Understanding Put-Call Parity: A Comprehensive Guide

Put-call parity is an important concept in options Options: Calls and PutsAn option is a derivative contract that gives the holder the right, but not the obligation, to buy or sell an asset by a certain date at a specified price.pricing which shows how the prices of putsPut OptionA put option is an option contract that gives the buyer the right, but not the obligation, to sell the underlying security at a specified price (also known as strike price) before or at a predetermined expiration date. It is one of the two main types of options, the other type being a call option., callsCall OptionA call option, commonly referred to as a "call," is a form of a derivatives contract that gives the call option buyer the right, but not the obligation, to buy a stock or other financial instrument at a specific price - the strike price of the option - within a specified time frame., and the underlying assetAsset ClassAn asset class is a group of similar investment vehicles. They are typically traded in the same financial markets and subject to the same rules and regulations. must be consistent with one another. This equation establishes a relationship between the price of a call and put option which have the same underlying asset. For this relationship to work, the call and put option must have an identical expiration date and strike price.

The put-call parity relationship shows that a portfolio consisting of a long Long and Short PositionsIn investing, long and short positions represent directional bets by investors that a security will either go up (when long) or down (when short). In the trading of assets, an investor can take two types of positions: long and short. An investor can either buy an asset (going long), or sell it (going short).call option and a shortLong and Short PositionsIn investing, long and short positions represent directional bets by investors that a security will either go up (when long) or down (when short). In the trading of assets, an investor can take two types of positions: long and short. An investor can either buy an asset (going long), or sell it (going short). put option should be equal to a forward contract with the same underlying asset, expiration, and strikeStrike PriceThe strike price is the price at which the holder of the option can exercise the option to buy or sell an underlying security, depending on price. This equation can be rearranged to show several alternative ways of viewing this relationship.

Quick Summary of Points

- Put-call parity is an important relationship between the prices of puts, calls, and the underlying asset

- This relationship is only true for European options with identical strike prices, maturity dates, and underlying assets (European options can only be exercised at expiration, unlike American options that can be exercised on any date up to the expiration date)

- This theory holds that simultaneously holding a short put and long call (identical strike prices and expiration) should provide the same return as one forward contract with the same expiration date as the options and where the forward price is the same as the options’ strike price

- Put-call parity can be used to identify arbitrage opportunities in the market

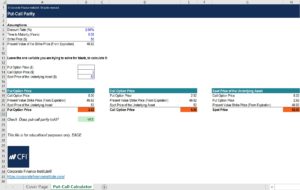

Put-Call Parity Excel Calculator

Below, we will go through an example question involving the put-call parity relationship. This can easily be done with Excel. To download the put-call parity calculator, check out CFI’s free resource: Put-Call Parity CalculatorPut-Call Parity CalculatorThis put-call parity calculator demonstrates the relationship between put options, call options, and their underlying asset.

Interpreting the Put-Call Parity

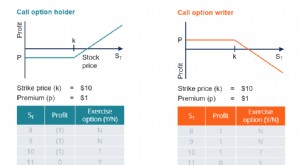

To better understand the put-call parity theory, let us consider a hypothetical situation where you buy a call optionCall OptionA call option, commonly referred to as a "call," is a form of a derivatives contract that gives the call option buyer the right, but not the obligation, to buy a stock or other financial instrument at a specific price - the strike price of the option - within a specified time frame. for $10 with a strike price of $100 and maturity date of one year, as well as sell a put optionPut OptionA put option is an option contract that gives the buyer the right, but not the obligation, to sell the underlying security at a specified price (also known as strike price) before or at a predetermined expiration date. It is one of the two main types of options, the other type being a call option. for $10 with an identical strike price and expiration. According to the put-call parity, that would be equivalent to buying the underlying asset and borrowing an amount equal to the strike price discountedDiscount RateIn corporate finance, a discount rate is the rate of return used to discount future cash flows back to their present value. This rate is often a company’s Weighted Average Cost of Capital (WACC), required rate of return, or the hurdle rate that investors expect to earn relative to the risk of the investment. to today. The spot price of the asset is $100 and we make the assumption that at the end of the year the price is $110 – so, does the put-call parity hold?

