ROA Calculation: Understand Return on Assets & Formula

Return on Assets (ROA) is a type of return on investment (ROI)ROI Formula (Return on Investment)Return on investment (ROI) is a financial ratio used to calculate the benefit an investor will receive in relation to their investment cost. It is most commonly measured as net income divided by the original capital cost of the investment. The higher the ratio, the greater the benefit earned. metric that measures the profitability of a business in relation to its total assetsTypes of AssetsCommon types of assets include current, non-current, physical, intangible, operating, and non-operating. Correctly identifying and. This ratio indicates how well a company is performing by comparing the profit (net incomeNet IncomeNet Income is a key line item, not only in the income statement, but in all three core financial statements. While it is arrived at through) it’s generating to the capital it’s invested in assets. The higher the return, the more productive and efficient management is in utilizing economic resources. Below you will find a breakdown of the ROA formula and calculation.

What is the ROA Formula?

The ROA formula is:

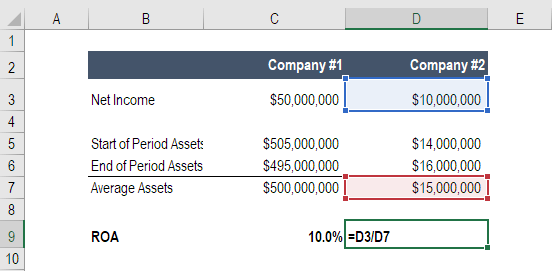

ROA = Net Income / Average Assets

or

ROA = Net Income / End of Period Assets

Where:

Net Income is equal to net earnings or net income in the year (annual period)

Average Assets is equal to ending assets minus beginning assets divided by 2

Image: CFI’s Financial Analysis Fundamentals Course.

Example of ROA Calculation

Let’s walk through an example, step by step, of how to calculate return on assets using the formula above.

Q: If a business posts a net incomeNet IncomeNet Income is a key line item, not only in the income statement, but in all three core financial statements. While it is arrived at through of $10 million in current operations, and owns $50 million worth of assets as per the balance sheetBalance SheetThe balance sheet is one of the three fundamental financial statements. The financial statements are key to both financial modeling and accounting., what is its return on assets?

A: $10 million divided by $50 million is 0.2, therefore the business’s ROA is 20%. For every dollar of assets the company invests in, it returns 20 cents in net profit per year.

Download the Free Template

Enter your name and email in the form below and download the free template now!

What is the Importance of Return on Assets?

The ROA formula is an important ratio in analyzing a company’s profitabilityProfitability RatiosProfitability ratios are financial metrics used by analysts and investors to measure and evaluate the ability of a company to generate income (profit) relative to revenue, balance sheet assets, operating costs, and shareholders' equity during a specific period of time. They show how well a company utilizes its assets to produce profit. The ratio is typically used when comparing a company’s performance between periods, or when comparing two different companies of similar size in the same industry. Note that it is very important to consider the scale of a business and the operations performed when comparing two different firms using ROA.

Typically, different industries have different ROA’s. Industries that are capital-intensive and require a high value of fixed assetsFixed Asset TurnoverFixed Asset Turnover (FAT) is an efficiency ratio that indicates how well or efficiently the business uses fixed assets to generate sales. This ratio divides net sales into net fixed assets, over an annual period. The net fixed assets include the amount of property, plant, and equipment less accumulated depreciation for operations, will generally have a lower ROA, as their large asset base will increase the denominator of the formula. Naturally, a company with a large asset base can have a large ROA, if their income is high enough.

What is Net Income?

Net income is the net amount realized by a firm after deducting all the costs of doing business in a given period. It includes all interest paid on debt, income tax due to the government, and all operational and non-operational expenses.

Operational costs can include cost of goods sold (COGS)Cost of Goods Sold (COGS)Cost of Goods Sold (COGS) measures the “direct cost” incurred in the production of any goods or services. It includes material cost, direct, production overhead, administrative and marketing expenses, and amortization and depreciation of equipment and property.

Also added into net income is the additional income arising from investments or those that are not directly resulting from primary operations, such as proceeds from the sale of equipment or fixed assets. Note: non-operating items may be adjusted out of net income by a financial analystBecome a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today!.

Net income/loss is found at the bottom of the income statement and divided into total assets to arrive at ROA.

Video Example of Return on Assets in Financial Analysis

ROA is commonly used by analysts performing financial analysisAnalysis of Financial StatementsHow to perform Analysis of Financial Statements. This guide will teach you to perform financial statement analysis of the income statement, of a company’s performance.

