Understanding Imputed Interest: Definition & Tax Implications

Imputed interest is the interest that is estimated to be collected by the lender, regardless of what the lender actually receives. Tax collection agencies use imputed interest to collect tax revenue on below-market loans and zero-coupon bondsZero-Coupon BondA zero-coupon bond is a bond that pays no interest and trades at a discount to its face value. It is also called a pure discount bond or deep discount bond..

Summary

- Imputed interest is the interest estimated to be collected by the lender, regardless of what the lender actually receives. The tax collection agency uses the imputed interest to collect tax revenue on below-market loans and zero-coupon bonds.

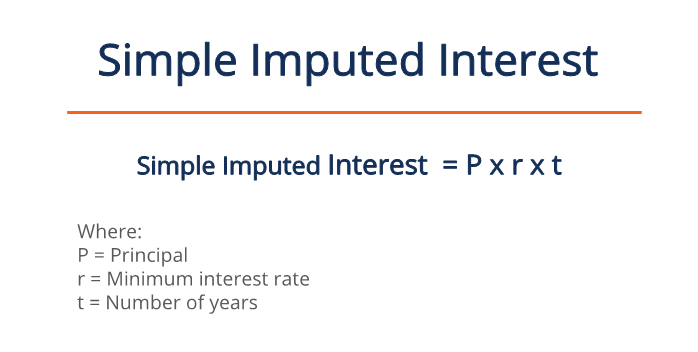

- For below-market loans, imputed interest is calculated using the minimum interest rate.

- For zero-coupon bonds, the imputed interest is calculated as accrued interest based on the yield to maturity.

Calculating Imputed Interest

Tax Implications – Base Scenario

Generally, lenders must report interest incomeInterest IncomeInterest income is the amount paid to an entity for lending its money or letting another entity use its funds. On a larger scale, interest income is the amount earned by an investor’s money that he places in an investment or project. made on their loans to be taxed. For example, consider a scenario whereby a lender loans out $50,000 at an annual rate of 2% with a maturity of one year. The lender receives 50,000 x 0.02 x 1 = $1,000 in interest income to be declared on their tax return.

There are two scenarios in which imputed interest applies:

1. Below-Market Loans

Below-market loans occur when lenders charge below the minimum interest rate, most common in cases of lending to friends and family. The minimum interest rate for private loans is determined on a quarterly basis by the tax collection agency.

In Canada, the Canadian Revenue Agency (CRA) sets the prescribed interest rate, and in the United States, the Internal Revenue Services (IRS) sets the applicable federal rate (AFR). The minimum interest rate is closely related to the treasury yield. For below-market loans, lenders are taxed on the minimum interest rate even if they do not receive interest.

For example, an aunt lends her nephew $100,000 for three years with no interest. At the time, the prescribed rate is 1.5%. Despite the aunt not receiving any interest, she must report interest income of 100,000 x 0.015 = $1,500 of imputed interest on each tax return for the three years the loan was outstanding.

2. Zero-Coupon Bonds

Zero-coupon bonds are bonds that pay no interest over the duration, only a lump sum at maturity. Lenders make a profit because zero-coupon bonds are sold at a discount to the face valueFace ValueThe value mentioned on an instrument like a coin, stamp, or bill is called the face value of the instrument. It always remains constant. It means that at any point before maturity, the bond is sold for less than the lump sum received at maturity.

As time passes, the bond increases in value due to accrued interest until it reaches face value at maturity. Zero-coupon bondholders can sell the bond on the secondary market before it matures; the longer they hold the bond, the more they can sell it. In filing tax returns, zero-coupon bonds are required to declare the imputed interest.