If the price goes up to $110, you would exercise the call option. You paid $10 for it but you can buy the assetAsset ClassAn asset class is a group of similar investment vehicles. They are typically traded in the same financial markets and subject to the same rules and regulations. at the strike price of $100 and sell it for $110, so you net $0. You have also sold the put option. Since the asset has increased in market value, the put option will not be exercised by the buyer and you pocket the $10. That leaves you with $10 from this portfolio.

What is the portfolio consisting of the underlying asset and short position on the strike price worth at the expiration date? Well, if you had invested in the asset at the spot priceSpot PriceThe spot price is the current market price of a security, currency, or commodity available to be bought/sold for immediate settlement. In other words, it is the price at which the sellers and buyers value an asset right now. of $100 and it ended at $110, and you had to pay back the strike price at maturity from the amount you borrowed which would be $100, the net amount would be $10. We see that these two portfolios both net to positive $10 and the put-call parity holds.

Why is the Put-Call Parity Important?

The put-call parity theory is important to understand because this relationship must hold in theory. With European put and calls, if this relationship does not hold, then that leaves an opportunity for arbitrageArbitrageArbitrage is the strategy of taking advantage of price differences in different markets for the same asset. For it to take place, there must be a situation of at least two equivalent assets with differing prices. In essence, arbitrage is a situation that a trader can profit from. Rearranging this formula, we can solve for any of the components of the equation. This allows us to create a synthetic call or put option. If a portfolio of the synthetic option costs less than the actual option, based on put-call parity, a trader could employ an arbitrage strategy to profit.

What is the Put-Call Parity Equation?

As mentioned above, the put-call parity equation can be written a number of different ways and rearranged to make varying inferences. A couple of common ways it is expressed are as follows:

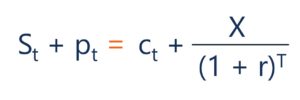

St + pt = ct + X/(1 + r)^T

The above equation shown in this combination can be interpreted as a portfolio holding a long positionLong and Short PositionsIn investing, long and short positions represent directional bets by investors that a security will either go up (when long) or down (when short). In the trading of assets, an investor can take two types of positions: long and short. An investor can either buy an asset (going long), or sell it (going short). in the underlying asset and a put option should equal a portfolio holding a long position in the call option and the strike price. According to the put-call parity this relationship should hold or else an opportunity for arbitrage would exist.

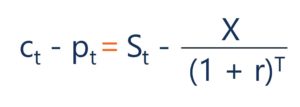

ct – pt = St – X/(1 + r)^T

In this version of the put-call parity, a portfolio that holds a long position in the call, and a short position in the put should equal a portfolio consisting of a long position in the underlying asset and a short position of the strike price.

For the above equations, the variables can be interpreted as:

- St = Spot PriceSpot PriceThe spot price is the current market price of a security, currency, or commodity available to be bought/sold for immediate settlement. In other words, it is the price at which the sellers and buyers value an asset right now. of the Underlying Asset

- pt = Put Option Price

- ct = Call Option Price

- X/(1 + r)^T = Present ValueNet Present Value (NPV)Net Present Value (NPV) is the value of all future cash flows (positive and negative) over the entire life of an investment discounted to the present. of the Strike Price, discounted from the date of expiration

- r = The Discount Rate, often the Risk-Free RateRisk-Free RateThe risk-free rate of return is the interest rate an investor can expect to earn on an investment that carries zero risk. In practice, the risk-free rate is commonly considered to equal to the interest paid on a 3-month government Treasury bill, generally the safest investment an investor can make.

