Annuity Tables: Understanding Present & Future Value

An annuity table is a method that helps in understanding the worth of an annuity. It calculates the present value and future value of the annuity, considering the value and the time period of the investment. The table helps an investor in making informed decisions while planning for investments.

Annuities are either lump-sum payments or multiple payments made at regular intervals. The deposits made to savings accountsSavings AccountA savings account is a typical account at a bank or a credit union that allows an individual to deposit, secure, or withdraw money when the need arises. A savings account usually pays some interest on deposits, although the rate is quite low., monthly rent payments, and retirement pensions are considered annuities. The payments received from an annuity are reported as income, and the amount of tax to be paid depends on the product.

Summary

- An annuity table aids in finding out the present and future values of a sequence of payments made or received at regular intervals.

- It helps an investor to make informed decisions regarding investment planning.

- An annuity table cannot be used for non-discrete interest rates and time periods.

Annuity Table and the Worth of an Annuity

The annuity table consists of a factor specific to the series of payments an investor is expecting to receive at regular intervals and a particular interest rate. The number of payments is on the y-axis, and the rate of interest, or the discount rateDiscount RateIn corporate finance, a discount rate is the rate of return used to discount future cash flows back to their present value. This rate is often a company’s Weighted Average Cost of Capital (WACC), required rate of return, or the hurdle rate that investors expect to earn relative to the risk of the investment., is on the x-axis. The intersection of the number of payments and the discount rate presents a factor that is multiplied by the value of payments, providing the present value of the annuity.

One can also determine the future value of a series of investments using the respective annuity table. For example, the annuity table can be used to determine the present value of the annuity that is expected to make eight payments of $15,000 at a 6% interest rate, as well as the value of the payments on of a future date.

Present Value of Annuity, Future Value of Annuity, and the Annuity Table

The annuity table provides a quick way to find out the present and final values of annuities. However, the table works for discrete values only. However, in the real world, interest ratesInterest RateAn interest rate refers to the amount charged by a lender to a borrower for any form of debt given, generally expressed as a percentage of the principal. and time periods are not always discrete. Therefore, there are certain formulas to compute the present value and future value of annuities.

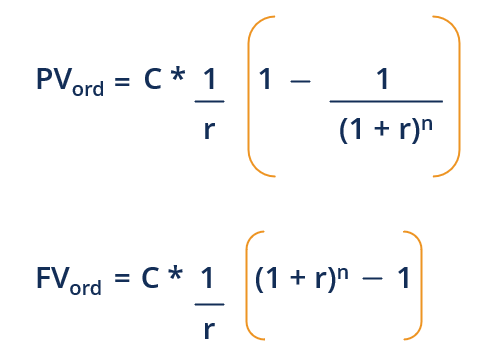

1. Regular annuity

A regular annuity is where the regular payments are required or made at the end of a period for a specific length of time. The present and future values of an annuity can be calculated as:

Where:

- PVord – Present value of ordinary annuity

- FVord – Future value of ordinary annuity

- C – Cash flows, which are annuity payments in this case

- r – Interest rate

- n – Number of periods for which payments are to be made or required

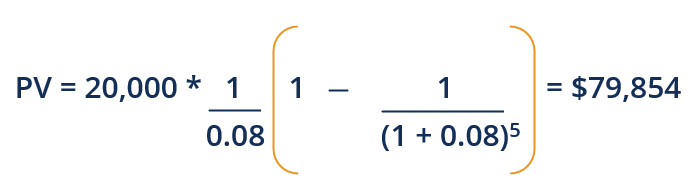

Assume that you are offered an annuity that pays $20,000 at the end of each year for five years at an 8% interest rate, or you can receive a lump-sum amount of $75,000 today. Which option is better?

To compare both options, let’s find out the present value of the annuity.

Here, the annuity value is higher; hence, it would be reasonable to choose the annuity over the lump-sum amount.