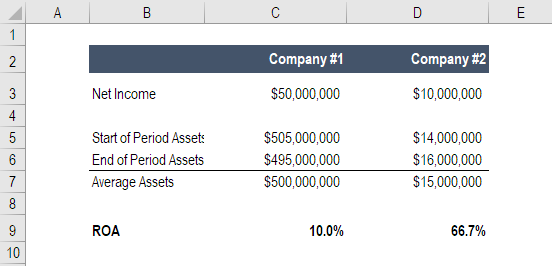

ROA is important because it makes companies more easily comparable. Imagine two companies… one with a net income of $50 million and assets of $500 million, the other with a net income of $10 million and assets of $15 million.

Which company would you rather own?

The first company earns a return on assets of 10% and the second one earns an ROA of 67%.

Watch more in CFI’s Financial Analysis Fundamentals Course.

Return on Assets for Companies

Below are some examples of the most common reasons companies perform an analysis of their return on assets.

1. Using ROA to determine profitability and efficiency

Return on assets indicates the amount of money earned per dollar of assets. Therefore, a higher return on assets value indicates that a business is more profitable and efficient.

2. Using ROA to compare performance between companies

It is important to note that return on assets should not be compared across industries. Companies in different industries vary significantly in their use of assets. For example, some industries may require expensive property, plant, and equipment (PP&E)PP&E (Property, Plant and Equipment)PP&E (Property, Plant, and Equipment) is one of the core non-current assets found on the balance sheet. PP&E is impacted by Capex, to generate income as opposed to companies in other industries. Therefore, these companies would naturally report a lower return on assets when compared to companies that do not require a lot of assets to operate. Therefore, return on assets should only be used to compare with companies within an industry. Learn more about industry analysisIndustry AnalysisIndustry analysis is a market assessment tool used by businesses and analysts to understand the complexity of an industry. There are three commonly used and.

3. Using ROA to determine asset-intensive/asset-light companies

Return on assets can be used to gauge how asset-intensive a company is:

- The lower the return on assets, the more asset-intensive a company is. An example of an asset-intensive company would be an airline company.

- The higher the return on assets, the less asset-intensive a company is. An example of an asset-light company would be a software company.

As a general rule, a return on assets under 5% is considered an asset-intensive business while a return on assets above 20% is considered an asset-light business.

Additional Resources

Thanks for reading CFI’s guide to return on assets and the ROA formula. To keep learning and become a world-class financial analystThe Analyst Trifecta® GuideThe ultimate guide on how to be a world-class financial analyst. Do you want to be a world-class financial analyst? Are you looking to follow industry-leading best practices and stand out from the crowd? Our process, called The Analyst Trifecta® consists of analytics, presentation & soft skills, these additional CFI resources will be a big help:

- Internal Rate of ReturnInternal Rate of Return (IRR)The Internal Rate of Return (IRR) is the discount rate that makes the net present value (NPV) of a project zero. In other words, it is the expected compound annual rate of return that will be earned on a project or investment.

- Return on EquityReturn on Equity (ROE)Return on Equity (ROE) is a measure of a company’s profitability that takes a company’s annual return (net income) divided by the value of its total shareholders' equity (i.e. 12%). ROE combines the income statement and the balance sheet as the net income or profit is compared to the shareholders’ equity.

- DCF Modeling GuideDCF Model Training Free GuideA DCF model is a specific type of financial model used to value a business. The model is simply a forecast of a company’s unlevered free cash flow

- Financial Modeling Best PracticesFree Financial Modeling GuideThis financial modeling guide covers Excel tips and best practices on assumptions, drivers, forecasting, linking the three statements, DCF analysis, more

-

Calculate Rate of Return: Formulas & Investment Performance

How to Calculate the Rate of Return With a Formula All investors hope to make money on their investment, expressed as a "gain." But you don't have to be a big player in the stoc

-

Understanding the Return on Assets (ROA) Ratio: A Comprehensive Guide

The return on assets ratio (ROA) for any individual company shows how effectively it has turned its investments into profits. The model uses the simple formula of net income divided by total ass

finance

- Understanding Net Foreign Assets (NFA): A Comprehensive Guide

- Net Liquid Assets: Definition, Calculation & Importance

- Operating Return on Assets (OROA): Definition & Calculation

- Return on Net Assets (RONA): Definition & Significance

- Understanding Unrestricted Net Assets for Nonprofits

- Understanding the Limitations of Return on Assets (ROA)

- Return on Assets (ROA): Calculation & Interpretation

- Return on Net Assets (RONA): Definition & Analysis

- Internal Rate of Return (IRR) Calculation: A Practical Guide

-

ROI Calculation: A Simple Formula for Investment Returns

ROI Calculation: A Simple Formula for Investment ReturnsCalculating return on investment using a formula Return on investment shows how much money is made on an investment compared to how much was spent on it. It is expressed as a percentage. The ...

-

Net Worth Calculator: A Step-by-Step Guide to Financial Health

Calculating your net worth is a multi-step process. Before you start, decide if you want to calculate net worth individually (you) or jointly (you and your spouse/partner). Also, get all your financia...