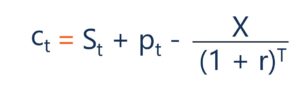

The equation can also be rearranged and solved for a specific component. For example, based on the put-call parity, a synthetic call option can be created. The following shows a synthetic call option:

ct = St + pt – X/(1 + r)^T

Here we can see that the call optionCall OptionA call option, commonly referred to as a "call," is a form of a derivatives contract that gives the call option buyer the right, but not the obligation, to buy a stock or other financial instrument at a specific price - the strike price of the option - within a specified time frame. should be equal to a portfolio with a long position on the underlying asset, a long position on the put optionPut OptionA put option is an option contract that gives the buyer the right, but not the obligation, to sell the underlying security at a specified price (also known as strike price) before or at a predetermined expiration date. It is one of the two main types of options, the other type being a call option. and a short position on the strike price. This portfolio can be thought of as a synthetic call option. If this relationship doesn’t hold, then an arbitrage opportunity exists. If the synthetic call was less than the call option, then you could buy the synthetic call and sell the actual call option to profit.

Put-Call Parity – European Call Option Example

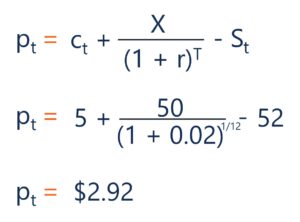

Let us now consider a question involving the put-call parity. Suppose a European call option on a barrel of crude oil with a strike price of $50 and a maturity of one-month, trades for $5. What is the price of the put premium with identical strike price and time until expiration, if the one-month risk-free rate is 2% and the spot price of the underlying asset is $52?

Here we can see the calculation that would be used to find the put premium:

These calculations can also be done in Excel. The following shows the solution to the above question done in excel:

Put-Call Parity CalculatorThis put-call parity calculator demonstrates the relationship between put options, call options, and their underlying asset.

Put-Call Parity CalculatorThis put-call parity calculator demonstrates the relationship between put options, call options, and their underlying asset.

If you would like to learn more about financial modeling, check out CFI’s Financial Modeling Courses

Additional Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Options: Calls and PutsOptions: Calls and PutsAn option is a derivative contract that gives the holder the right, but not the obligation, to buy or sell an asset by a certain date at a specified price.

- Option Pricing ModelsOption Pricing ModelsOption Pricing Models are mathematical models that use certain variables to calculate the theoretical value of an option. The theoretical value of an

- ArbitrageArbitrageArbitrage is the strategy of taking advantage of price differences in different markets for the same asset. For it to take place, there must be a situation of at least two equivalent assets with differing prices. In essence, arbitrage is a situation that a trader can profit from

- DerivativesDerivativesDerivatives are financial contracts whose value is linked to the value of an underlying asset. They are complex financial instruments that are

-

Put-Call Parity Explained: Understanding the Relationship

What Is Put-Call Parity? The term put-call parity refers to a principle that defines the relationship between the price of European put and call options of the same class. Put simply, this

-

What is a Stock Option?

A stock option is a contract between two parties that gives the buyer the right to buy or sell underlying stocksStockWhat is a stock? An individual who owns stock in a company is called a shareholder

finance

- Call Options: A Comprehensive Guide for Investors

- Understanding Delta: A Key Risk Measure in Derivatives

- Understanding Digital Options: A Comprehensive Guide for Traders

- Understanding Exercise Price in Options Trading

- Knock-In Options Explained: A Comprehensive Guide

- Knock-Out Options: A Comprehensive Guide

- Naked Options: Risks, Rewards, and How They Work

- Understanding Near-The-Money Options: A Comprehensive Guide

- Put Options Explained: A Comprehensive Guide for Investors

-

Understanding Strike Price: Options Trading Explained

Understanding Strike Price: Options Trading ExplainedThe strike price is the price at which the holder of the option can exercise the option to buy or sell an underlying security, depending on whether they hold a call optionCall OptionA call option, com...

-

Understanding Option Intrinsic Value: A Clear Explanation

Intrinsic value for call options is literally the difference between the price of the market and the strike price (or exercise price), as long as the market is above the strike price. The intrin...