Understanding American Depositary Receipts (ADRs): A Comprehensive Guide

American Depositary Receipts (ADR) are negotiable security instruments that are issued by a US bankTop Banks in the USAAccording to the US Federal Deposit Insurance Corporation, there were 6,799 FDIC-insured commercial banks in the USA as of February 2014. that represent a specific number of shares in a foreign company that is traded in US financial marketsPrimary MarketThe primary market is the financial market where new securities are issued and become available for trading by individuals and institutions. The trading activities of the capital markets are separated into the primary market and secondary market.. ADRs pay dividends in US dollars and trade like regular shares of stockStockWhat is a stock? An individual who owns stock in a company is called a shareholder and is eligible to claim part of the company’s residual assets and earnings (should the company ever be dissolved). The terms "stock", "shares", and "equity" are used interchangeably.. Companies can now purchase stocks of foreign companies in bulk and reissue them on the US market. ADRs are listed on the NYSE, NASDAQ, AMEX and can be sold over-the-counter.

Before the introduction of ADRs in 1927, investors in the US faced numerous hurdles when attempting to invest in stocks of foreign companies. American investors could purchase the shares on international exchanges only, and that meant dealing with currency exchange rates and regulatory differences in foreign jurisdictions. They needed to familiarize themselves with different rules and risks related to investing in companies without a US presence. However, with ADRs, investors can diversify their portfolio by investing in foreign companies without having to open a foreign brokerage account.

How American Depositary Receipts Work

Investors willing to invest in American Depositary Receipts can purchase them from brokers or dealers. The brokers and dealers obtain ADRs by buying already-issued ADRs in the US financial markets or by creating a new ADR. Already-issued ADR can be obtained from the NASDAQ or NYSE.

Creating a new ADR involves buying the stocks of the foreign company in the issuer’s home market and depositing the acquired shares in a depository bank in the overseas market. The bank then issues ADRs that are equal to the value of the shares deposited with the bank, and the dealer/broker takes the ADR to US financial markets to sell them. The decision to create an ADR depends on the pricing, availability, and demand.

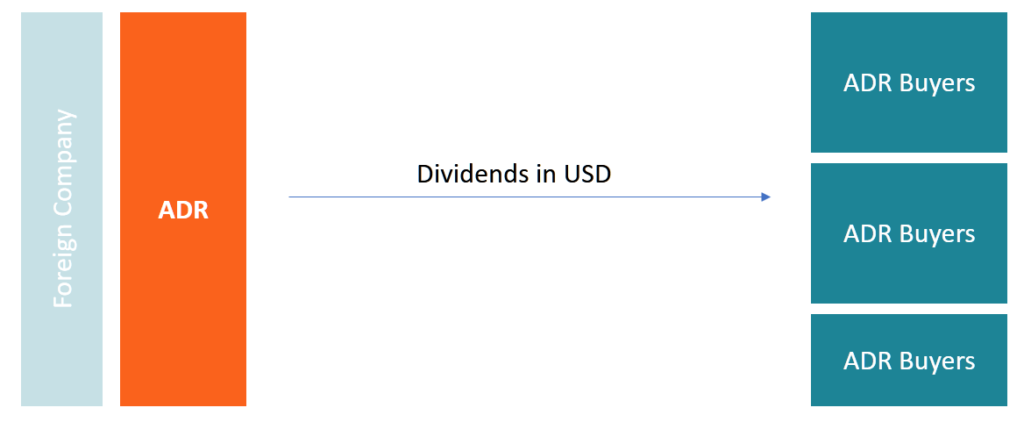

Investors who purchase the ADRs are paid dividends in US dollars. The foreign bank pays dividends in the native currency, and the dealer/broker distributes the dividends in US dollars after factoring in currency conversion costs and foreign taxes. This makes it easy for US investors to invest in a foreign company without worrying about currency exchange rates. The US banks that deal with ADRs require the foreign companies to furnish them with their financial information, which investors use to determine the company’s financial health.

Types of American Depositary Receipts

The ADRs that are sold in US financial markets can be categorized into sponsored and unsponsored.

1. Sponsored ADR

For a sponsored ADR, the foreign company issuing shares to the public enters into an agreement with a US depositary bank to sell its shares in US markets. The US bank is responsible for recordkeeping, sale, and distribution of shares to the public, distribution of dividends, etc. Sponsored ADRs can be listed on the US stock exchanges.

2. Non-Sponsored ADR

A non-sponsored ADR is created by brokers/dealers without the cooperation of the foreign company issuing the shares. Non-sponsored ADRs are traded in US over-the-counter markets without requiring registration with the Securities and Exchange Commission (SEC). Before 2008, any brokers and dealers trading in ADRs were required to submit a written application before being allowed to trade in the US. The 2008 SEC amendment provided an exemption to foreign issuers that met certain regulatory conditions. Non-sponsored ADRs are only traded on over-the-counter markets.

Levels of American Depositary Receipts

ADRs are grouped into three levels depending on the extent of the foreign company’s access to the US trading market.

