Operating Return on Assets (OROA): Definition & Calculation

Operating return on assets (OROA), an efficiency or profitability ratioProfitability RatiosProfitability ratios are financial metrics used by analysts and investors to measure and evaluate the ability of a company to generate income (profit) relative to revenue, balance sheet assets, operating costs, and shareholders' equity during a specific period of time. They show how well a company utilizes its assets to produce profit, is a variation of the traditional return on assets ratio. Operating return on assets is used to show a company’s operating income that is generated per dollar invested specifically in its assets that are used in its everyday business operations. Like the return on assets ratio, OROA measures the level of profits relative to the company’s assets, but using a narrower definition of its assets.

Formula for Operating Return on Assets

The formula for the operating return on assets ratio is as follows:

Where:

- Earnings before interest and taxesEBIT GuideEBIT stands for Earnings Before Interest and Taxes and is one of the last subtotals in the income statement before net income. EBIT is also sometimes referred to as operating income and is called this because it's found by deducting all operating expenses (production and non-production costs) from sales revenue. (EBIT) is equivalent to operating income.

- Average total assets is the average of beginning and ending values of the company’s assets used in its normal business activities.

The formula differs from the formula for the regular return on assets ratio as follows:

1) It uses EBIT rather than net income as the numerator.

2) It uses regular business operations assets rather than total assets as the denominator.

Example of Operating Return on Assets

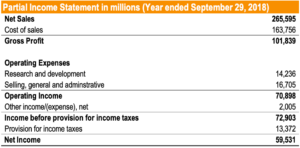

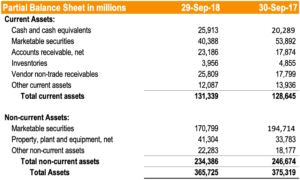

Tim is an equity analyst looking to determine the profitability of Apple Inc. Among other ratios that Tim uses, he decides to also use the OROA to determine the level of profits relative to Apple’s operating assets. He compiles the following information from Apple’s 2018 annual report:

Tim calculates Apple’s OROA for the year ended September 29, 2018, as follows:

Tim concludes that Apple generated $0.1913 in operating income per dollar of operating assets.

Benefits of Using Operating Return on Assets

Similar to the traditional return on assets, the operating return on assets is used to determine the effectiveness of business operations and the profitability generated from assets used. The OROA is commonly used by analysts and investors who want to disregard the cost of asset acquisition that can come in the form of debt (i.e., interest expenseInterest ExpenseInterest expense arises out of a company that finances through debt or capital leases. Interest is found in the income statement, but can also) or equity and the effect of taxes (which may vary across countries).

There is no “perfect” OROA – the ratio should be compared relative to competitors. With that said, a higher OROA is desirable.

The OROA can be used:

- To compare how well a company utilizes its assets among companies that operate in the same industry and are engaged in similar business operations;

- On a trended basis to compare its current performance to its performance in the previous year

- To indicate how well a company is using its assets to generate operating income.

Key Takeaways

Operating return on assets (OROA) is similar to the traditional return on assetsReturn on Assets & ROA FormulaROA Formula. Return on Assets (ROA) is a type of return on investment (ROI) metric that measures the profitability of a business in relation to its total assets. ratio but uses operating income in the numerator as opposed to net income. OROA is used to determine a company’s operating efficiency by revealing the amount of income generated per dollar invested in its operating assets. It excludes assets that are not part of its normal business operations – such as investments in other companies that it may hold.

The OROA can be used to compare with peer companies, used to determine the trend of company performance, and as an indicator of how well a company is using its assets to generate operating income.

More Resources

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

- Non-Operating AssetsNon-Operating AssetsNon-operating assets are assets that are not required in the normal operations of a business but that can generate income nonetheless. The assets are recorded in the balance sheet and may be listed separately or as part of operating assets. Non-operating assets may be investments or assets that can be disposed of to generate income

- Operating IncomeOperating IncomeOperating income is the amount of revenue left after deducting the operational direct and indirect costs from sales revenue.

- Return on Net Assets (RONA)Return on Net Assets (RONA)The return on net assets (RONA) ratio, a measure of financial performance, is an alternative metric to the traditional return on assets ratio. RONA measures how well a company’s fixed assets and net working capital perform in terms of generating net income. Return on net assets is commonly used for capital-intensive companies

- Types of AssetsTypes of AssetsCommon types of assets include current, non-current, physical, intangible, operating, and non-operating. Correctly identifying and

-

Operating Ratio: Definition, Calculation & Importance

The operating ratio is a measure of efficiency that is used by management to determine day-to-day operational performance. This metric compares operating expenses, also known as OPEX, to net sales. Th

-

Understanding Quick Assets: Definition & Examples

Quick assets are those assets that can be converted into cash within a short period of time. The term is also used to refer to assets that are already in cash form. They are considered to be the most

finance

- Understanding Alpha: A Guide to Investment Performance

- Asset Management: Definition, Types & Importance

- Cash-on-Cash Return: Definition, Calculation & Importance

- Operating Asset Turnover Ratio: Definition & Analysis

- Operating Return on Assets (OROA): Definition & Calculation

- Understanding Operating Risk: A Key Component of Business Risk

- Understanding Rate of Return: A Comprehensive Guide

- Return on Net Assets (RONA): Definition & Significance

- Return on Ad Spend (ROAS): Definition & Importance for eCommerce

-

Understanding Non-Monetary Assets: Definition & Examples

Understanding Non-Monetary Assets: Definition & ExamplesNon-monetary assets are assets whose value frequently changes in response to changes in economic and market conditions. The assets appear on the balance sheet under intangible and non-current assetsNo...

-

![Operating Profit Margin: Definition & Calculation | [Your Company Name]](https://www.etffin.com/article/uploadfiles/202110/2021100815165062_S.png) Operating Profit Margin: Definition & Calculation | [Your Company Name]

Operating Profit Margin: Definition & Calculation | [Your Company Name]Operating Profit Margin is a profitability or performance ratio that reflects the percentage of profit a company produces from its operations, prior to subtracting taxes and interest charges. It is ca...