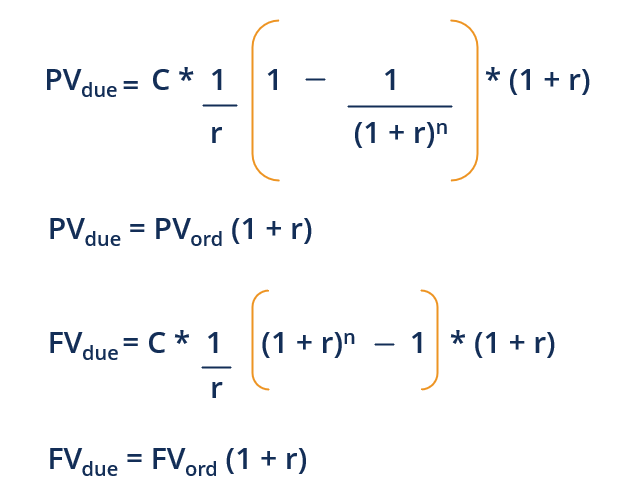

2. Annuity due

If regular payments are made or required at the beginning of each period for a certain length of time, the annuity is called an annuity due. The present and future values of an annuity due can be computed as follows:

Where:

- PVdue – Present value of annuity due

- FVdue – Future value of annuity due

Assume that in the example above, the annuity payment is to be received at the beginning of each year. Then, the present value of the annuity will be:

PVdue = PVord (1 + r)

PVdue = 79,854 (1 + 0.08)

PVdue = $86,242

The annuity due value is greater; hence, you should choose the annuity due over the lump-sum payment. In case you are given an option to choose between the two types of annuities, you should choose annuity due, as its value is more than the ordinary annuity.

More Resources

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™Program Page - CBCAGet CFI's CBCA™ certification and become a Commercial Banking & Credit Analyst. Enroll and advance your career with our certification programs and courses. certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

- Amortization ScheduleAmortization ScheduleAn amortization schedule is a table that provides the details of the periodic payments for an amortizing loan. The principal of an amortizing loan is paid

- Annuity DueAnnuity DueAnnuity due refers to a series of equal payments made at the same interval at the beginning of each period. Periods can be monthly, quarterly,

- Checking Accounts vs. Savings AccountsChecking Accounts vs Savings AccountsA bank client can choose to open checking accounts vs savings accounts depending on several factors, such as purpose, ease of access, or other attributes. A checking account is a type of bank account that is used for everyday transactions. It is the most basic account that banks, credit unions, and small lenders offer.

- Pension FundPension FundA pension fund is a fund that accumulates capital to be paid out as a pension for employees when they retire at the end of their careers.

-

Value Engineering: Definition, Benefits & Implementation

Value engineering refers to the systematic method of improving the value of a product that a project produces. It is used to analyze a service, system, or product to determine the best way to manage t

-

Value Proposition: Definition, Examples & How to Create One

A value proposition is a promise of value stated by a company that summarizes how the benefit of the company’s product or service will be delivered, experienced, and acquired. Essentially, a val

invest

- Commercial Annuities: Understanding Contracts & Payments

- Annuity Factor: Definition, Calculation & Uses

- Federal Annuities: A Comprehensive Overview for Qualified Individuals

- Annuity Due Explained: Payments at the Beginning of Each Period

- Understanding Financial Denomination: A Comprehensive Guide

- Ex-Post Analysis: Understanding Outcomes After Events

- Value at Risk (VaR): Understanding Investment Risk

- Value Investing: A Comprehensive Guide to Finding Undervalued Investments

- Annuities Explained: A Simple Guide to Retirement Income

-

What is Value Date?

What is Value Date?Value date refers to the date when a transaction takes place or when the value of assets or money becomes effective. it is also used to determine the present value of a product with a fluctuating pric...

-

Par Value Explained: Understanding Bonds & Stocks

Par Value Explained: Understanding Bonds & StocksPar value is the nominal or face value of a bond, share of stock, or coupon as indicated on a bond or stock certificate. The certificate is issued by the lender and given to a borrower or by a corpora...