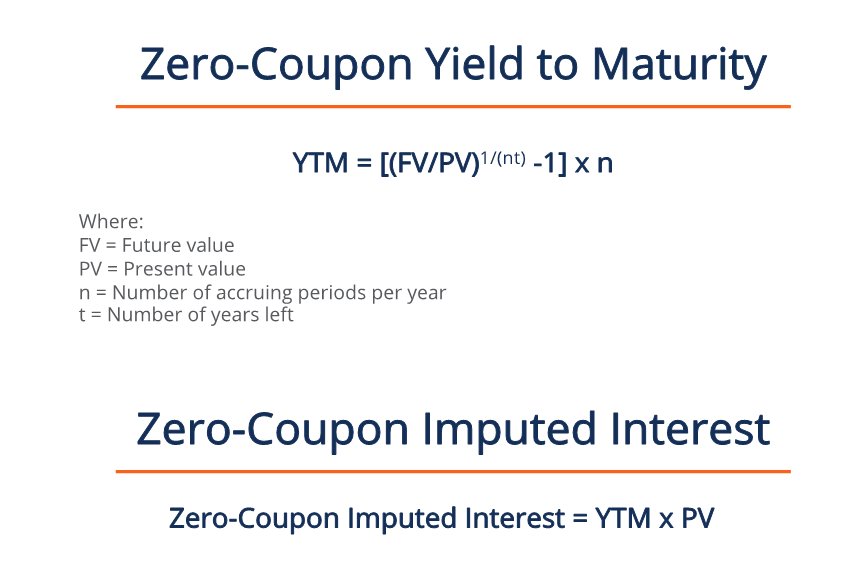

The imputed interest for the year on zero-coupon bonds is estimated as the accrued interest rather than the minimum interest like in below-market loans. It is calculated as the yield to maturity (YTM)Yield to Maturity (YTM)Yield to Maturity (YTM) – otherwise referred to as redemption or book yield – is the speculative rate of return or interest rate of a fixed-rate security. multiplied by the present value of the bond. The value of the bond at any point in time depends on the amount of time left until maturity, calculated as the starting value of the loan plus accrued interest.

For example, a borrower issues a zero-coupon bond at a discount of $2,500 with a face value of $10,000, quarterly accruals, and a maturity of two years. At inception, the lender purchases the bond for $7,500, and in two years’ time, they will receive a lump sum of $10,000.

The YTM on the bond at issuance is [(10,000/7,500)1/(4×2)-1] x 4 = 14.65%. Therefore, the imputed interest is 0.1465*7,500 = $1,098.44, which is the amount declared on the lender’s tax form.

Now let’s say that lender decides to sell the bond after holding it for one year. The lender sells the bond for the initial price plus accrued interest: $7,500 + $1,098.44 = $8,598.44. Since there is only one year left until maturity, the imputed interest for the new lender is the face value minus the purchase price: $10,000 – 8,598.44 = $1,401.56.

Learn More

CFI is the official provider of the Capital Markets & Securities Analyst (CMSA)®Program Page - CMSAEnroll in CFI's CMSA® program and become a certified Capital Markets &Securities Analyst. Advance your career with our certification programs and courses. certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below:

- Accrued InterestAccrued InterestAccrued interest refers to interest generated on an outstanding debt during a period of time, but the payment has not yet been made or

- Applicable Federal Rate (AFR)Applicable Federal Rate (AFR)The applicable federal rate (AFR) is the interest rate that applies to personal loans. It is the minimum rate applicable to such loans under U.S. law.

- Effective YieldEffective YieldEffective yield is a financial metric that measures the interest rate – also known as the coupon rate – return on a bond.

- Par ValuePar ValuePar Value is the nominal or face value of a bond, or stock, or coupon as indicated on a bond or stock certificate. It is a static value

-

Understanding Vested Interest: Definition & Implications

Vested interest refers to an entity’s personal involvement in a business project, an investment, or the outcome of a given situation. Usually, they are situations that include the possibility of

-

Accrued Interest Explained: Accounting & Financial Definition

Accrued interest refers to interest generated on an outstanding debt during a period of time, but the payment has not yet been made or received by the borrower or lender. SummaryUnder accru

invest

- Coupon Bonds: Understanding Fixed Income & Interest Payments

- Discount Bonds: Understanding Pricing & Secondary Markets

- Understanding Dollar Duration: A Guide for Bond Investors

- Effective Interest Method Explained: Bond Amortization & Accounting

- Understanding Noncallable Securities: A Comprehensive Guide

- Samurai Bonds: A Guide to Understanding Yen-Denominated Corporate Debt

- Treasury Bonds: A Comprehensive Guide to U.S. Government Debt

- Zero-Coupon Bonds: Definition, How They Work & Examples

- Understanding Imputed Interest: Definition & Calculation

-

Understanding Interest Rates: A Comprehensive Guide

Understanding Interest Rates: A Comprehensive GuideAn interest rate refers to the amount charged by a lender to a borrower for any form of debtCurrent DebtOn a balance sheet, current debt is debts due to be paid within one year (12 months) or less. It...

-

Mortgages Explained: Your Guide to Home Loans & Financing

Mortgages Explained: Your Guide to Home Loans & FinancingA mortgage is a loan – provided by a mortgage lender or a bankTop Banks in the USAAccording to the US Federal Deposit Insurance Corporation, there were 6,799 FDIC-insured commercial banks i...