1. Sponsored Level I

Level I is the lowest level at which sponsored ADRs can be issued. It is the most common level for foreign companies that do not qualify for other levels or that do not want their securities listed on US exchanges. Level I ADRs are subject to the least reporting requirements with the Securities and Exchange Commission, and they are only traded over the counter. The companies are not required to issue quarterly or annual reports like other publicly traded companies. However, Level I issuers must have their stock listed on one or more exchanges in the country of origin. Level I can be upgraded to Level II when the company is ready to sell through US exchanges.

2. Sponsored Level II ADRs

Level II ADRs have more requirements from the SEC than Level I, and the company gets an opportunity to establish a higher trading presence on the US stock markets. The company must file a registration statement with the SEC. Also, the company must file Form-20-F in accordance with the GAAP or IFRS standards. Form 20-F is the equivalent of Form-10-K, which is submitted by US publicly traded companies. If the issuer fails to comply with these requirements, it may be delisted or downgraded to Level I.

3. Sponsored Level III ADRs

Level III is the highest and most prestigious level that a foreign company can sponsor. A foreign company at this level can float a public offering of ADRs to raise capital from American investors through US exchanges. Level III ADRs also attract stricter regulations from the SEC. The company must file Form F-1 (prospectus) and Form 20-F (annual reports) in accordance with GAAP or IFRS standards. Any materials distributed to shareholders in the issuer’s home country must be submitted to the SEC as Form 6-K. Examples of foreign companies that have managed to enter this ADR level include Vodafone, Petrobras, and China Information Technology.

Termination or Cancellation

ADRs are subject to cancellation at the discretion of either the foreign issuer or the depositary bank that created them. The termination results in the cancellation of all ADRs issued and delisting from the US exchange markets where the foreign stock was trading. Before the termination, the company must write to the owners of ADRs, giving them the option to swap their ADR for foreign securities represented by the receipts.

If the owners take possession of the foreign securities, they can look for brokers who trade in that specific foreign market. If the owner decides to hold onto their ADR certificates after the termination, the depositary bank will continue holding onto the foreign securities and collect dividends but will not sell more ADR securities.

More Resources

Thank you for reading CFI’s explanation of American Depositary Receipts. CFI is the official global provider of the Financial Modeling and Valuation Analyst (FMVA)®Become a Certified Financial Modeling & Valuation Analyst (FMVA)®CFI's Financial Modeling and Valuation Analyst (FMVA)® certification will help you gain the confidence you need in your finance career. Enroll today! designation, a leading financial analyst certification program. To continue learning and advancing your career, these additional resources will be helpful:

- Marketable SecuritiesMarketable SecuritiesMarketable securities are unrestricted short-term financial instruments that are issued either for equity securities or for debt securities of a publicly listed company. The issuing company creates these instruments for the express purpose of raising funds to further finance business activities and expansion.

- Equity Capital MarketsEquity Capital Market (ECM)The equity capital market is a subset of the capital market, where financial institutions and companies interact to trade financial instruments

- Types of Markets – Dealers, Brokers, ExchangesTypes of Markets - Dealers, Brokers, ExchangesMarkets include brokers, dealers, and exchange markets. Each market operates under different trading mechanisms, which affect liquidity and control. The different types of markets allow for different trading characteristics, outlined in this guide

- Trading MechanismsTrading MechanismsTrading mechanisms refer to the different methods by which assets are traded. The two main types of trading mechanisms are quote driven and order driven trading mechanisms

-

Income Stocks: A Guide to Dividend Investing

Income stocks are equity financial securities that pay regular and predictable dividendsDividendA dividend is a share of profits and retained earnings that a company pays out to its shareholders. When

-

Investment-Grade Bonds: Understanding Credit Risk & Ratings

An investment-grade bond is a bond classification used to denote bonds that carry a relatively low credit riskCredit RiskCredit risk is the risk of loss that may occur from the failure of any party to

invest

- American Depositary Shares (ADS): A Comprehensive Guide

- American, European, & Bermudan Options: A Comprehensive Comparison

- Baby Bonds: A Comprehensive Guide to Investing in Children's Futures

- Understanding Bonds: A Comprehensive Guide for Investors

- Understanding Commodities: A Beginner's Guide to Investing

- Defensive Industries: Stability in Economic Uncertainty | [Your Company Name]

- Understanding American Depository Receipts (ADRs) | Investment Guide

- American Depositary Receipts (ADRs): A Beginner's Guide

- Understanding American Depositary Receipts (ADRs): A Beginner's Guide

-

Understanding Hard Assets: Definition, Examples & Investment

Understanding Hard Assets: Definition, Examples & InvestmentHard assets are physical or tangible assets that hold value and are normally held for the long term. In addition to tangibility, they are also visible and are considered an investable asset because of...

-

Understanding Historical Returns: A Guide for Investors

Understanding Historical Returns: A Guide for InvestorsThe historical return of a financial asset, such as a bond, stock, security, index, or fund, is its past rate of return and performance. The historical data is commonly used in financial analysisTypes...