Definition, Pros & Cons | [Your Company Name]

Incremental budgeting is a type of a budgeting process that is based on the idea that a new budget can best be developed by making only some marginal changes to the current budget. In other words, with incremental budgeting, the current budget is used as a base to which incremental assumptions are added or subtracted from the base amounts to determine new budget amounts. Among all budgeting methodsTypes of BudgetsThere are four common types of budgeting methods that companies use: (1) incremental, (2) activity-based, (3) value proposition, and (4), incremental budgeting is commonly considered as the most conservative approach.

![Incremental Budgeting: Definition, Pros & Cons | [Your Company Name]](https://www.etffin.com/Article/UploadFiles/202110/2021100815150282.jpeg)

Note that there is no standard formula to determine the applicable marginal changes in the budgeting process. The marginal changes are typically determined using certain assumptions that are based on previous budgeting and expenses.

Advantages of Incremental Budgeting

Incremental budgeting can be appealing to companies for a number of reasons, including:

1. Simplicity

Incremental budgeting is the easiest budgeting approach. Since it uses the budget for the current period to project the future budget, it does not require complex calculationsTop 8 Financial CalculatorsFinancial calculators are a type of electronic calculators used in computing financial functions that regular calculators cannot handle. Some of the. Also, only a few assumptions are required in the budgeting method. Finally, the method’s simplicity allows the company’s management to save time on the budgeting process.

2. Consistency and operational stability

The dependence on the figures from the budgets of previous periods ensures that the budgets remain fairly consistent and relatively stable over time.

3. Funding stability

Incremental budgeting may also help ensure that funding remains stable over time, as expenses are relatively easy to project. This can be helpful for companies with projectsProject ManagementProject management is designed to produce an end product that will make an impact on an organization. It is where knowledge, skills, experience, and that require funding for multiple years.

4. Reduces internal rivalry

Incremental budgeting generally allocates equal incremental changes to the budget from one year to the next. Thus, departments within a company are not forced into a position of competing with each other to obtain a larger portion of the budget.

Disadvantages

Despite its simplicity and consistency, incremental budgeting is frequently criticized for a number of underlying flaws. The primary potential disadvantages of such a budgeting method are as follows:

1. Promotes unnecessary spending

Incremental budgeting can result in unnecessary spending for a company. The reason behind this is that the departments within a company generally tend to spend all the money that they’ve been allocated in a budget one year in order to obtain a greater amount of money in the next budgeting period. Incremental budgeting takes the position of increasing each part of the budget by a certain amount each year. However, some departments may not, in fact, need more money each year – but they will be allotted an increase anyway, simply because that’s how the budgeting process works. In this way, the budgeting process may be wasteful and less than optimally efficient.

2. Discourages innovation

This type of budgeting may discourage the production of innovative ideas and growth. Since new budgets are based on figures from previous budgets, there is a little room for the financing of completely new ideas or activities. Thus, the budgeting process discourages the implementation of new ideas and fosters a conservative business environment.

3. Fails to account for changes and external factors

The key assumption behind incremental budgets is the constant stability of the company’s operations. Therefore, the budgets are typically not responsive to potential changes that can result from unforeseen circumstances or some unanticipated factors.

4. Lacks an incentive for a comprehensive review

The stability of incremental budgets does not provide any incentives to the company’s management for reviewing its budgets with a view to realizing savings in expenditures. The lack of a review process makes budgets vulnerable to waste, inadequate assumptions, and mistakes.

Bottom line

Simplicity and consistency are the primary advantages of incremental budgeting. However, this budgeting technique can lead to adverse effects in the long term (as discussed immediately above).

The conservatism of this budgeting method, as well as its inflexibility and resulting inability to adjust to internal and external changes, imposes potentially problematic limitations on companies operating in today’s fast-paced business environment.

Generally, incremental budgeting is best applied only if you are confident that the company’s budgets will remain stable in the long term, with only minimal changes. In other cases, it is recommended to use more sophisticated budgeting techniques.

More Resources

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

- Budget HolderBudget HolderThe person who is ultimately responsible for ensuring that the budget is followed is known as the Budget Holder. Budget holders are usually the managers and operational directors of companies who are tasked by the owners/shareholders or the board of directors to ensure that the company follows its budget

- Capital Budgeting Best PracticesCapital Budgeting Best PracticesCapital budgeting refers to the decision-making process that companies follow with regard to which capital-intensive projects they should pursue. Such capital-intensive projects could be anything from opening a new factory to a significant workforce expansion, entering a new market, or the research and development of new products.

- Imposed BudgetingImposed BudgetingImposed budgeting, also known as top-down budgeting, is the process wherein the top management of a company prepares a budget and then imposes it on lower-level managers for implementation. It starts at the top, where the budget is prepared by senior management

- Zero-Based BudgetingZero-Based BudgetingZero-based budgeting (ZBB) is a budgeting technique that allocates funding based on efficiency and necessity rather than on budget history

-

Top-Down Budgeting: Definition, Advantages & Disadvantages

Top-down budgeting refers to a budgeting method where senior managementCorporate StructureCorporate structure refers to the organization of different departments or business units within a company. De

-

Personal Budgeting: A Beginner's Guide to Financial Control

Mastering personal finance is like learning any new skill. It takes time, practice, and patience. Most people who start caring about personal finance realize that they’ve made a few financial mistakes

finance

- Activity-Based Budgeting (ABB): A Comprehensive Guide

- Beyond Budgeting: A Modern Approach to Organizational Control

- Business Budgeting: A Comprehensive Guide to Planning & KPIs

- Incremental Analysis: A Comprehensive Guide for Business Decisions

- Understanding Incremental Cost: A Definition & Key Considerations

- Negotiated Budgeting: A Collaborative Approach to Financial Planning

- Budgeting Software: Types, Features & Comparison - [Year]

- Incremental Budgeting: Pros, Cons & Why It's Often Problematic

- Activity-Based Budgeting (ABB): A Comprehensive Guide

-

Output/Input Budgeting: A Comprehensive Guide

Output/Input Budgeting: A Comprehensive GuideAn output/input budget is also known as a performance budget. It is a type of budget that reflects both the funding levels (input) and the expected output from each unit of the organizationTypes of Or...

-

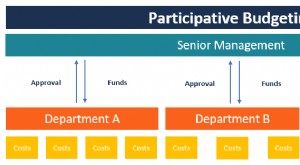

Participative Budgeting: Definition, Benefits & Implementation

Participative Budgeting: Definition, Benefits & ImplementationParticipative budgeting is a budgeting process in which the people who are in the lower levels of management are involved in the budget preparation process. Unlike the imposed budgetingImposed Budgeti...